%2016_9.avif)

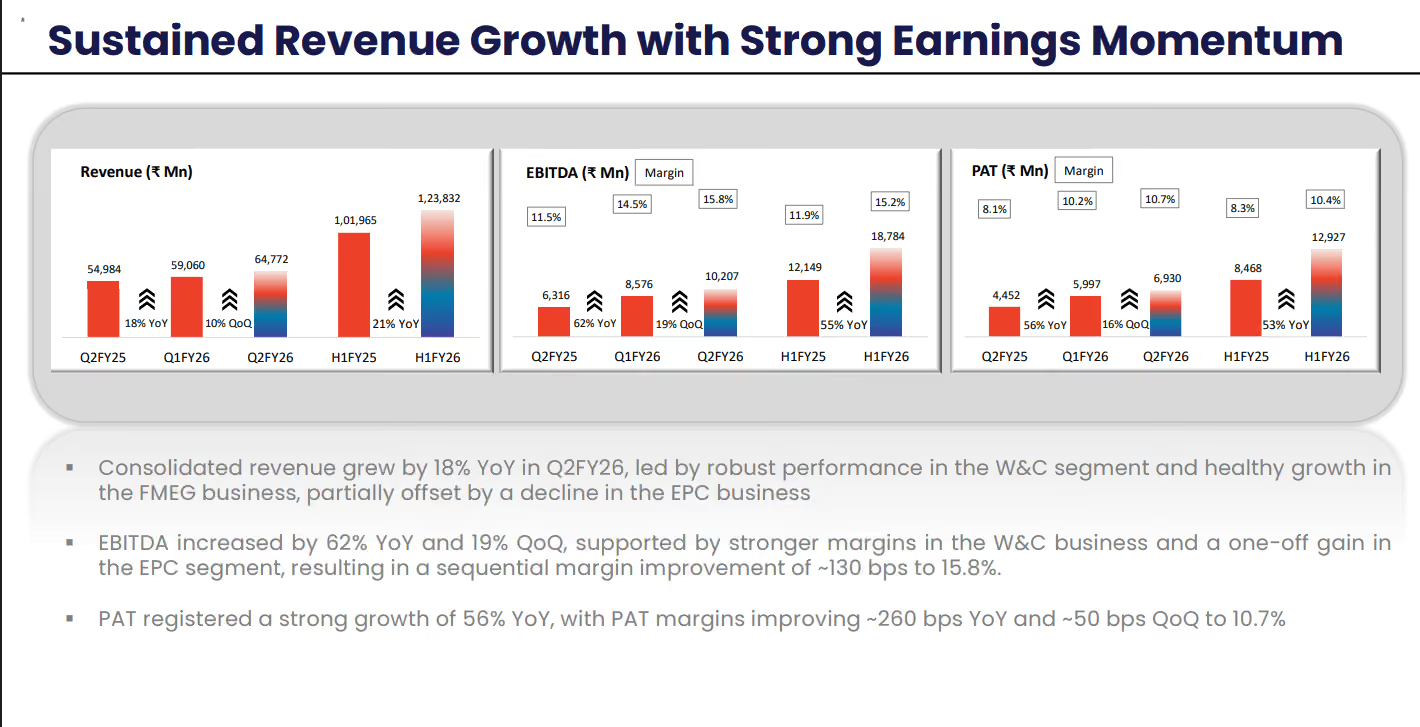

As the world shifts toward electrification and energy efficiency, the unsung champions powering this transition are often found in the humble cables and wires that run through the heart of every major infrastructure project. In this edition of Investor’s Edge, we delve into the Q2 FY26 results of three industry players Polycab, KEI, and RR Kabel who are quietly but powerfully driving the future of connectivity, energy, and automation.

While much of the spotlight goes to tech giants and software breakthroughs, the real story of growth is playing out in the industrial corridors, with these companies showing that innovation in cables and wires can be just as impactful as the next big software revolution. From revenue growth and margin trajectories to strategic investments in expanding capacity, we uncover how these players are not just riding the wave of electrification but are shaping it.

In this edition, we’ll explore how their recent Q2 FY26 results highlight the resilience of the industry amid a rapidly evolving macroeconomic landscape. We’ll also dive into the key takeaways from their conference calls, touching on growth drivers, Project RISE initiatives, and the continued push towards sustainable capex investments. These insights offer a deeper look at how Polycab, KEI, and RR Kabel are positioning themselves for long-term success, making them companies to watch in the years ahead.

