.avif)

Most business transformations don’t announce themselves loudly. They show up in smaller places — in how management answers questions, in where capital is being deployed, and in what is not being said anymore. Over the past few quarters, Pricol has begun to exhibit those signs. Not as a company chasing growth, but as one preparing itself for a longer, structurally different phase.

This note is an attempt to understand that transition — not through projections, but through intent.

More quiet confidence. As I went through Pricol’s recent annual disclosures and conference commentary, what stood out was not just the growth guidance, but the quality of growth the company is positioning itself for. This is not a story built on volume recovery alone—it is anchored in content expansion, platform stickiness, and structural industry tailwinds.

This blog is not about what Pricol was. I’ve already written about that phase earlier. This is about what Pricol is quietly becoming, and why that journey feels far more interesting than a loud turnaround headline.

When Pricol’s annual report is read alongside recent conference calls, the company’s future potential does not reveal itself through a single headline number or a bold guidance statement. Instead, it emerges through a series of deliberate choices—in product direction, capital allocation, and customer engagement—that collectively point toward a structurally different business than what Pricol was even a few years ago.

Rather than viewing this as a near-term growth story, it is more useful to analyse Pricol through three forward-looking lenses: how the product mix is evolving, where demand expansion is structurally supported, and whether capacity is being built ahead of that demand.

