Welcome to Investors’ Edge— your daily dose of business insights, trends, and updates that matter. In this space, we go beyond the headlines to explore the evolving world of companies and industries. Each day, we bring you thoughtfully curated insights, sharp observations, and key developments shaping the business landscape.

Whether it's a strategic pivot by a market leader or an under-the-radar company making waves, we break it down for you — clearly, concisely, and consistently.

The Top 7 Learnings Covered in Today’s Edition:

Cables and Wires - Strong Results Across the board

Microfinance Lenders - Is this the worst that can happen?

Privi Speciality - Expanding through De-bottlenecking

Key takeaways for Hotel Industry - Indian Hotels’ Q4FY25 Concall

Impact on markets of Global Conflicts

PAYTM - Hitting the S Curve

Mahindra and Mahindra - Gaining market share

Cables and wires

The cables and wires sector demonstrated robust performance in the fourth quarter of the financial year ended 31st March 2025, driven by sustained underlying demand and strategic initiatives by key players

Key trends shaping up in the Industry:

Strong Demand Drivers: Demand for cables and wires continues to be strong. This momentum is supported by increased government spending, infrastructure project execution, and continued strength in the real estate sector. Demand is also seeing tailwinds from specific areas such as data centres, renewable energy projects, and industrial capex. While real estate demand in large metros has been slow, increasing market shares in Tier 2 and Tier 3 towns have helped the domestic wire business.

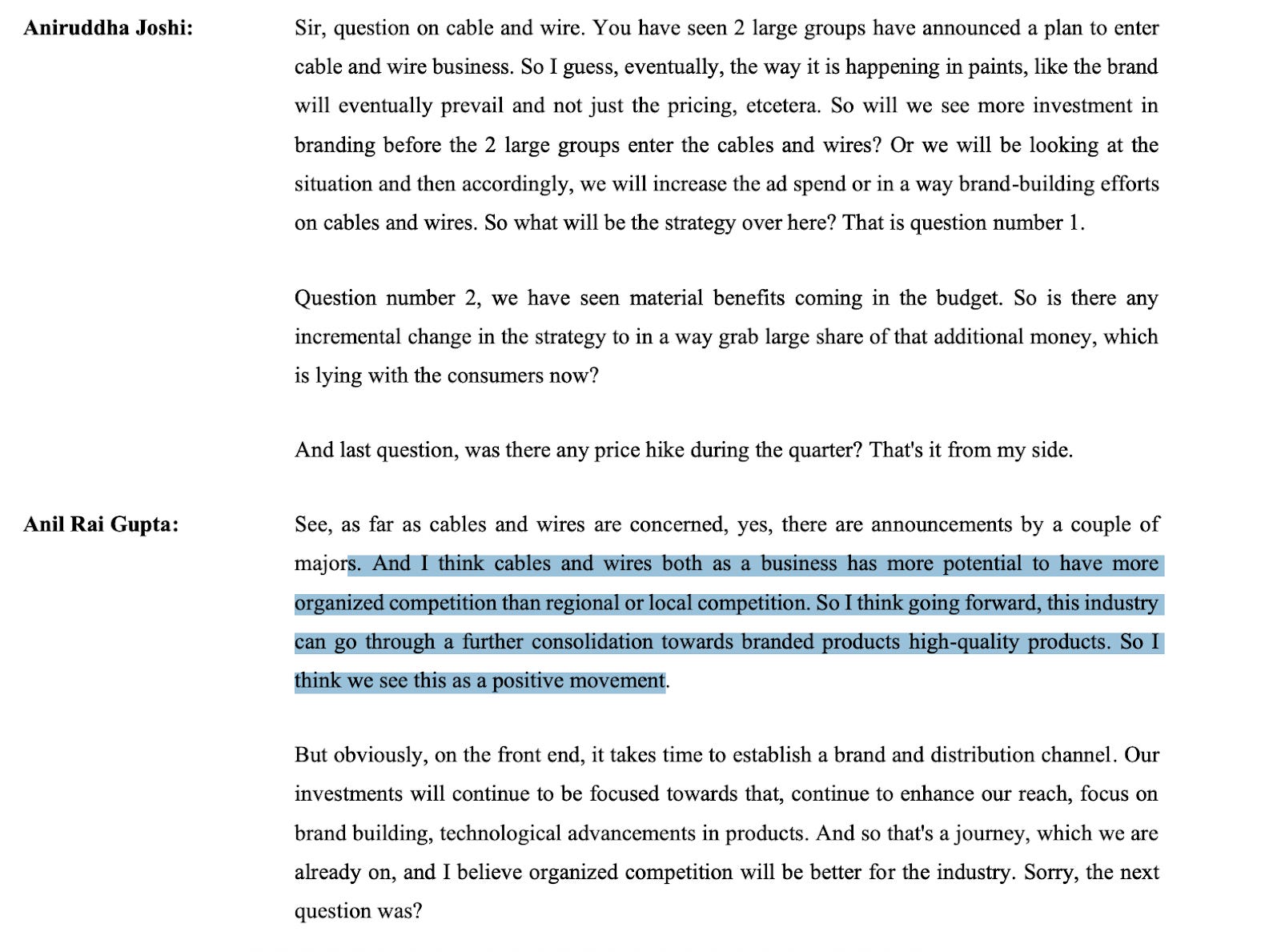

Competition and Formalisation: The industry is seeing increased participation from new entrants, including announcements by a couple of large groups. Companies like Havells and RR Kabel view this as a positive development that could lead to further formalisation of the sector, consolidating towards branded and high-quality products. While increasing competition is a factor, companies rely on quality, brand loyalty, consumer pull, distribution channels, and pricing as key differentiators. Establishing presence in segments like industrial cables requires long-term effort and approvals, acting as a barrier to entry.

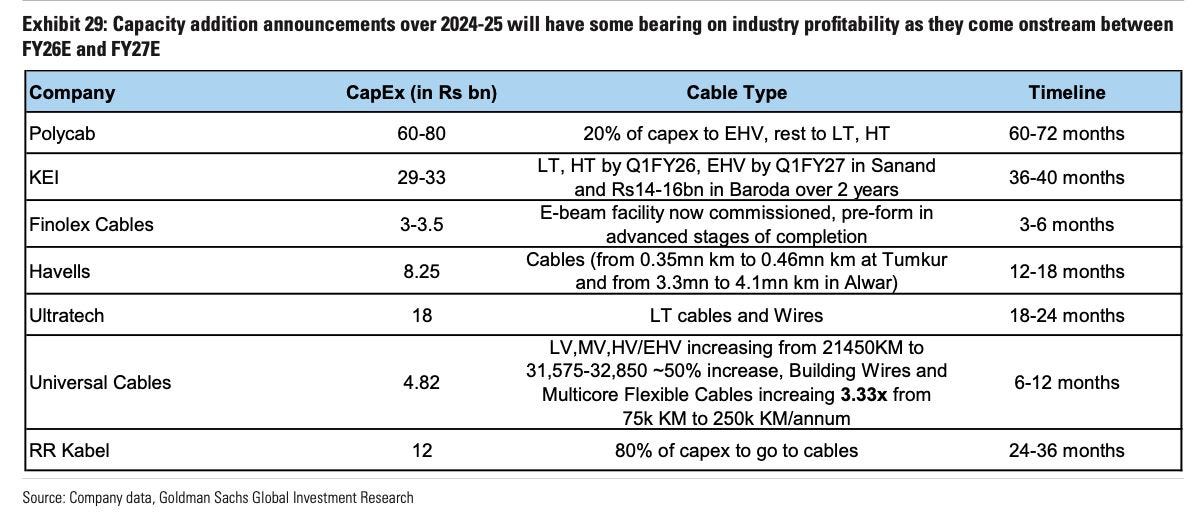

Capacity Expansion: To meet the rising demand and prepare for future growth, companies are actively investing in capacity expansion. New capacities are coming online or are planned, particularly focused on the cable segment.

