.avif)

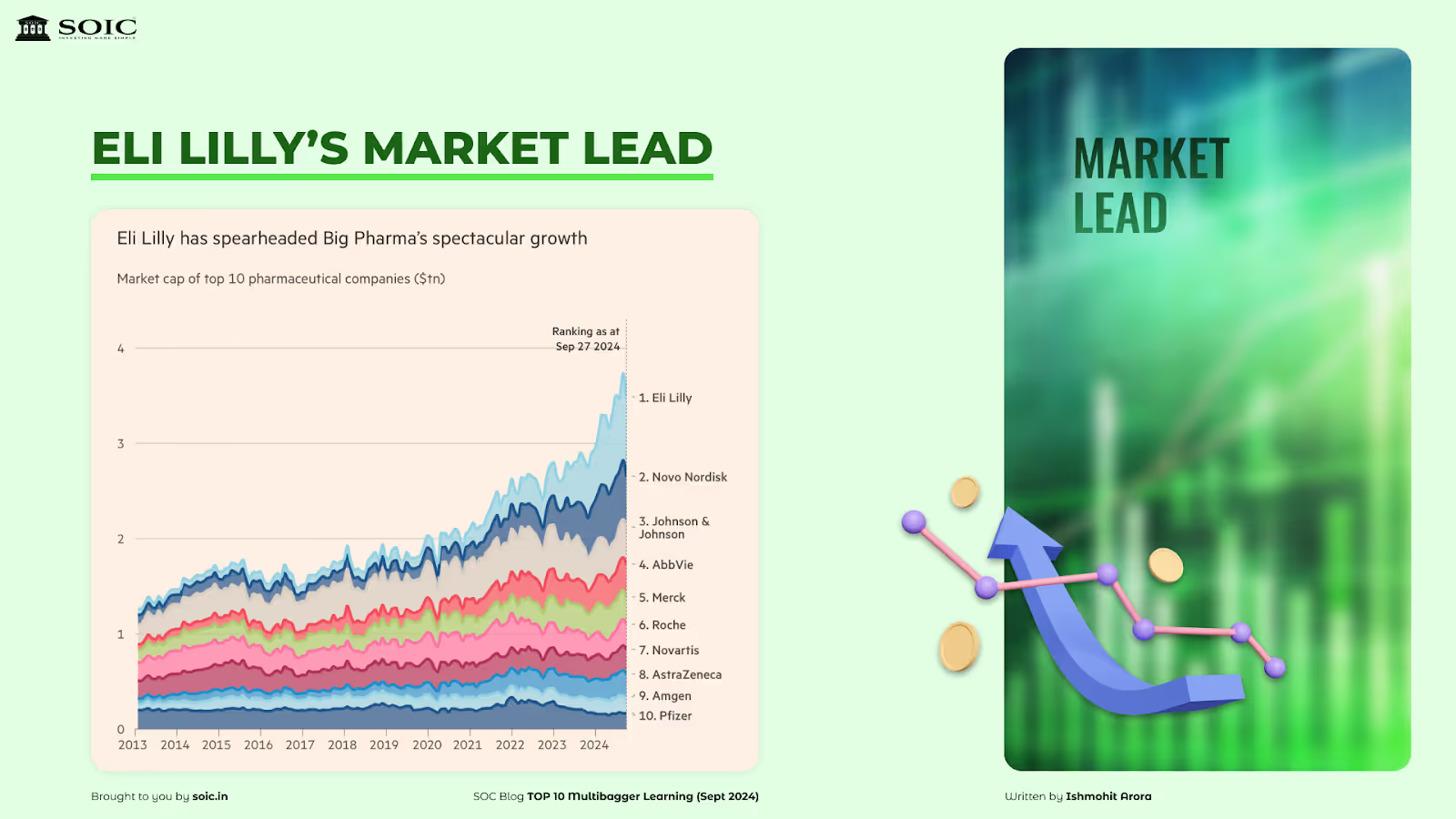

1. The sales of glucagon-like-1 peptide (GLP-1) drugs (weight loss drugs) are expected to double to $130 bn in 2030. This year the sales are expected to approach the $50 bn mark. 6% of the entire US population has been using these drugs. Obesity in the US has peaked out and started declining ever since these drugs were introduced. The following are some interesting facts about how this space is evolving:

A. GLP-1 drugs cause significant muscle loss along with weight loss. This has led to gyms in the US, making more space for strength training equipment vs cardio. Don’t be surprised with more weights or muscle training machines in the gym going forward (if you live in the USA).