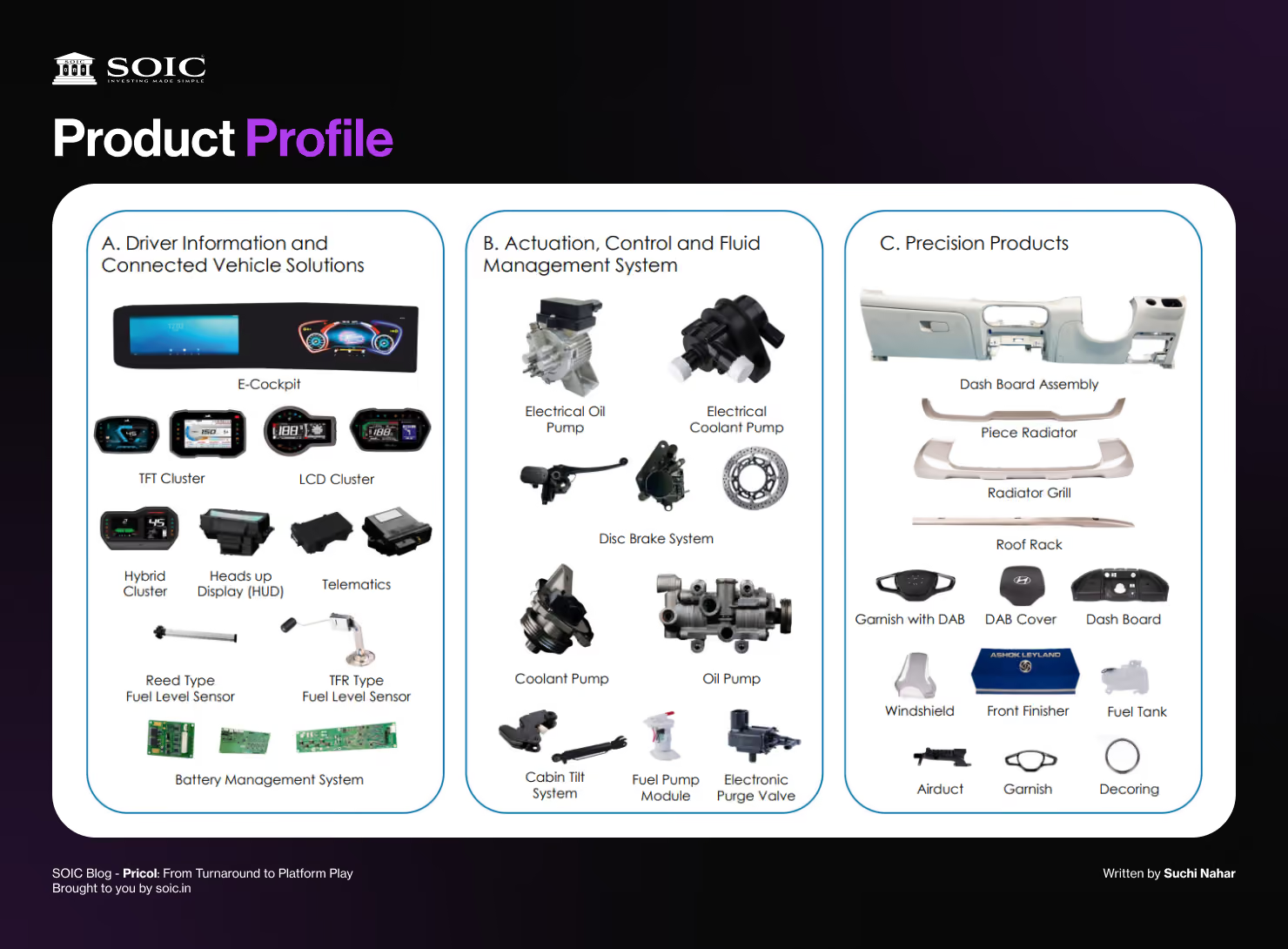

Pricol’s operations are now organised across three verticals—Driver Information & Connected Vehicle Solutions, Actuation & Fluid Management Systems, and Precision Products through P3L. While these verticals may appear diverse on the surface, they share a common strategic direction.

Across clusters, braking systems, pumps, plastics, and electronics, the company is steadily moving away from supplying isolated components and toward integrated systems and assemblies. This matters because system-level suppliers tend to enjoy:

This transition is also reflected in Pricol’s elevated R&D spend and its increasing focus on software-led interfaces such as digital clusters, connected platforms, and E-cockpit solutions. Over time, this has the potential to shift Pricol’s role from a cost-based vendor to a value-based partner for OEMs.

Several of Pricol’s emerging growth segments are supported not by cyclical demand alone, but by structural tailwinds.

One such example is disc brakes. With ABS regulations becoming mandatory from January 2026 across engine capacities, the addressable market for disc braking systems expands by design. Management commentary suggests that Pricol has already moved beyond pilot stages into production, including early EV applications and upcoming SOPs with large OEMs. Importantly, management has been careful not to overstate near-term numbers, instead framing this as a gradual, multi-year ramp.

A similar pattern is visible in handlebar control systems and switches, where Pricol has entered into an exclusive technology licensing arrangement. Here too, management has provided realistic timelines—indicating revenue visibility over the next 12–16 months rather than immediate scale.

In connected vehicle solutions and E-cockpit platforms, the opportunity is less about unit growth and more about increasing electronic and software content per vehicle. Once designed into a vehicle platform, these systems tend to remain for the full model cycle, offering both revenue stability and margin resilience.

Perhaps the most telling indicator of Pricol’s confidence in its future pipeline is its approach to capital expenditure.

Management has been explicit about maintaining capex levels of approximately ₹250–300 crore annually, with meaningful portions directed toward modernisation, debottle-necking, and expansion across both legacy and newly acquired businesses. This is not reactive spending. It reflects a belief that demand will materialise—and that being capacity-constrained at that stage would be more damaging than carrying higher depreciation today.

In the acquired precision plastics business (P3L), utilisation levels and land acquisition plans indicate that Pricol is not merely improving margins, but actively preparing the platform for customer diversification and scale. This suggests that the acquisition was not an endpoint, but a base for further expansion.

Pricol today operates across two core verticals—Driver Information & Connected Vehicle Solutions (DICVS) and Actuation, Control & Fluid Management Systems (ACFMS)—with over 5,200 product variants supplied across two-wheelers, passenger vehicles, commercial vehicles, and off-highway segments

What makes this important is not the breadth itself, but the direction of evolution. The company is steadily moving from mechanical components toward electronic, software-enabled, and system-level offerings. Digital clusters (LCD, TFT, hybrid), connected cockpits, disc brakes with ABS compatibility, and electric coolant pumps are all examples of this shift.

Content per vehicle is not a headline number—but over time, it becomes the most reliable driver of compounding.