“Looking at the broader environment, demand remains robust across key sectors. Central government capex spend continues to remain robust. Additionally, the Government of India released an extra ₹ 1 trillion in tax devolution to states on 1st of October ahead of the festive season to accelerate capex and welfare spending, a timely fiscal boost for infrastructure and development projects. India's private capex cycle is also showing early signs of revival after a period of subdued activity, supported by monetary easing such as rate cuts and liquidity infusion, fiscal stimulus like front-loading of capex and tax cuts and regulatory reforms”

“The government, as you would have seen in the numbers, they are front-loading their capex and has already spent ~38% of their yearly target. We are also seeing a lot of green shoots in few of the private sectors as far as capex is concerned. And all of those put together are helping in terms of the volume growth on the cables and wires business.”

—Chirayu upadhya, Head of Investor relations , Polycab India.

Venturing into Special purpose cables to cater specialised cables demand from Defence , EV, Auto & Railways

“Within the special purpose cables (SPC) vertical, we cater to 3 types of opportunities — defense, automobiles, and railways, specifically railway coaches. These three put together form part of our SPC vertical. As of now, the contribution of SPC vertical to our overall cables and wires would be in low single digits. However, looking at the kind of investments which are happening in those sectors, it can be one of the fastest-growing vertical for us. As far as the opportunity size is concerned, you can track the announcements of government related to defense. Similarly, on the automobile side, you can look at the investments happening on the EV side as well as on the railway coaches side.”

— Chirayu upadhya, Head of Investor relations , Polycab India.

Volume growth is faster in the cables vs wires

“As far as the growth is concerned, the 21% revenue growth is on the base of high teens volume growth, and the remaining is the value contribution. Both cables and wires have registered strong growth. As far as the revenue growth in both cables and wires are concerned, they are pretty much equal. Again, on the volume terms, the growth will be a bit higher on the cable side, and a bit lower on the wire side, but that is because of very high base of wires in Q2 of previous year. If you would recall, in September of last year, we had seen an upward trend in copper prices in the last 15 days, which had led to a lot of pre-emptive stocking by distributors. As a result, we sat on a very high base as far as wires are concerned. Even on that, we were able to register doubledigit volume growth in the wires business - with in line revenue growth with cables. So that was the breakup of volume versus value.”

— Chirayu upadhya, Head of Investor relations , Polycab India.

Project spring on track while being ahead on the track

“Under Project Spring, we continue to make steady progress in line with our FY 2030 strategic guidance. Within Wires & Cables, growth in the first two quarters since the project's launch has been ahead of guidance at 1.5x to 2x of the industry growth rate, with margins above the guided range”

— Chirayu upadhya, Head of Investor relations , Polycab India.

15%+ Margins in cables and wires in structural in nature led by Operating leverage and business efficiencies .

“As far as margin increase is concerned, see, it is a mixture of a lot of things. Operating leverage is definitely one of them, but also the business mix change is one of them. YoY, if you look at the exports mix, it's not very different. QoQ, yes, it is better. The margins in exports are definitely better. But unlike some of our peers, we don't operate through distributors when we export. We operate mainly through institutional channel. And irrespective of the tariffs or how the prices move, institutional players don't prepone their buying. It's the distributors who resort to stocking. So, in exports, we didn't see any kind of pre-stocking because of whatever tariffs or copperrelated movement or any of that sort. All of this is pretty much execution of the order book that we had.”

— Chirayu upadhya, Head of Investor relations , Polycab India.

Premiumisation & Solar SKUs in products to lead the Fmeg margins acceleration

“Solar is a profitable business for us, and that will continue to be the case. The other products that we have in the FMEG segment, which are switches, switchgears, conduits, all of them are profitable. Perhaps one of the segment that we would want to be profitable in the near to midterm is the Fans segment. Over there, the utilization rates continue to be at a bit lower and which is what is hampering our operating leverage and hence, the bottom line. As and when we scale up that business, perhaps that growth in terms of the bottom line in the FMEG business will see a material pickup. Over and above that, gross margin expansion as well based on the premiumization drive that we are undertaking across the product categories, that will be the other driver. We are also focusing on increasing the contribution of higher-margin products like switchgears and switches in the business. As and when that pans out over the course of next 5 years, again, that should be a booster to the bottom line of the FMEG segment. So, these are the 3 levers that we are working on to finish the journey from the current margins to 8% to 10% in the next 5 years”

—Chirayu upadhya, Head of Investor relations , Polycab India.