Volume and Value Growth: Growth is driven by both volume and value. While volume growth is a key focus, particularly given strategic capacity additions, value growth also plays a significant role, sometimes reflecting favourable product mix or commodity price impacts.

Product Mix and Margin Improvement: Companies are focusing on optimising their product mix to enhance profitability. This includes increasing the share of higher-margin categories or leveraging scale in specific segments.

Export Market: Exports are an important part of the strategy for Indian players, leveraging India's position as a favourable trade partner. While global uncertainties exist, the outlook for Indian W&C exports is seen as positive, with export cable markets noted as highly profitable.

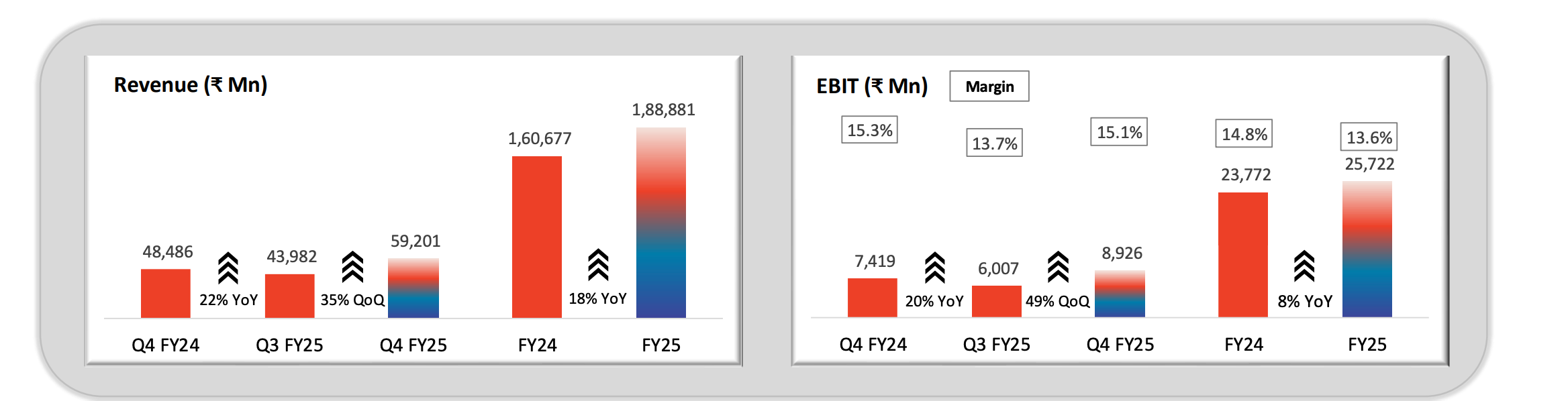

Havells

The Cables segment led Havells' overall revenue growth in Q4 FY25, showing a strong 21.2% year-on-year increase in revenue, reaching INR 2,169 crores. For the full fiscal year, the segment grew by 13.7% year-on-year to INR 7,184 crores.

In Q4, approximately half of the segment's growth was attributed to value growth. The business mix remained around 65% wires. Volume growth was more pronounced in underground cables compared to wires.

The contribution margin for the Cables segment saw a decline both year-on-year and quarter-on-quarter, standing at 14.7% in Q4 FY25 compared to 15.2% in Q4 FY24 and 15.0% in Q3 FY25. This decline was attributed to product mix changes and volatility in wire prices rather than being a normal level. The ramp-up of new capacity for cables at Tumkur is underway and has started contributing to growth.

Segment results (EBIT) were INR 259 crores in Q4 FY25, a 20.5% increase from INR 215 crores in Q4 FY24. The segment result margin was relatively stable at 11.9% in Q4 FY25 compared to 12.0% in Q4 FY24.

Havells views the entry of large groups into the cables and wires space positively, anticipating further consolidation towards branded, high-quality products. The company plans to continue investments in enhancing reach, brand building, and technological advancements. Exports of cables and wires remain a part of Havells' international strategy. Capex during FY25 included expansion for cables, and further capex is planned over the next two years, although specific allocation for cables and wires within the total ~INR 2,000 crore estimate was not detailed. Demand for cables remains strong

Polycab

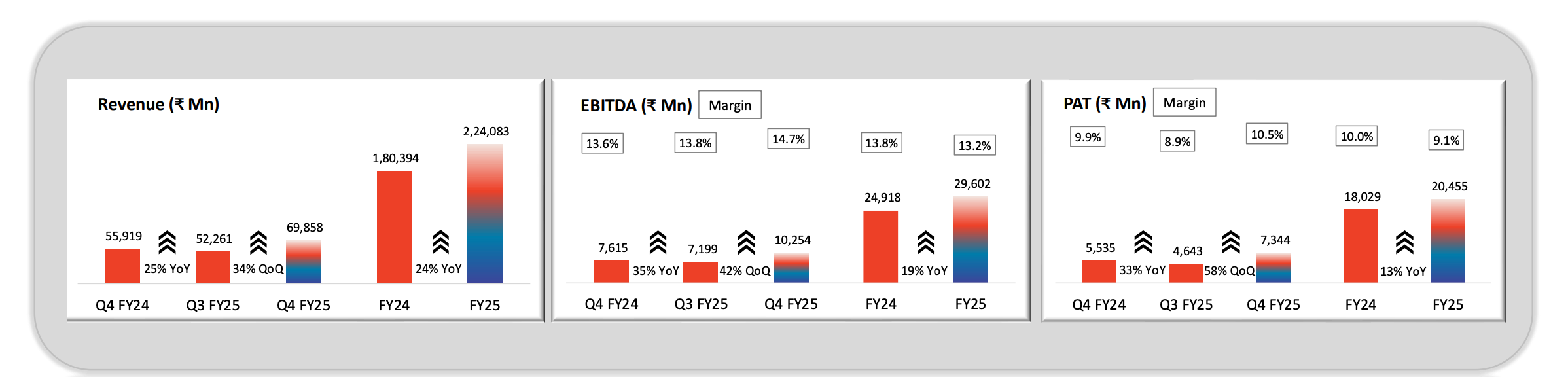

Polycab Reports Strong FY25 Results, Achieves FY26 Revenue Target Ahead of Time

Polycab India reported a 25% year-on-year revenue growth in Q4FY25, supported by steady performance across all business segments. For the full year, revenue rose by 24% YoY to over ₹22,000 crore, crossing the company's FY26 revenue goal of ₹20,000 crore a year ahead of schedule.

In terms of profitability, EBITDA grew by 35% YoY in Q4, with margins improving by about 110 basis points to 14.7%. This increase was mainly due to improved performance in the FMEG segment and better margins in the EPC business.

Net profit (PAT) grew by 33% YoY and 58% compared to the previous quarter, with margins increasing to 10.5%. Q4 PAT crossed ₹700 crore for the first time, contributing to a full-year PAT of over ₹2,000 crore.

Wires & Cables Segment Update: Domestic Growth Offsets Dip in International Business

During Q4FY25, the segment recorded solid growth, supported by continued demand across key sectors. Factors such as higher government spending, improved execution of infrastructure projects, firm real estate activity, and rising commodity prices contributed to this performance. The domestic business grew 27% YoY, with cables once again growing faster than wires. Both the channel and institutional segments showed steady momentum.