B. There are more than 100 mn US adults with obesity and 1 bn people worldwide. ELI Lilly and Company are the manufacturers of the popular weight loss drugs such as Mounjaro (tirzepatide) and Zepbound (tirzepatide) have nearly touched a market cap of $1 trillion. These are the biggest pharma companies as per the market caps in the world; two of them are leading due weight loss drugs i.e. Eli Lilly and Company and Novo Nordisk.

C. This year, Mounjaro and Zepbound, which are both based on the active ingredient tirzepatide, are set to generate $18.8 bn in sales between them, according to analyst consensus estimates — edging closer to Novo Nordisk’s $27 bn in projected revenues from Ozempic and Wegovy, despite being on sale for a shorter period of time.

Sales from Eli Lilly’s GLP-1 franchise are projected to surpass Novo Nordisk’s by 2027. In 2026, Eli Lilly is about to launch an oral solid vs injectable form in which these drugs are currently injected. It can be a potential game changer as Eli Lilly will also enjoy a 2 year monopoly.

D. Indian companies from CDMO to formulations to EpiPens are involved in the value chain. The major role will start once these drugs start going off patent. A simple way to find such companies is to just click on Screener search and type: “GLP-1.”

2. I was recently listening to a podcast on What Makes a Rolex Special, a couple of interesting insights stood out:

A. “Rolex has its own foundry, not just the gold and other proprietary metals, even the steel on Rolex is proprietary and it’s made by Rolex. There are two Nobel prize winning scientists who are working in Rolex. They have created machines to test their machines that make watches. They have created a machine which can open and close a Rolex Clasp a thousand times a minute.”

B. Moreover, Rolex is owned by a foundation and its run as a non-profit entity. It is one of the most vertically integrated brands as they make everything in-house. This is what sets them apart to maintain their exclusivity.

3. KAVACH 4.0 has replaced KAVACH 3.2 in the upcoming tenders from the Ministry of Railways. Recently, the Rail Ministry has announced tenders for 10,000 locomotives and for 6,000+ km of tracks. 60-70% of the 28 tenders are expected to be awarded by December, followed by 44,000 kms worth of tenders to come by 2029, another 10,000 km tenders expected after tenders of 10,000 km. The size of the current tenders stand at 11,600 crores vs 1,500 crores of tenders which were announced in 2022.

Three major players are approved to bid for these tenders: HBL Power, Kernex Microsystem and Medha Servo Drives and two new entrants, i.e. RailTel and CG Power and Industrial Solutions.

4. Indians spend twice on weddings vs education. With 8 mn to 10 mn weddings held annually, India is the largest wedding destination globally. Estimated at $130 bn in size, according to CAIT, the wedding industry is nearly twice that of the US and is a vital large contributor to key consumption categories such as jewellery, apparel, catering, hotels (destination wedding), alcohol, etc.

Moreover, the wedding industry is seasonal with different days considered to be auspicious for marriage according to the Hindu Calendar. Typically, November to February are the months which have the maximum number of weddings.

5. I recently visited the Renewables Exhibition in Noida, I had three distinct observations post meeting the Industry Participants:

A. There is a massive oversupply which is going to come in Solar Modules, 2 years down the line. There is an Anti-Dumping Duty of 40%+ on import of solar modules, this has led to a lot of domestic production. In 2 years, the industry will cross 100 GW of production capacity; out of which 60% can be produced. The annual demand in India is 40 GW, industry participants are betting that the rest can be exported.

