Time Technoplast: Betting on Composites and Packaging for a High-Pressure Growth Story

BY

Shuchi Nahar

Industry Trends

Manufacturing

The Plastics Powerhouse Evolving into a Composites Giant

In a world moving toward efficiency, light-weighting, and sustainability, Time Technoplast (TIME) is quietly building a powerful narrative. Already the world’s largest manufacturer of large plastic drums and the third-largest Intermediate Bulk Containers (IBC) player globally, TIME is now emerging as a leader in composite LPG/CNG cylinders — a sunrise sector with multi-decade tailwinds.

As industries pivot toward advanced materials and as India’s energy, chemical, and infrastructure sectors modernize, Time Technoplast’s transformation is not just a packaging story — it's an industrial evolution.

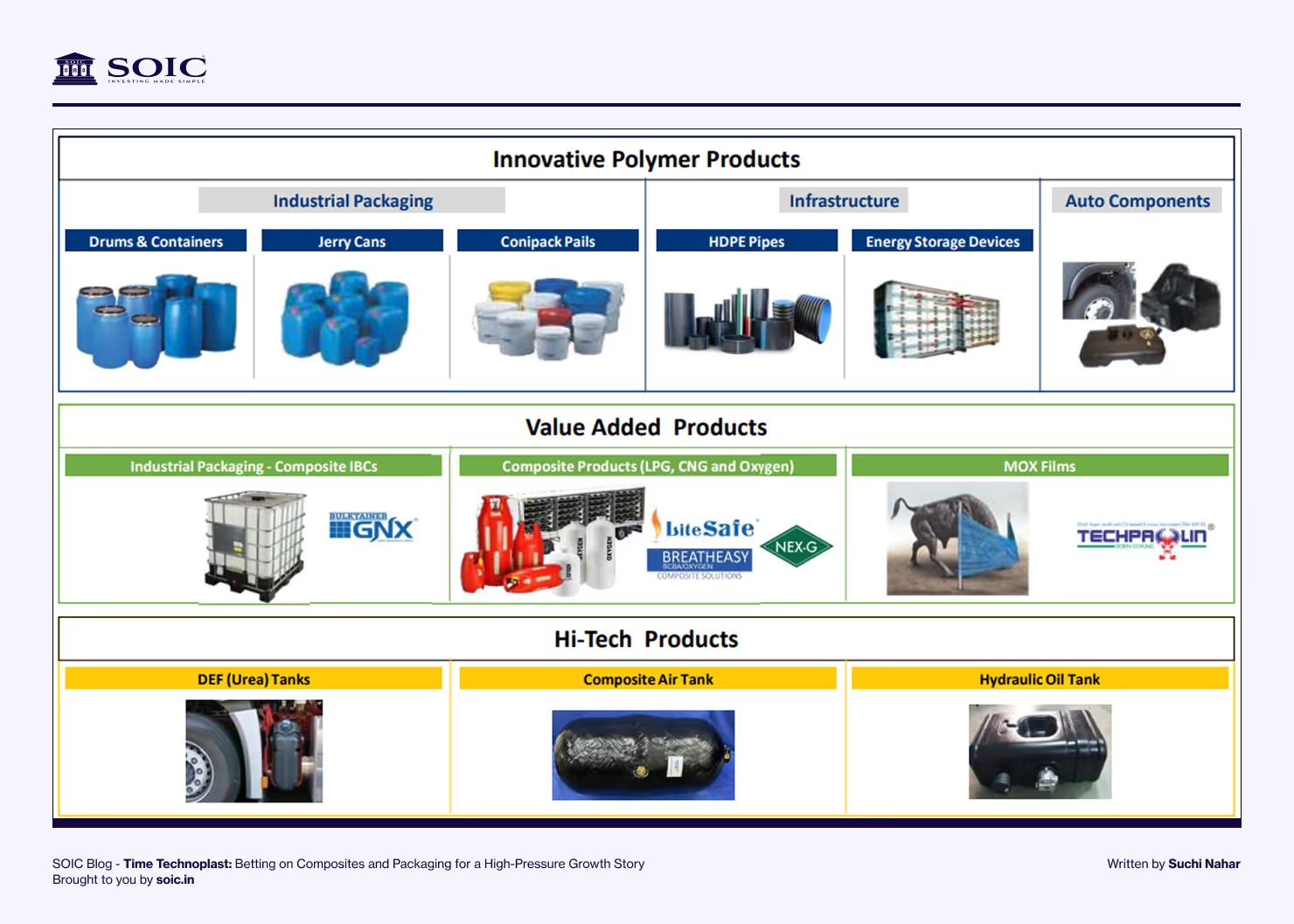

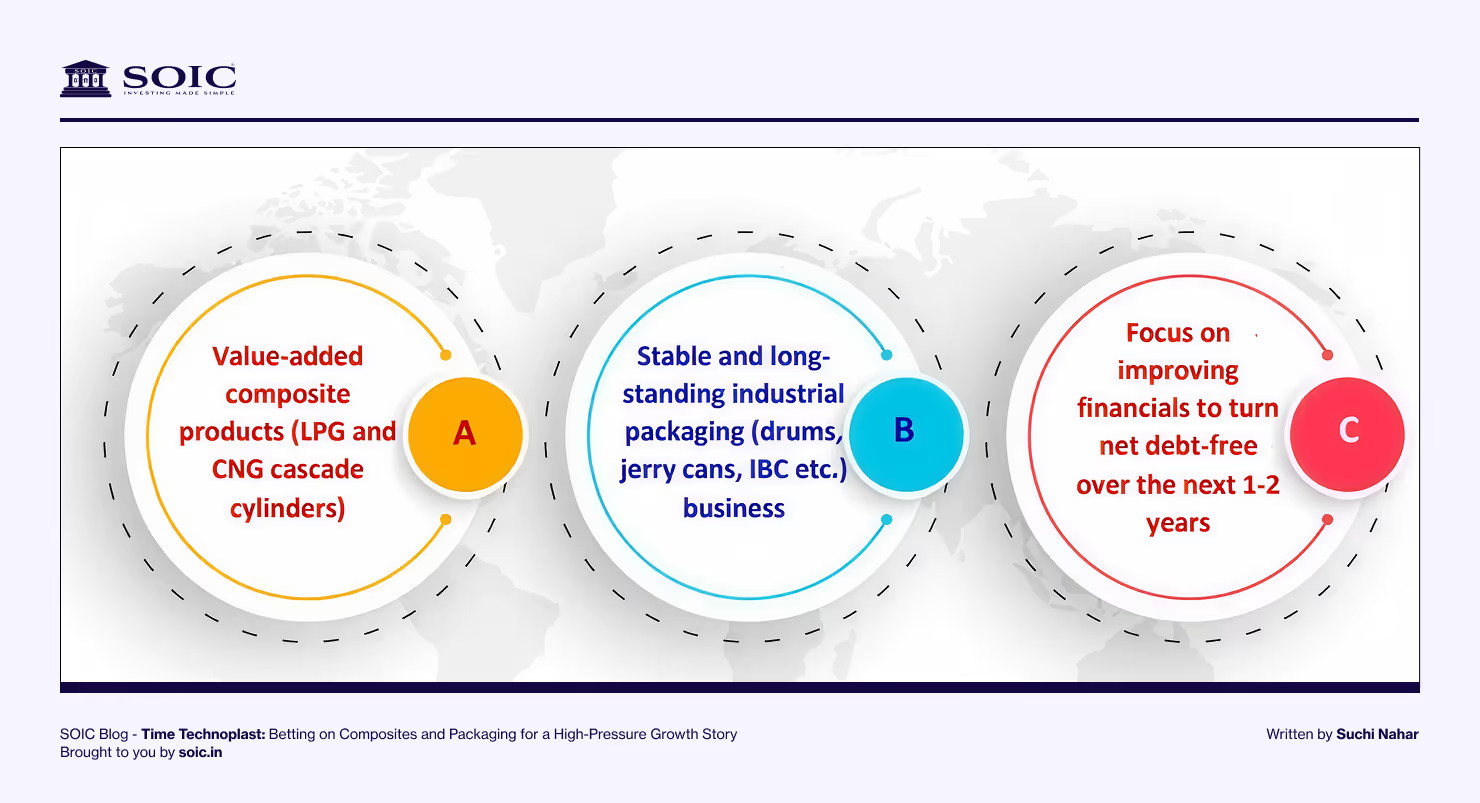

1. Industrial Packaging: Bread-and-Butter with Global Muscle

TIME dominates polymer-based industrial packaging in India with a 50-60% market share and strong positioning in 10 other countries. This “established products” segment (~73% of revenue) includes:

Drums, jerry cans, pails — critical for transporting chemicals, FMCG, paints, etc.