In contrast, the international business declined 24% YoY during the quarter, mainly due to the deferral of a large order to the next quarter. However, for the full year, it still contributed 6.0% to total consolidated revenue. A recovery in FY26 is anticipated, backed by a strong order pipeline and positive demand trends across key global markets.

Segment margins improved by around 140 basis points quarter-on-quarter to 15.1%, aided by better operating leverage and a favourable product mix, though the lower contribution from international operations limited the overall upside.

FMEG Segment Turns Profitable in Q4FY25, Closes Year with Record Revenue

Polycab’s FMEG (Fast-Moving Electrical Goods) business achieved a key milestone in Q4FY25 by turning profitable for the first time, following ten consecutive quarters of strategic investments in talent, innovation, and brand building.

The segment also reported a 33% YoY growth in Q4 revenue, while full-year revenue reached an all-time high of ₹1,653 crore, up 29% YoY.

Growth was seen across all product lines. The fans category performed well despite a delayed summer, reflecting gains from premiumisation efforts. Lights and luminaires maintained strong momentum with volume and value growth, even amid ongoing pricing pressures. Switchgears, conduit pipes, fittings, and switches also posted healthy growth, supported by consistent demand from the real estate sector.

Solar products saw particularly strong traction, growing nearly 2.5 times year-on-year, and are now the third largest contributor within the FMEG portfolio.

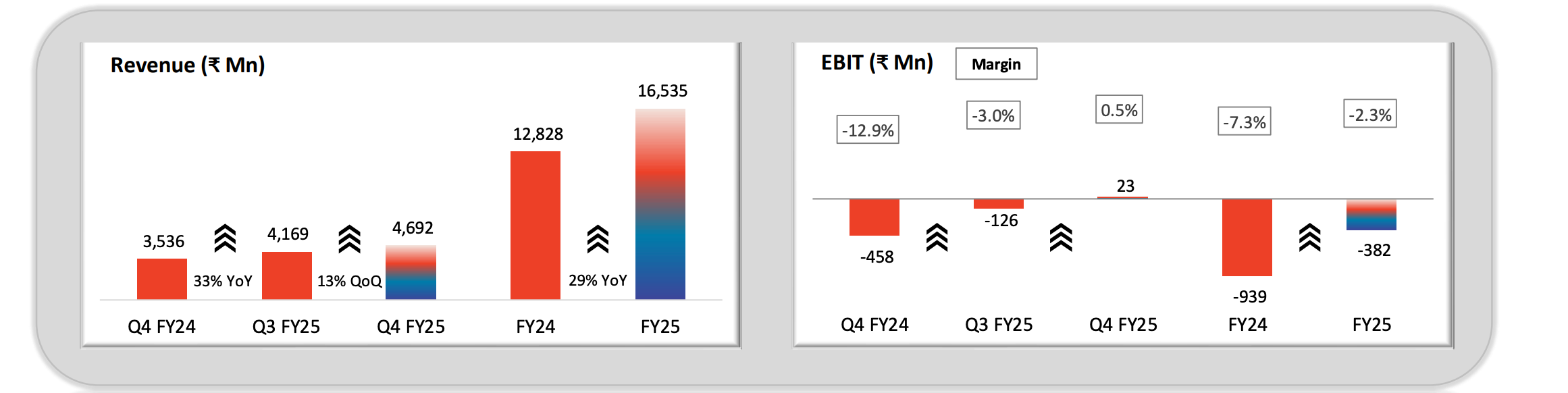

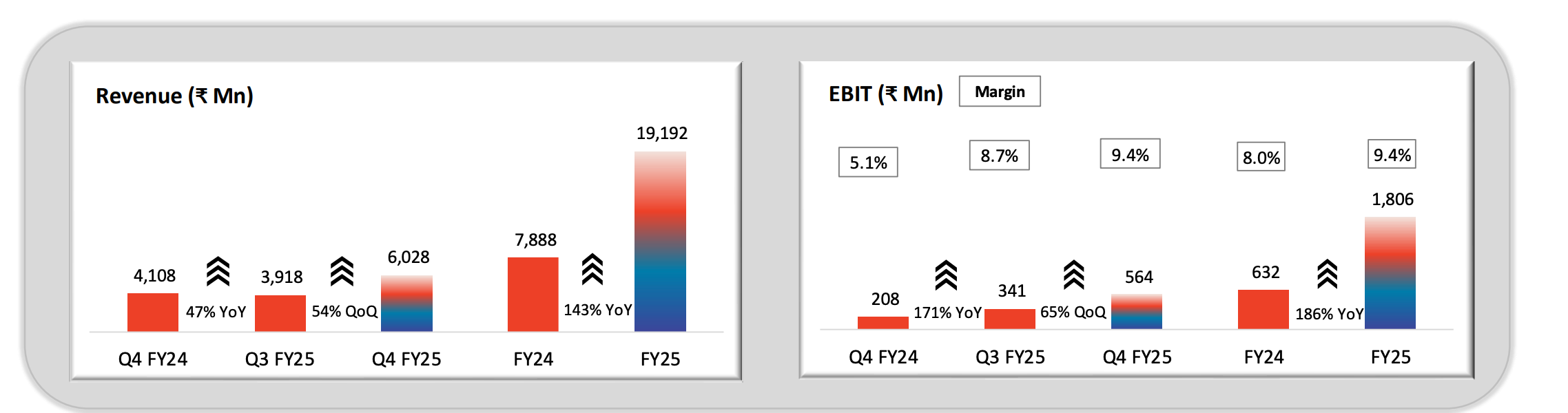

EPC Segment Delivers Strong Growth, Margins Align with Long-Term Targets

Polycab’s EPC (Engineering, Procurement & Construction) segment reported a 47% year-on-year increase in revenue for Q4FY25, supported by strong execution of the RDSS (Revamped Distribution Sector Scheme) order book. For the full year, the segment recorded a 143% increase in revenue compared to FY24.

On the profitability front, EBIT rose by 171% YoY in Q4, with the EBIT margin improving to 9.4%. For FY25 overall, EBIT grew by 186%, reflecting improved operational efficiency and scale.

The segment’s annual operating margins are now in line with the company's expectations for the mid-to-long term, aiming to maintain high single-digit margins on a sustainable basis.