The Indian auto industry is undergoing a visible premiumisation cycle—across motorcycles, scooters, and passenger vehicles. Entry-level segments are shrinking, while feature-rich models are gaining share. This directly benefits suppliers like Pricol, where the average selling price of digital clusters is already 3–4× that of mechanical clusters, and management expects this to rise further as TFT adoption accelerates

One of the more underappreciated drivers is Pricol’s entry into disc brake systems, with commercial supplies already underway to six OEMs. From January 2026, ABS becomes mandatory across all two-wheelers irrespective of engine capacity, structurally expanding the addressable market

For a relatively newer entrant, this regulation creates a rare opportunity: OEMs actively seek alternate, localised suppliers to diversify risk and ensure capacity readiness.

The acquisition of Sundaram Auto Components’ injection moulding business (now housed under Pricol Precision Products Ltd – P3L) deserves special mention. This business reported ₹842 crore revenue in FY25, with margins improving meaningfully post-acquisition as utilisation ramped up to ~95%

More importantly, this is not just a margin story. The acquired platform allows Pricol to:

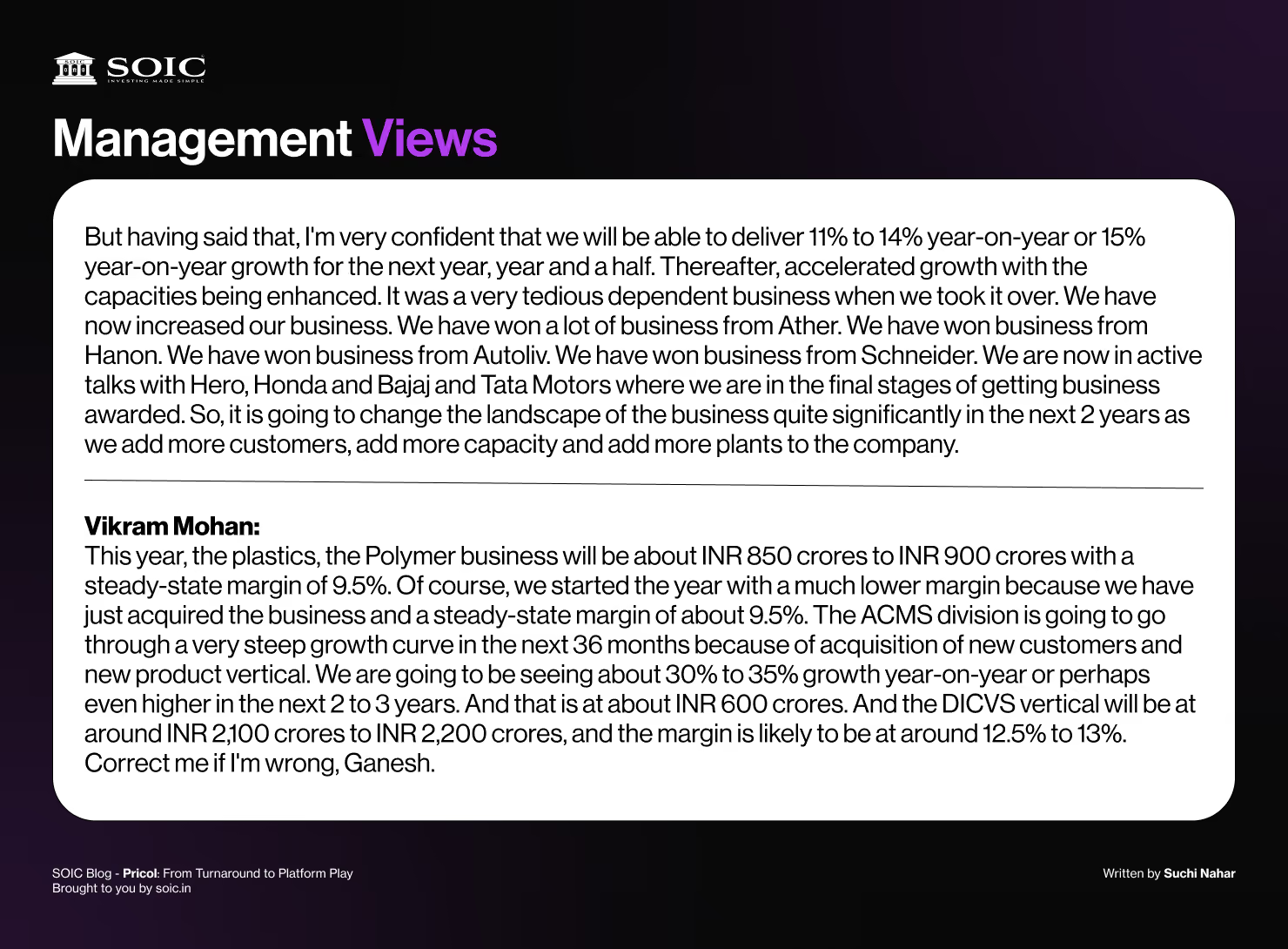

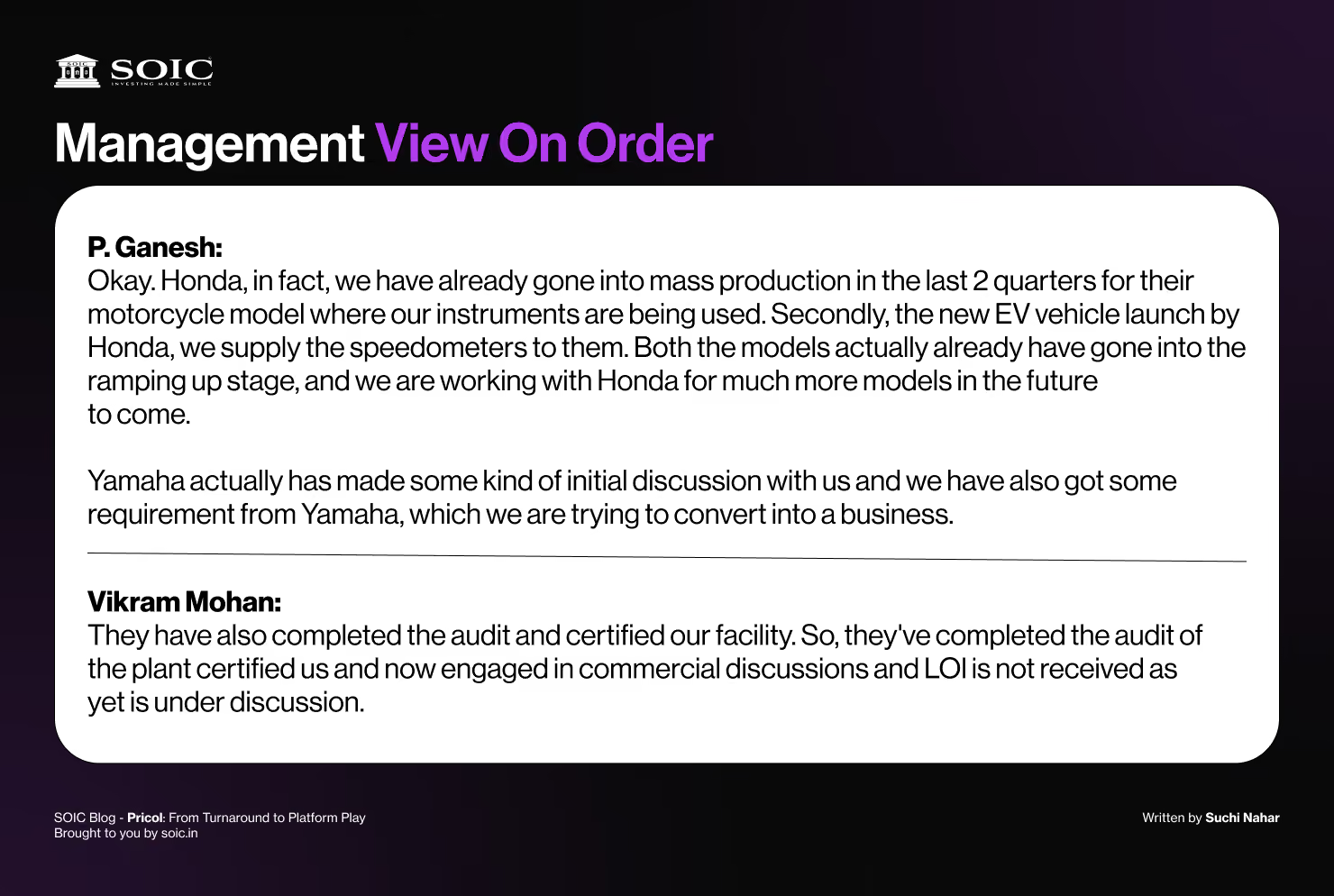

Recent order wins from Ather Energy, and Tier-1s such as Autoliv, Hanon, and Schneider, indicate early success. Management commentary also suggests a visible pipeline with Hero MotoCorp, HMSI, Bajaj Auto, and Tata Motors.