B. Due to domestic content requirements, players in solar cells are making abnormal profits. Abnormal profitability means EBITDA margins of 50-60%+. Cell manufacturing is technologically intensive and India still imports 95% of its solar cell requirements. Many module players like Goldi Solar, Waaree, Vikram, Solex, etc have announced plans to manufacture solar cells. Cell breakage will be a big factor in determining the quality and eventual margins when this cycle of abnormal profitability ends. Cells from China are imported at 4 cents per cell and cells made in India are selling at 14 cents right now. Such is the level of difference. Technology in cells keeps changing every 2-3 years, one has to be very careful with assessing players here if the technology they have is old.

C. The government is very supportive of localised manufacturing. Many government policies like ALMM, DCR, BCDs and a potential approved list of cell manufacturers have given birth to localised manufacturing of solar. Many players are trying to integrate and set up manufacturing capacities in Orissa; Orissa’s government is giving the highest subsidies. Most of the players in the exhibition were doing a fund raise or had closed one.

6. The biggest problem that solar or wind energy faces isn’t the lack of capacity, it’s the lack of transmission investments. Evacuating and transmitting the power from far away locations requires huge investments in the transmissions sector. This is what the National Electricity Plan wants to address. The Ministry of Power finalised the National Electricity Plan (NEP) for Central and State transmission systems, with a massive investment of ₹9.15 lakh crore. This plan aims to meet the growing energy demand, targeting a peak demand of 458 GW by 2032. This peak demand target exceeds the previous estimate of 380 GW.

Key features are:

A. The transmission network capacity will be expanded from 4.85 lakh circuit km to 6.48 lakh circuit km, and the transformation capacity will increase from 1,251 GVA (Gigavolt-Ampere) to 2,342 GVA.

B. Plans to set up nine higher voltage direct current transmission systems with a total capacity of 33.25 GW. The new capacities will nearly double the current operational capacity of 33.50 GW.

C. To increase the inter-regional transfer capacity from 119 GW to 168 GW by 2032.

D. Transmission schemes with an aggregate capacity of 50.9 GW have been approved during the first 100 days of Modi government's third stint, with a total estimated cost of Rs. 60,676 crore.

E. On Pumped Hydro Storage: India plans to add 39 GW of PSP capacity by 2030, in order to address storage and grid stability needs. Currently the installed capacity stands at 4.7 GW, with 6.47 GW under construction, and 60 GW under various stages of survey and investigation.

7. Out of Rs. 11.11 lakh crore of planned government capex, in the first 5 months of FY25, the government has spent only Rs. 3 Lakh crores. This is due to elections and monsoon led disruptions in the first 5 months of this financial year. The government will have to increase the speed of capex expenditure by 41% to meet targets, as the first five months have shown a contraction of 19% YOY in the government led capex.

8. In the USA, wealth managers and ALT asset managers have seen the fastest growth in their AUM and profitability vs the likes of mutual funds. I will urge all of you to study the business of Apollo Global Management to understand how this transition has played out globally. (It is at 13-14x PE and growing at 20% since the last many years+grabbing market share from banks in credit).

This podcast which can help you to understand this space deeply http://joincolossus.com/episode/panossian-a-primer-on-private-credit/

9. Diesel Genset Industry in India has transitioned to CPCB 4 norms.

What are CPCB IV norms?

CPCB IV+ emission standards represent the most recent and stringent environmental regulations set by the Central Pollution Control Board in India for diesel generators. These standards significantly elevate the requirements from the previous CPCB II norms, primarily focusing on reducing air pollution from DG setups.

A. The production of CPCB 2 genset has stopped post April.

B. CPCB 4 IV Gensets are less polluting and are priced at 30-40% higher than CPCB II Gensets.

C. Large players like KOEL and Cummins were ready with the CPCB IV portfolio much ahead.

A few insights on the CPCB IV norms from Motilal:

10. Last but not the least, we did a back test of all demergers in India since 2014 (excludes the ones that got delisted like Sintex). Here are the key results along with a special video on Demergers!

Link to the results: https://docs.google.com/spreadsheets/d/1Z8an9siILh8O--Ct9uNJIchKofXFjfD4yblwAFgvH3g/edit?gid=72858813#gid=72858813

Link to our Special video on Special Situation Investing!

https://www.youtube.com/watch?v=vPNBmG0URI4

Do let me know about your favourite learning in the comment section below!

Disclaimer: The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organisation, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

0 Comments