IBC containers — where TIME is a pioneer in India.

HDPE Pipes & Lifestyle Plastics — including turf, bins, and matting.

Despite being a lower-margin business (~13% EBITDA margin), its recurring demand, Fortune 500 client relationships (e.g., Dow, BASF, Shell), and deep B2B roots make it a steady cash engine.

2. Value-Added Products (VAP): The High-Octane Engine

TIME's real growth kicker lies in composite cylinders and IBCs, forming ~27% of FY25 revenues, projected to reach 35% by FY28 at a CAGR of 20-25%.

Why is this segment exciting?

a) Composite CNG Cascades: 30%+ CAGR Goldmine

Used in transporting gas from mother to daughter stations.

Clients include Adani Gas, MGL, IOCL, GAIL.

Composite cylinders offer 2.2x more gas per trip, 50% lower cost/kg than metal alternatives.

TIME expects revenue to double by FY28 (~₹8-10B).

b) Composite LPG Cylinders: Lightweight Disruptors

70% lighter than steel, safer, and corrosion-free.

Addressable market: 500M cylinders in India, 2.5B globally.

TIME currently has only 1.5M capacity—huge headroom ahead.

c) MOX Films and Specialty Products

Waterproof, UV-resistant films with industrial and agri uses.

Hydrogen & oxygen composite cylinders in R&D – future-ready bets.

These products command 18%+ EBITDA margins, enhancing TIME’s overall profitability.

3. Strong Financial Mojo: RoCE, FCF, and Net Cash in Sight

TIME is not just innovating — it’s doing so with discipline.

Revenue CAGR (FY21–25): 16%, expected at 15% FY25–28.

EBITDA Margin to expand from 14.4% to 15%+ by FY28.

Free Cash Flow: >₹4B/year; enough to fund capex and retire debt.

RoCE to jump from 18% to 23%+ by FY28.

Management plans to turn net cash by FY27, a rare feat in manufacturing-heavy sectors.

Monetizing non-core assets (~₹1.25B) and plans to divest its battery subsidiary NED Energy.

Setting up solar power and plastic recycling plants, improving cost structure and ESG appeal.

Restructuring plants for operational efficiency.

5. Valuation: Rerating Potential Still Untapped

Greater recognition of its VAP growth.

Institutional participation as debt falls.

Potential for exports-led growth in CNG and hydrogen cylinders.

Not Just a Packaging Company Anymore

Time Technoplast is transitioning from a commodity player to a value-added solutions provider. Its leadership in industrial packaging is now being complemented by high-growth, high-margin composites that align with global sustainability trends.

For investors betting on India's industrial evolution, alternative fuels, and lightweighting revolution — TIME might just be ticking in the right direction.

1. Strong FY25 Performance: Solid Base for a High-Growth Launchpad

Forex & Global Risks: 34% overseas revenue exposed to currency and policy changes; partly mitigated by global manufacturing.

A Multi-Themed, High-Conviction India Manufacturing Story

Legacy cash cow

High-growth, high-margin future products

ESG-aligned innovations

Global expansion optionality

Conservative capital allocation

Time Technoplast could become India’s answer to Hexagon Composites, and a dark horse in the green energy equipment theme. Time Technoplast stands today at a critical juncture—migrating from a legacy industrial packaging company to a high-margin, tech-enabled composites leader. Its story is one of foresight, execution, and adaptability.

This is not just a packaging company anymore. It's an energy transition enabler.

Disclaimer:

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

Industry Trends

Manufacturing

Market Trends

Stock Analysis

Author

Shuchi Nahar

Masters in Finance with 5 years of industry experience. My approach is to take one sector at a time and explore plausible Investment ideas.

.avif)

0 Comments