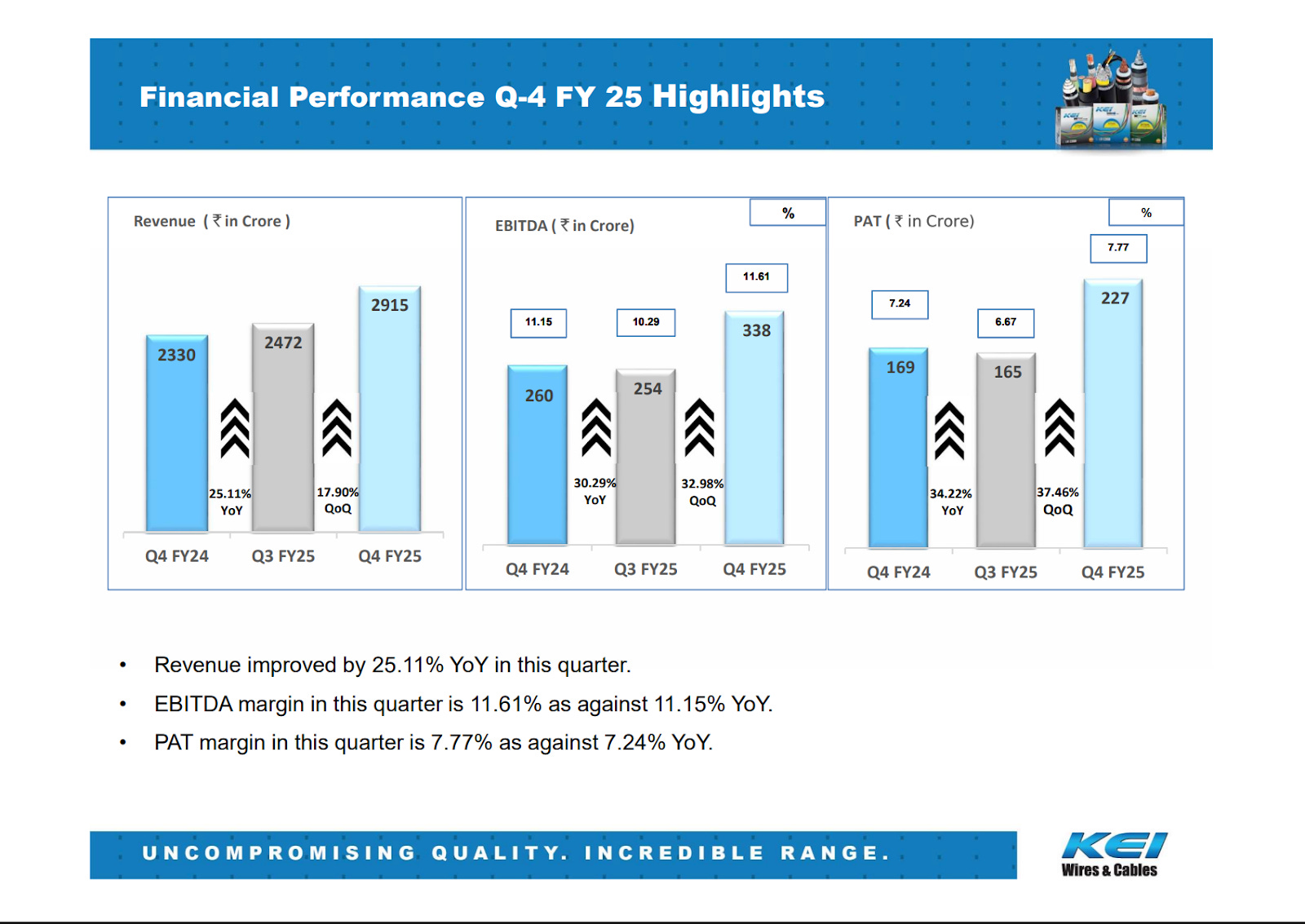

KEI Industries

Revenue jumped to about ₹2,915 crore, marking a 25.1% rise over last year’s March quarter and nearly an 18% uptick from Q3 FY25 .

EBITDA came in at ₹338 crore (an 11.6% margin) and PAT climbed to ₹227 crore, roughly a 33% gain year‑on‑year .

Cable and wire sales to institutions (including exports) hit ₹1,328 crore, up about 28% versus Q4 FY24 .

Shipments through dealers surged over 40% to roughly ₹1,498 crore, accounting for about half of total sales .

KEI ended the quarter with net cash of around ₹1,737 crore and a backlog of orders near ₹3,839 crore—plenty of fuel for the next leg of growth .

All in all, a neat quarter that keeps the momentum rolling into FY26.

RR Kabel

The Wires and Cables segment is the cornerstone of RR Kabel's business, delivering strong revenue growth of 28.4% year-on-year in Q4 FY25 to INR 1,956 crores. For the full year, the segment grew by 14.7% to INR 6,689 crores.

Q4 FY25 saw the highest volume growth of the year for the segment, at approximately 14% year-on-year and 24% sequentially. Sequential growth was purely volume-led. For the full year FY25, cable volume grew significantly faster (~19%) than wire volume (~1-2%), contributing to the segment's overall 7% volume growth for the year.

Segment profit grew substantially by 47.1% year-on-year in Q4 FY25 to INR 194 crores. This improvement was driven by better contribution margins and operational efficiency, with volume growth being the major contributor to margin improvement, alongside a slight benefit from upward metal prices.

Demand was robust in both domestic and export markets after two relatively subdued quarters in FY25. Domestic growth is expected from real estate resurgence, data centres, renewables, and industrial capex. The company's working capital cycle improved significantly to 56 days in FY25, expected to normalise around 60 days.

Exports contributed a stable 26% to total revenue in FY25 and grew 11% year-on-year. RR Kabel sees good export demand, particularly from the EOP market, and is optimistic about the Indian W&C industry benefiting from global uncertainties. Export cable margins are noted as highly profitable (~12-13%) compared to domestic cable margins (~6-7%) or export wire margins (~5-6%). Domestic wire margins (~12%) are the strongest domestically.