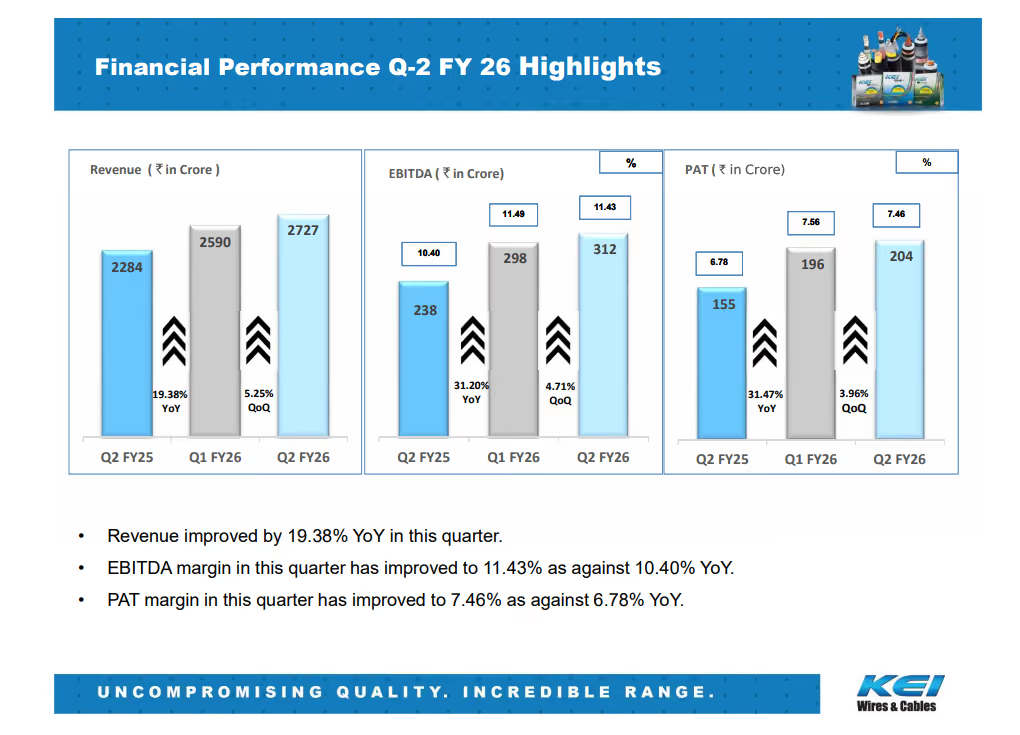

Sanand capex first phase to go live from November

“See, once full project is completed, we have estimated a revenue of around INR6,000 crores from the whole project. With the commissioning of first phase of this first phase in Sanand in November '25, around 50% of the capacity will come on board, which means around INR3,000 crores of new capacity will come on board, which will be gradually convert into revenues from the fourth quarter onwards and in the next financial year, because the capacity ramp-up and the stabilization of production will be gradual.”

— Anil gupta (Chairman & MD , KEI Industries)

Growth isnt a constrain but rather capacity is a constrain

“It's only a capacity constraint. That's why we are growing 18% to 20%. Now 15% to 20%, whether we can grow from domestic or we can grow from export or we can grow from retail. So it does not matter to us. Ultimately, we have to grow. Which market does not matter. It is not the clear that the demand is weak. Demand is very strong in the current market, because the other companies are also working in the same market. So everyone is growing.”

— Rajeev Gupta (Executive director , KEI Industries)

Commodity prices may fluctuate but it doesn't impact the margin profile of the company

“A lot of orders from the B2B segment have price variation clause available with us. So we don't get any you can see from our margins, EBITDA margins over the last 15 years, commodity price goes up and down, but our margins are not impacted because of the increase or decrease in the prices.”

— Anil gupta (Chairman & MD , KEI Industries)

Infrastructure and energy demand continues to persist given the Global tailwinds

“This business will continue to grow for the next several years because of the infrastructure demand and growth in the energy sector. Energy growth in the solar, wind and energy consumption sectors will continue to drive the demand of our products. You can see from the data that how much new capacities are planned in solar, wind, even thermal power generation, battery energy storage projects, which are linked with solar projects. And also the projects will be which will use this energy”

— Anil gupta (Chairman & MD , KEI Industries)

Focus remains to grow faster than Industry growth rates and gain market share and Invest in cables production capacities

“ of course we will achieve the better growth than uh industry average okay and in almost all the players in the industry right that they will be growing at 1.5x of the industry so what is our market share currently and what we are targeting in terms of future in 2 year down the line so uh I hope this industry is expected to grow at 13 14% because by thumb rule double of your GDP this industry grows and uh we are also since we are expecting a volume growth of 18% so it will be better than industry average and this we are uh trying to get uh through uh better product mix or new capex plan by investing in our cable business and uh at the same time wire will be remain in focus”