Unlike many auto ancillary stories that hinge entirely on EV adoption, Pricol’s portfolio is largely powertrain agnostic. Digital clusters, disc brakes, cockpit systems, and several actuation products find relevance across ICE, EV, and hybrid platforms. Even within fluid management, Pricol’s electric coolant pumps cater to EV thermal management needs

This design choice reduces binary risk and allows the company to participate in EV growth without betting the franchise on it.

Pricol continues to guide for ₹250–300 crore annual capex, largely funded through internal accruals. This capex is being deployed toward:

The balance sheet remains lean, with net debt under control—suggesting growth without financial stress

Good businesses talk about orders. Great businesses talk about platforms.

Pause for a moment — how often do we confuse fixing the past with building the future?

When I listen to Pricol’s recent concalls, I don’t hear management celebrating past fixes. There is very little chest-thumping about margin recovery or growth percentages. Instead, the tone feels… calm. Almost impatient to move on.

That tells me something important: The turnaround phase is mentally over for them. What follows after that phase is usually harder — building something durable.

On paper, the P3L acquisition can be explained in one line:

“Lower-margin plastics business acquired, margins improving steadily.”

But when I read the concalls closely, that framing feels incomplete.

This didn’t sound like a financial turnaround.

It sounded like Pricol transplanting its operating discipline into another body.

Plastics here are not the end product. They are a bridge — a way to increase content per vehicle and participate deeper in the OEM ecosystem.

Sometimes the most important part of a business is not what it sells, but where it sits in the value chain.

That’s a very different mindset from running a standalone injection moulding business.

One sentence from management keeps echoing in different forms across calls: “We are moving from mechanical to electromechanical to electronics and now integrated systems.” When I see this alongside their capex plans, R&D spend, and product launches, the picture becomes clearer.

Pricol isn’t chasing growth by adding more SKUs.

It’s doing something more patient:

In auto ancillaries, this is where real pricing power quietly builds.

The ABS regulation: preparation beats prediction

They weren’t forecasting windfall gains. They were talking about:

That matters. Regulations don’t reward excitement. They reward prepared incumbents.

The fact that Pricol is already supplying disc brakes, already testing systems, already thinking in terms of multi-year ramps — that tells me they are positioning themselves before the regulation fully plays out.

Rare earth magnets. Semiconductor shortages.

Most companies use these moments to explain weak quarters.

What caught my attention in Pricol’s calls was the emphasis on response:

This is a subtle shift — from being a vendor to being a problem-solving partner. In cyclical industries, this difference often decides who survives cycles with dignity.

One thing I personally watch very closely is how management talks about capex and depreciation. Pricol doesn’t sound defensive about rising depreciation. There is no attempt to dress it up.

The message is simple:

That clarity gives me comfort — not because risks don’t exist, but because decisions appear deliberate, not reactive.

The mental model I now use for Pricol

I no longer see Pricol as:

I increasingly see it as a mobility technology platform with multiple option legs.

Each new vertical doesn’t just add revenue — it adds:

Platform stories rarely look exciting quarter to quarter. They reward patience.

No story is without risks, and this one is no different:

But these feel like execution risks, not structural fragilities. That distinction matters.

What to track:

In essence, Pricol’s growth visibility is not in disclosed order book numbers — it is embedded in where the company is choosing to invest capacity.

They unfold quietly — through conference calls, capex decisions, and the tone management uses when things go wrong.

Pricol’s story today is no longer about recovery or near-term growth cycles. It is about quiet repositioning — moving up the value chain, expanding content per vehicle, and embedding itself deeper into OEM platforms.

The absence of loud guidance or headline order book numbers is, in some ways, the point. Instead, intent is visible through SOP wins, capacity decisions, and sustained investment in systems rather than standalone components.

If execution continues along this path, Pricol may not emerge as a sudden surprise. It is more likely to evolve into a steady compounder, built on relevance rather than scale alone.

The information provided is for educational purposes only and should not be considered investment advice. We are SEBI-registered research analysts.

We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

.avif)

0 Comments