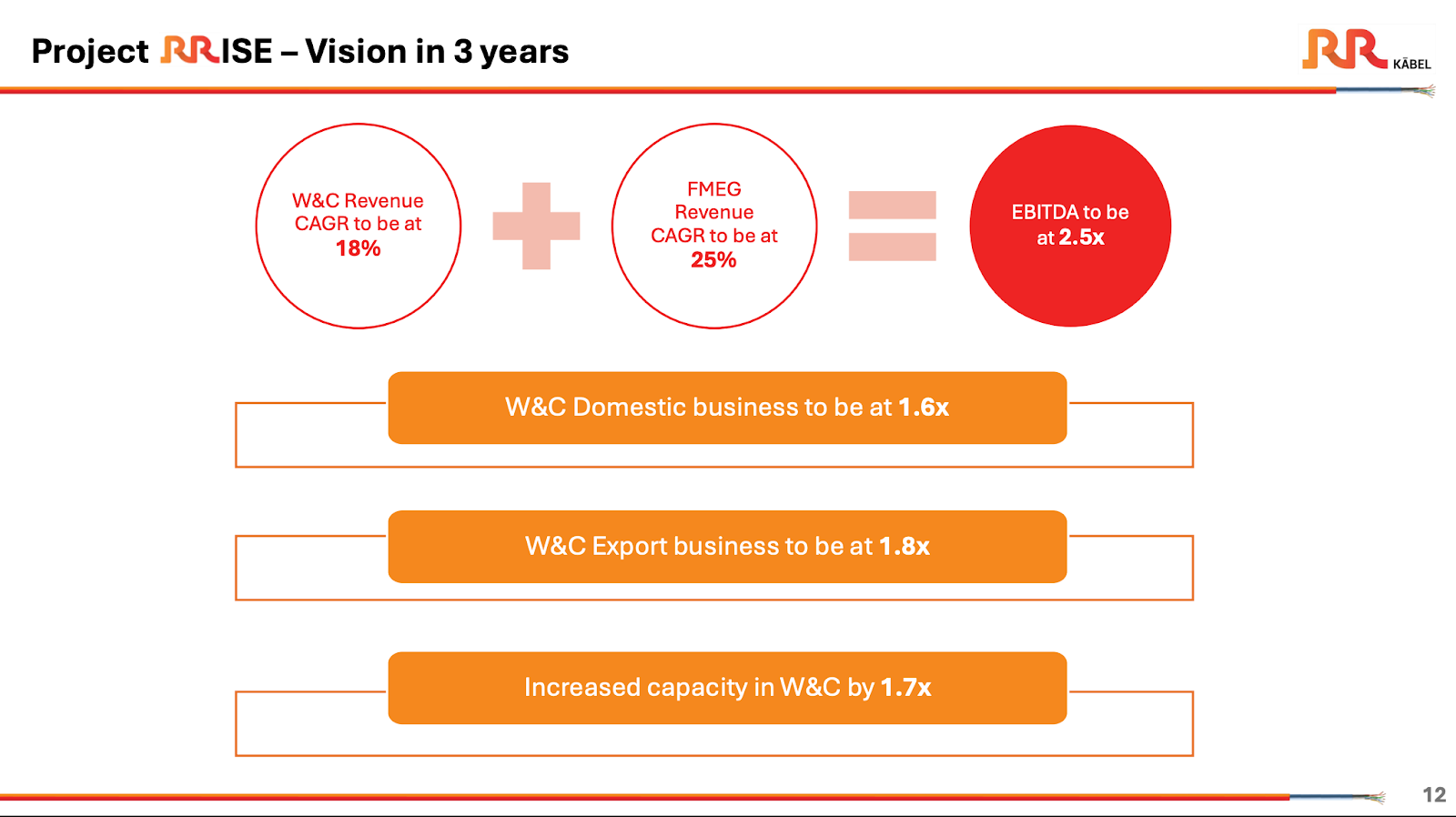

Under its 'Project Rise' strategic vision for the next three years, RR Kabel aims for an 18% W&C Revenue CAGR. This is expected to be largely driven by faster growth in the cable segment, where the company is currently under-indexed relative to the industry mix (RR Kabel is ~70% wire, 30% cable vs industry ~35% wire, 65% cable).

To support this, RR Kabel is undertaking a major capacity expansion of approximately 1.7x across its Silvassa (wire) and Waghodia (cable) facilities with an investment of around INR 1,200 crores over FY26-28. This expansion, particularly in cable capacity, is intended to enable 15-20% volume growth in cables and improve margins.

Margin improvement in W&C is a critical focus, targeted through rebalancing the sales portfolio mix towards higher-margin products and achieving better margins in cables through scale. RR Kabel expects to improve W&C margins by 100 basis points in the coming year. The company is also expanding its cable product portfolio to include more MV and HV cables.

Microfinance Lenders - Q4 Update

The fourth quarter of the Financial Year 2025 provided a mixed, yet increasingly hopeful, picture for the microfinance sector, following what was widely acknowledged as a challenging year. While headwinds persisted, particularly related to asset quality and regional disruptions, lenders discussed strategic adjustments and observed signs of potential normalisation.

Performance and Asset Quality Trends:Several lenders noted the challenging business environment during the year, especially in the microbanking segment. Equitas Small Finance Bank, for instance, experienced a significant increase in microfinance credit costs, rising to 11.37% in FY25 from 2.3% in FY24, which substantially impacted their profitability. In response, Equitas slowed down fresh disbursements in microfinance, leading to a notable drop in their MFI advances and a significantly reduced share of MFI in total disbursements in Q4 FY25 compared to the previous year. Equitas expects their MFI book to continue to degrow in FY26.

Ujjivan Small Finance Bank, on the other hand, saw a robust growth in Micro Banking disbursements by 38% quarter-on-quarter in Q4 FY25, although their Group Loan (GL) book de-grew by 4% for the quarter. This disbursement growth was primarily driven by lending to good existing customers. Ujjivan managed to maintain what they consider one of the best portfolio qualities in the industry within the microbanking segment. Their Portfolio at Risk (PAR), Gross Non-Performing Assets (GNPA), and Net Non-Performing Assets (NNPA) ratios all showed improvement in Q4 FY25 compared to Q3 FY25, and their SMA book started to reduce, with PAR seeming to have peaked in Q4.

AU Small Finance Bank saw an improvement in overall asset quality in Q4 FY25, with GNPA and NNPA ratios decreasing compared to Q3 FY25. Slippages also improved in Q4, including in their Secured assets and MFI portfolios. However, AU's Microfinance credit cost remained elevated at 7.75% for the full year FY25.

Five Star Business Finance, while not a traditional MFI (focusing on secured business loans), noted that their gross stage 3 assets (GNPA) inched up in Q4 FY25. They attributed this largely to disruption in collections in Karnataka from January to March 2025, alongside a general issue of over-leverage. They aim to maintain gross NPAs below 2% and credit costs below 1% for their portfolio, which serves middle and lower-middle-class customers with average ticket sizes between three to five lakhs.

Challenges and Contributing Factors:A significant factor impacting asset quality and collections discussed by lenders was the disruption in Karnataka, particularly noted by Five Star and Ujjivan. Five Star estimated that two-thirds of their collection dip was due to the Karnataka situation. Ujjivan's Bucket-X collection efficiency in Karnataka was notably lower (98.7% in March '25) than in other states (99.6%), despite overall improvements elsewhere.

The issue of over-leverage among borrowers was also highlighted. Five Star noted that while this crisis was still prevailing, the threat of more over-leverage had reduced as small ticket lenders had stopped significant lending to this segment.

Regarding the Tamil Nadu ordinance, Equitas stated they had not seen any impact on collection behaviour as of their earnings call.

Strategic Responses and Regulatory Environment:Lenders are actively implementing strategies to navigate the challenging environment and mitigate risks. Diversification is a key theme, with Ujjivan significantly increasing the share of their secured loan book to 44% by March '25, up from 30% the previous year, focusing on Housing and MSME segments. AU Small Finance Bank also has MFI as part of its secured asset mix. Equitas is focusing on growing their Small Business Loans (SBL) and Vehicle Finance books while shrinking their MFI portfolio. Five Star is adjusting its focus within its secured lending, moving towards larger ticket sizes (3-10 lakhs) and reducing exposure to the less than 3 lakhs segment, which they feel is sometimes wrongly bucketed with MFIs and perceived to have slightly higher stress.

Accelerated provisioning was undertaken by both AU (₹150 Cr in Q4) and Ujjivan (₹46 Cr for FY25) to strengthen provision coverage.

The MFIN guardrails, including limits on the number of lenders (three lenders) and borrower indebtedness caps, were seen as structurally positive for the industry, expected to increase discipline. Ujjivan has implemented Guardrail 2 fully from April 1st, and Five Star believes these guardrails will help contain over-leverage and potentially lead to increased credit demand for regulated entities as the supply from small ticket unsecured lenders reduces.

The CGFMU credit guarantee scheme was highlighted by AU as a critical backstop for eligible MFI loans, enabling them to lend more confidently and mitigate downside risk. AU expects to cover nearly 100% of Q4 MFI disbursements under this scheme, aiming for over 75% coverage on their overall book in the future.

Outlook:

Despite the challenges faced, there is an expectation of gradual improvement. AU anticipates that their MFI credit costs will take two more quarters to reach near normalcy (around Q3-Q4 FY26). Equitas expects credit costs to remain elevated in Q1 and Q2 FY26 due to a lag effect of previous slippages, with normalisation anticipated from Q3 onwards. Five Star expects the impact of the prevailing stress (related to over-leverage and Karnataka) to continue for at least the next two quarters. Ujjivan's management noted that while the business momentum picked up in Q4, the Microbanking business still needs to navigate some geography-specific issues and industry guardrail mandates before providing full-year guidance.

In summary, Q4 FY25 reflected an industry grappling with lingering asset quality pressures and regional issues in microfinance, prompting strategic shifts towards diversification and risk mitigation. While some normalisation is expected, the timeline varies, with lenders keeping a close watch on the impact of regulatory guardrails and the evolving market dynamics.