— Mahendrakumar Kabra ( MD, R R Kabel)

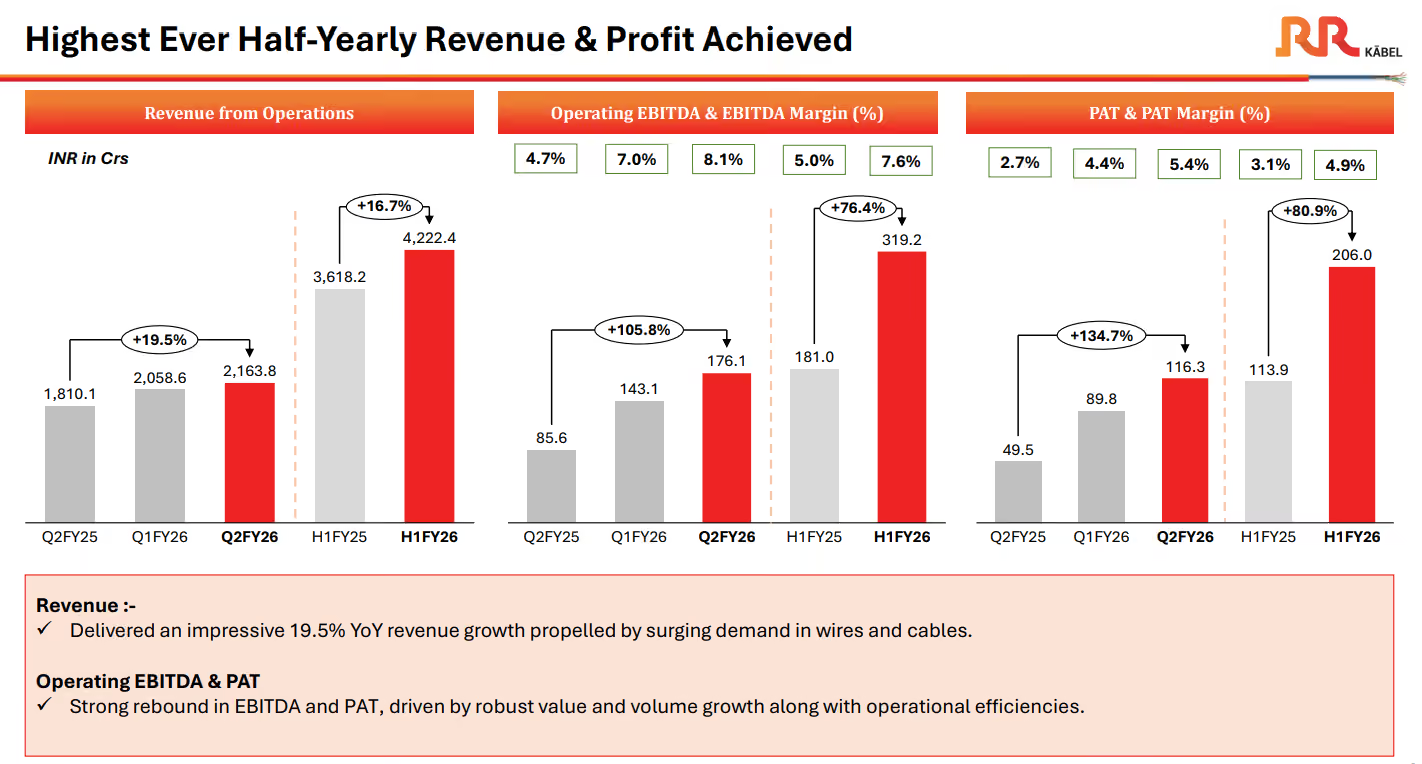

Margin acceleration every year and added with 18% volume growth are the catalyst for the company

“margins of 7.4% 4% in our wire and cable business and at the same time we had targeted to improve by almost 100 basis points and uh we are very happy to share that uh we have achieved this target in first half also at the same time uh uh now also we have our uh plan to improve this margins and maintain the volume growth and uh even uh to do and achieve our target of 18% volume growth”

— Mahendrakumar Kabra ( MD, R R Kabel)

Aims to get ebitda margin band towards 10.5-11% by Fy28 , with 100 bps expansion every year towards the same goal

“ Let's say fy27 and fy 28 in our long-term uh planning we have like targeted of having a bit margins in wire and cable in the range of 10.5 to 11% kind of margins uh by FI28 at the same time if you see we have targeted improvement of 100 basis points uh in this year and we are in line with our project”