Privi Speciality - Expanding through De-bottlenecking

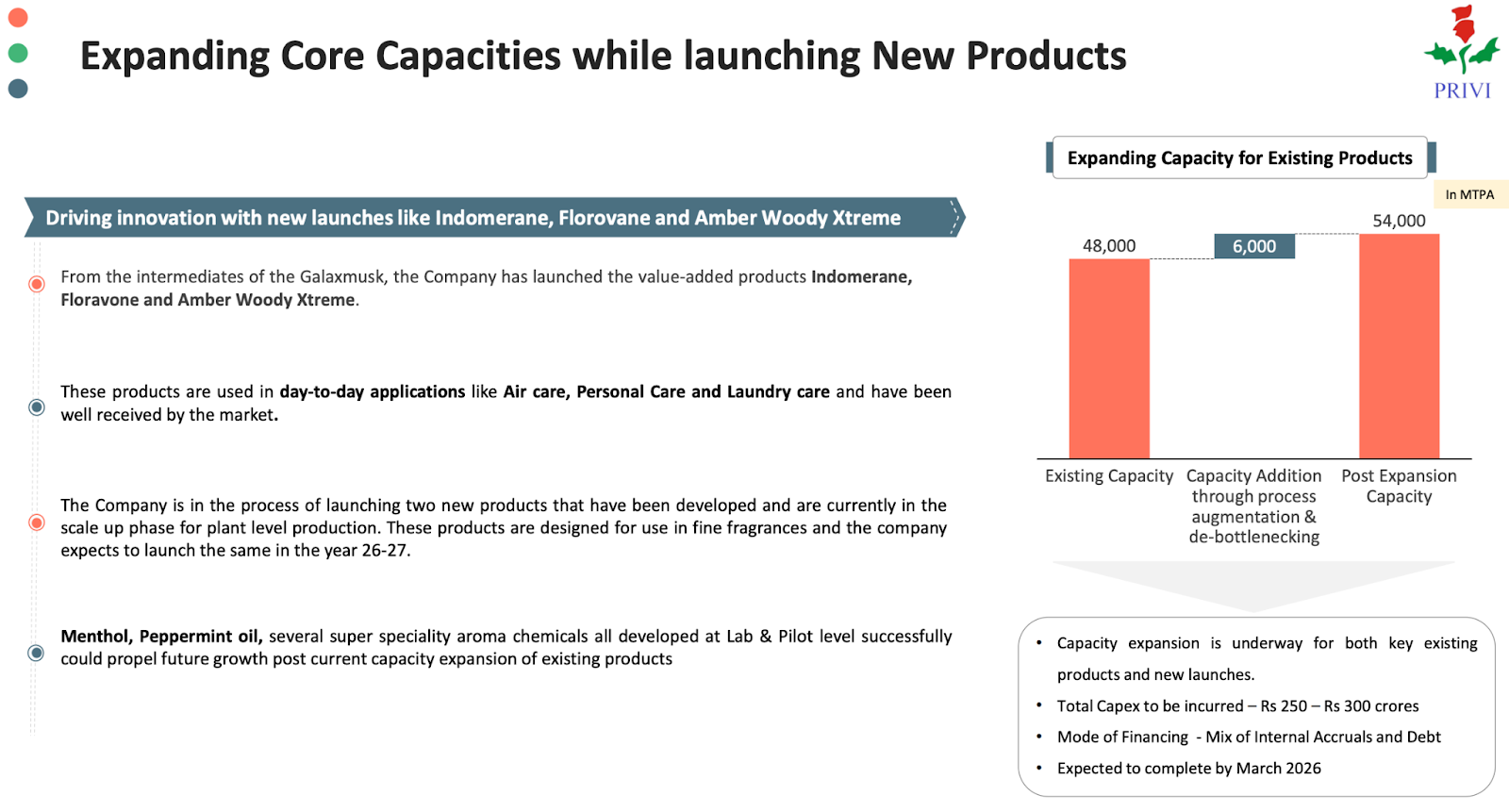

Privi is growing its production capacity while also launching new, high-demand aroma products.

Capacity expansion is underway for both key existing products and new launches.

Capex Plan: Rs 250 – Rs 300 crores.

Mode of Financing: Mix of Internal Accruals and Debt

Timeline: Expected to complete by March 2026

Concall Notes -Q4FY25

Three newly launched products are fully booked.

Two new premium products are planned for launch.

Demand remains strong across all key products.

The company is expanding production capacity from 48,000 MTPA to 54,000 MTPA, expected to be completed by March 2026.

Debottlenecking efforts are underway to address growing demand.

JV with Givaudan (Citroda) expected to contribute ₹300–350 crore to topline over the next 2–3 years.

EBITDA margins are expected to remain in a similar range in the upcoming quarters.

The company aims to maintain EBITDA margins north of 20%.

Revenue growth target remains at 20–25% YoY.

1.5x–1.7x asset turns, with plans to further improve.

Working capital cycle is under ongoing improvement.

Core strength lies in backward integration, supporting margin resilience.

Actively working on reducing energy costs.

Ambition is to become the world’s No. 1 aroma chemical company — and management believes they’re not far from it.

Minimal exposure to the U.S. market (only 7% of sales) — management sees no significant impact from tariffs.

Key takeaways - Hotel Sector

Strong Industry Fundamentals and Up-cycle

The hospitality sector is currently in an "up-cycle". This positive trend is driven by strong domestic demand, limited supply additions, and favourable demographics in India.

A fundamental driver of performance is that demand, represented by room nights sold, grew 6% in FY24-25, while the supply of room nights available grew only under 3% compared to the previous year.

This trend of demand continuing to outpace supply is a key factor supporting the sector and is expected to sustain in the mid-to-long term.

What were the demand drivers?

Strong domestic business travel, coupled with mega events like Mahakumbh, international music concerts (Coldplay), and a strong wedding season, were key demand drivers in FY24-25

India's position as the fastest-growing large economy, rising disposable incomes, addition of new tourist destinations, and evolving traveller behaviours are expected to sustain this demand

What is the future outlook here ?

The outlook for FY26 and beyond is considered robust.

The current financial year has started strongly, with industry indicators suggesting minimum double digit growth for the sector in the first quarter.

The overall environment suggests continued strong growth.

Also performance metrics remains solid (ARR & RevPAR)

RevPAR is highlighted as a key metric for the sector.

Strong performance is being seen in both Average Room Rates (ARRs) and RevPAR.

The ability for the sector to comfortably pass on inflation, potentially by 1 to 2% over the inflation rate, continues to exist.

There does not appear to be any indication that ARRs have peaked.

The Premiumisation Trend continues and Traveller behaviour continues to evolve

Traveller behaviour is evolving, with booking windows becoming shorter, particularly outside of main holiday seasons

Crucially, there is a significant increase in the willingness of people in India (estimated at over a million) to pay for quality, experiences, and premiumisation

This is evident in trends like small, high-quality restaurants being booked out months in advance.

Growth in Foreign tourists arrival can also boost up the demand

While domestic demand is strong, there is significant potential for growth in foreign arrivals. Although the number of technical arrivals has increased recently, the sector has not yet returned to pre-COVID tourism levels

Increased business interest in India, driven by its growing economic relevance, is leading to more business-related foreign travel

The industry, through various associations, is actively engaged in promoting India internationally and lobbying the government for dedicated international marketing budgets

India's relatively lower tariffs compared to some other destinations could potentially help attract more business visits.

Tier II and Tier III offer interesting opportunities

While buying land from scratch and undertaking pure greenfield developments may still not offer attractive Internal Rates of Return (IRRs) at current rates, greenfield opportunities in Tier 2 and Tier 3 cities or new markets can be very interesting and viable

This is often the case when land is acquired at a compelling proposition, sometimes supported by government infrastructure development programs, leading to expectations of quick payback periods (e.g., within 7 years, or even 4-5 years)

Industry reports indicate that over 50% of hotel signings in CY24 were greenfield, suggesting such context-specific opportunities are being pursued.

In conclusion, IHCL's Q4 FY25 earnings call paints a vibrant picture of the Indian hotel industry

It's firmly in an upcycle driven by robust domestic demand and demand significantly outpacing supply.

With healthy growth in ARRs and RevPAR, evolving traveller behaviour favouring premiumisation, and significant potential for increased foreign arrivals, the outlook remains robust with expectations of continued double-digit growth....

While rising competition is a factor, the fundamental dynamics suggest a period of sustained positive performance for the sector in the mid-to-long term....

Mahindra and Mahindra - Gaining market share

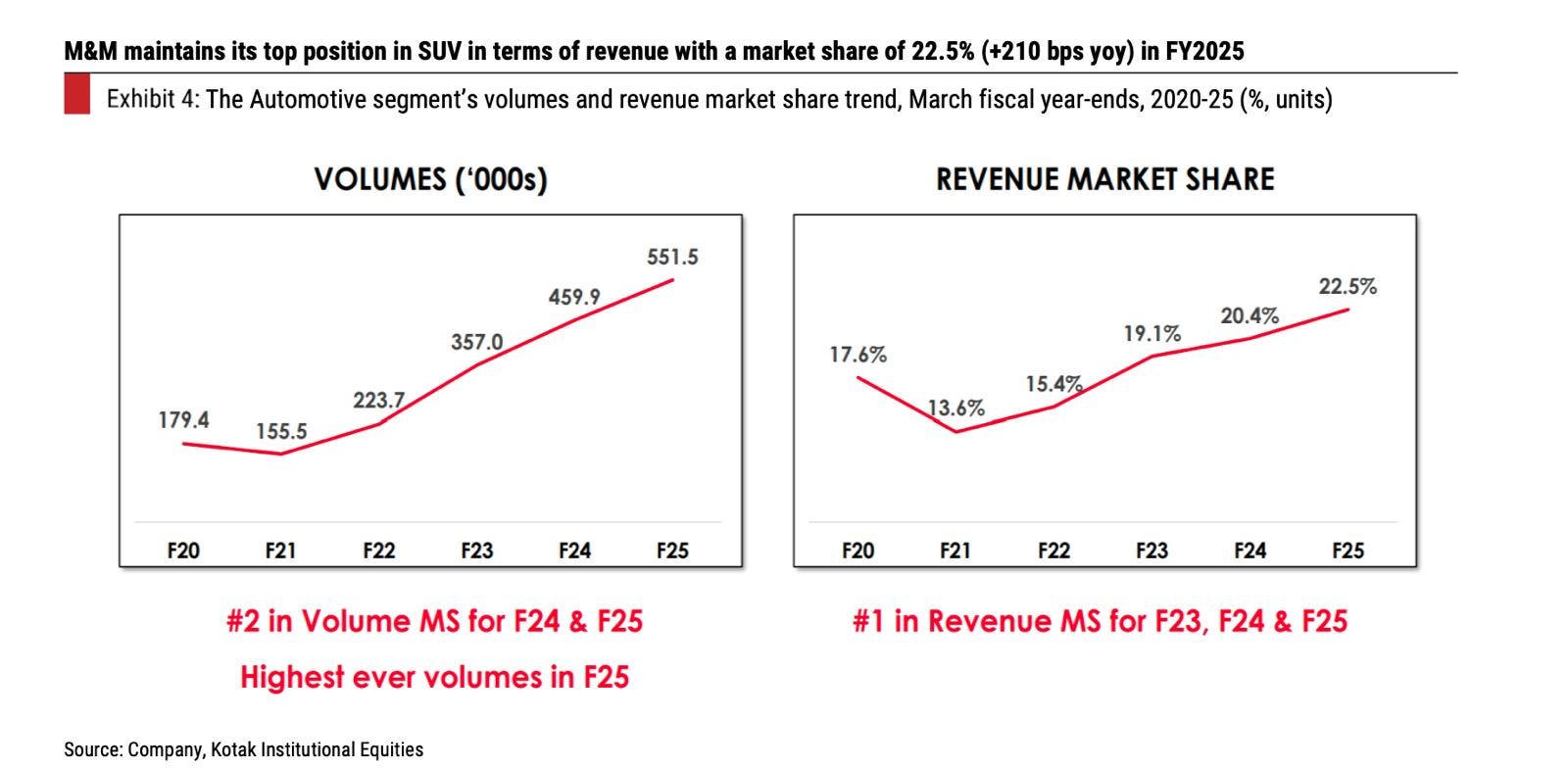

M&M strengthened its SUV revenue market share by 210 bps year-over-year in Q4FY25, securing the top spot. This growth was fueled by new models like the XUV 9e and BE6, along with price adjustments for certain XUV 700 versions. In the <3.5T LCV category, the company's market share increased by 290 bps year-over-year to 51.9% in the same period. M\&M also continued to lead the EV 3W segment, achieving a 42.9% market share in Q4FY25, a 110 bps quarter-over-quarter improvement. The company introduced four new EV 3W products last quarter: Treo Metal, Zeo, eAlfa Plus, and Alfa Duo.