— Mahendrakumar Kabra ( MD, R R Kabel)

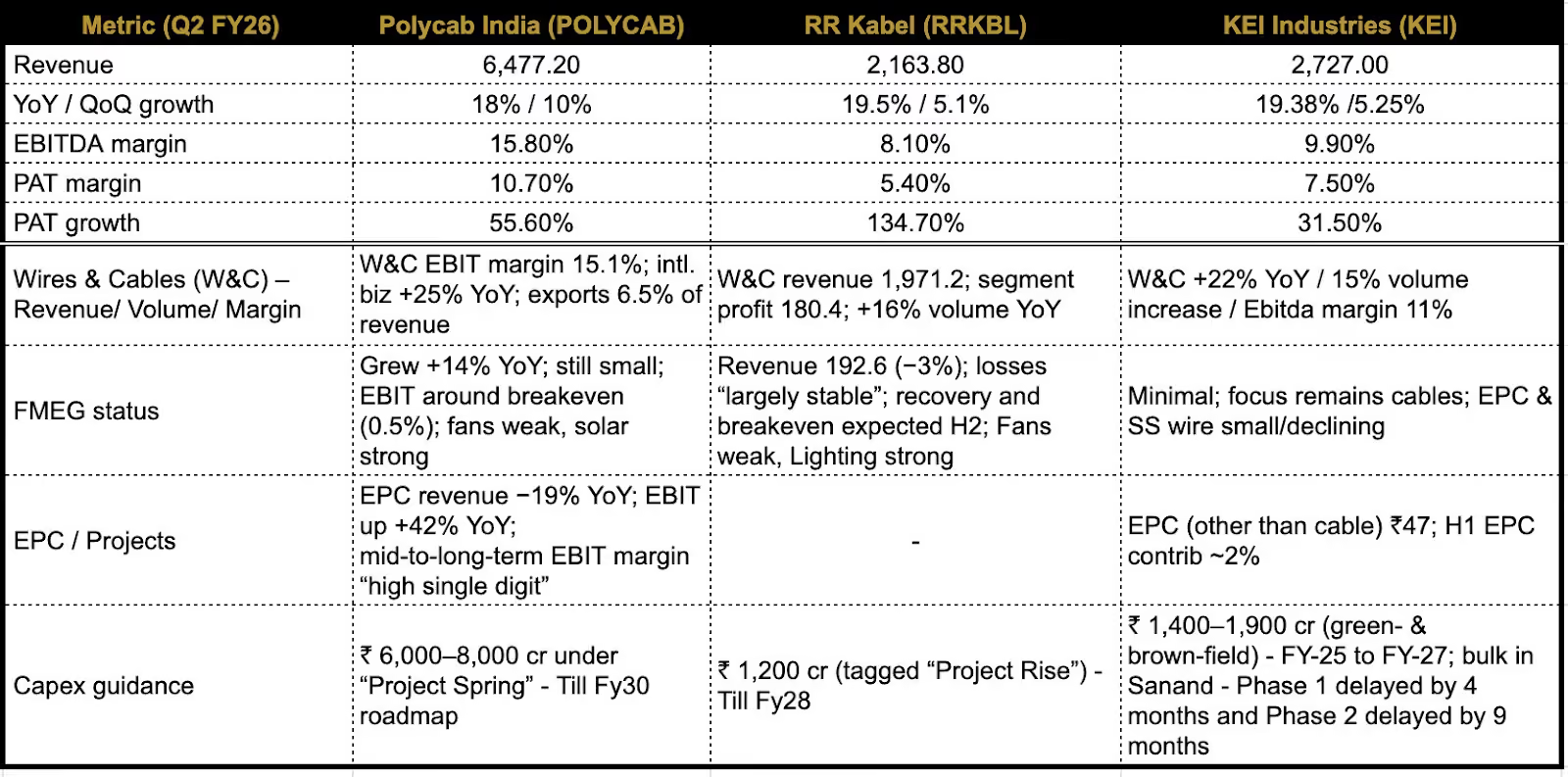

Based on the Q2 FY26 results and peer comparison of Polycab, RR Kabel, and KEI Industries, it is evident that:

Overall, Polycab outperforms in terms of volume and margin strength, while RR Kabel stands out for its impressive PAT growth. KEI shows consistent performance but with a more focused strategy on cables, especially in the near term. Each company continues to invest in expanding their EPC capacities, with Polycab and KEI making significant long-term capex plans to drive further growth.

Disclaimer - This is only for educational purposes and not a recommendation to buy or sell

.avif)

0 Comments