PayTm - Hitting the S Curve

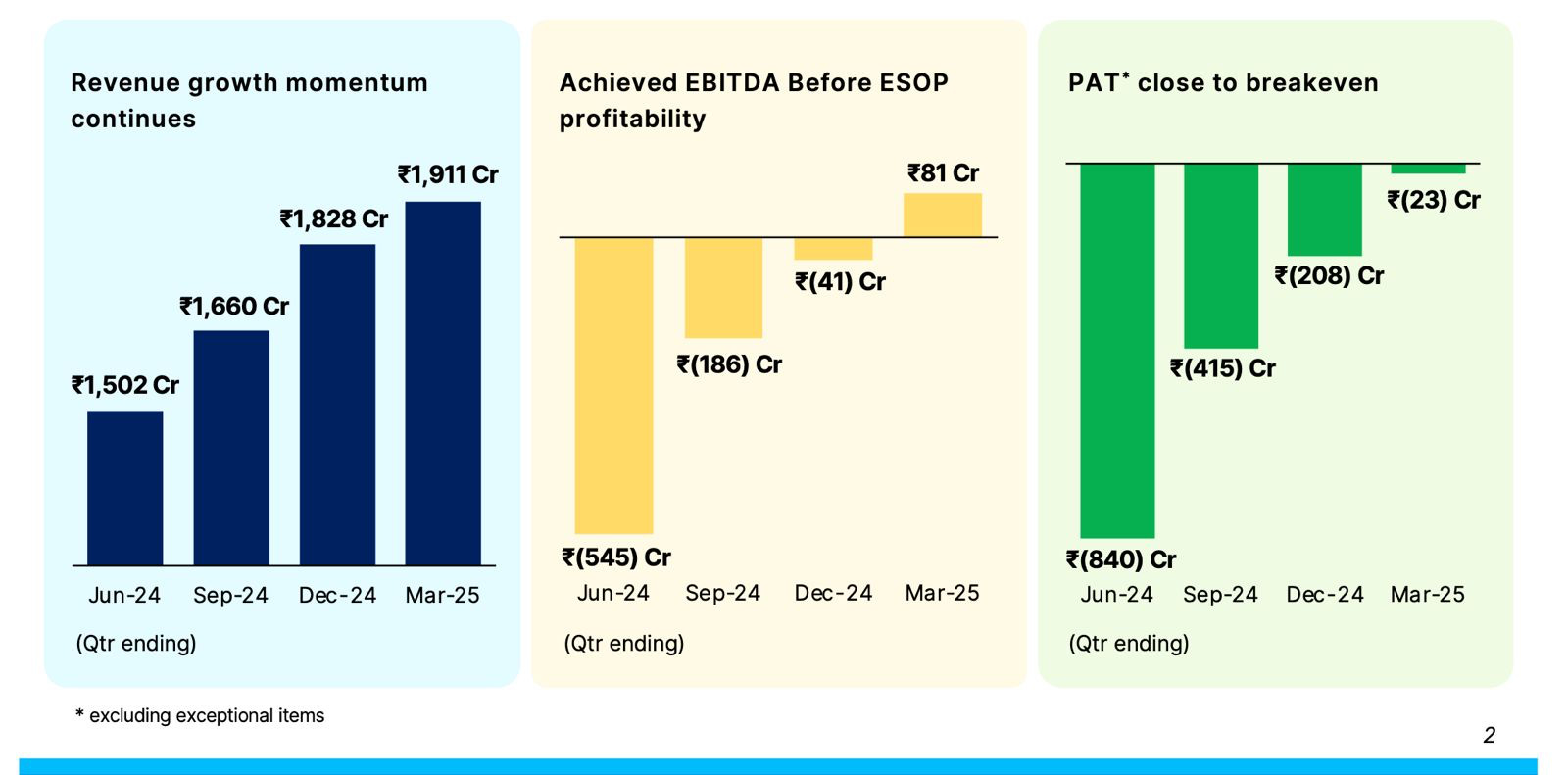

Paytm’s Q4 FY25 results mark a crucial turning point for the fintech giant, signaling resilience and recalibration amid regulatory headwinds.

After a turbulent FY24, marked by regulatory action against Paytm Payments Bank and sharp contraction in business operations, Q4 FY25 showcased early signs of a turnaround. While revenues dropped 3% QoQ to ₹2,267 Cr, the company made significant progress in realigning its business model.

What’s Next?

Expansion of new financial services products with a partner-first approach.

Focus on monetizing merchant and consumer platforms with ecosystem-led plays.

Strong intent to hit profitability at PAT level—already adjusted EBITDA positive for 6 straight quarters.

Q4 FY25 shows Paytm is down but not out. Strategic cost control, retention of core merchants, and a rebooted banking model are signs of a business realigning for sustainable, profitable growth. If execution remains tight and regulatory risk subsides, the comeback story might just be real.

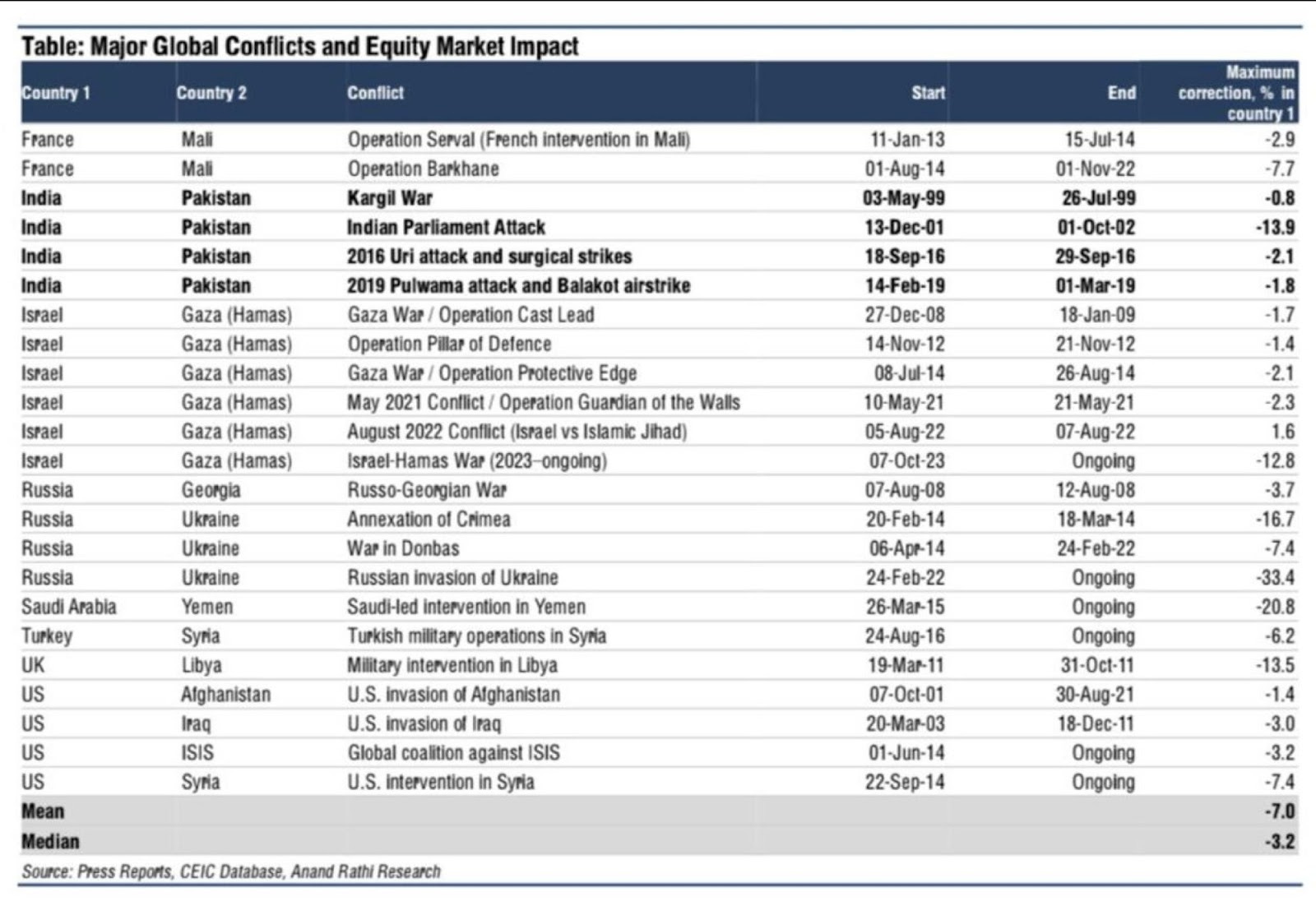

Impact on Markets of Global Conflicts

Historical Resilience: In four major India–Pakistan standoffs since 1999 (Kargil, Parliament attack, Uri strikes, Pulwama/Balakot), the Nifty 50 never dropped more than 2%, except during the 2001 Parliament attack (‑13.9%). 2001 drop was also coincided with global turmoil as at that point S&P 500 was also down close to 30%

Global Conflict Norms: Across 25 major conflicts worldwide, equities average a 7% correction (median 3.2%).

Current Tensions: Renewed India–Pakistan friction may spark short‑term volatility, but a steep market crash seems unlikely seeing the historical trends

Expected Range: Even under significant escalation, historical precedent and current risk pricing imply a 5–10% max pullback for the Nifty 50.

Investor Strategy: Focus on fundamentals, avoid knee‑jerk selling, and view geopolitical jitters as temporary rather than market‑derailing.

Disclaimer: The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

%2016_9.png)

0 Comments