%2016_9%20(2).png)

Welcome to Investors’ Edge – your daily dose of business insights, trends, and updates that matter. In this space, we go beyond the headlines to explore the evolving world of companies and industries. Here we bring you thoughtfully curated insights, sharp observations, and key developments shaping the business landscape.

Welcome to the 28th edition of Investor’s Edge! This issue dives into the Q1 FY26 results of new-age internet businesses. We analyze how leading players in fintech, e-commerce, food delivery, and mobility are navigating growth, profitability, and strategic pivots. From revenue scale-ups to margin swings, we decode what’s working, what’s challenging, and the key triggers shaping their future trajectory.

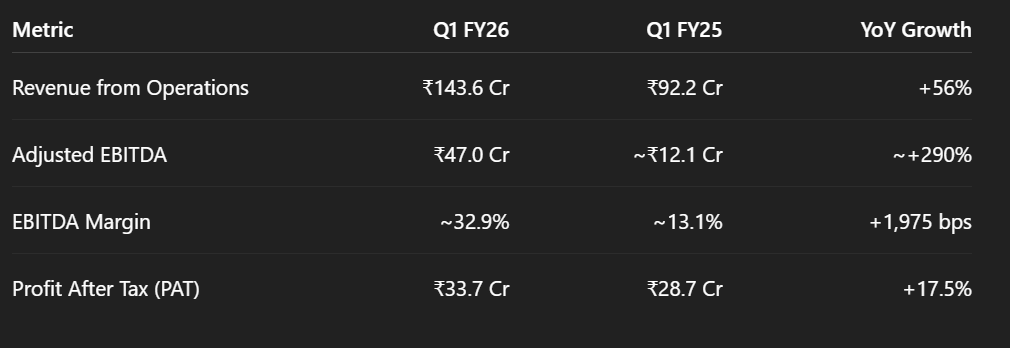

Blackbuck grew its overall revenue by 62.28% , with adjusted Ebitda growing by over 2.9x backed by strong cash flow generation and massive profitability lead by operating leverage

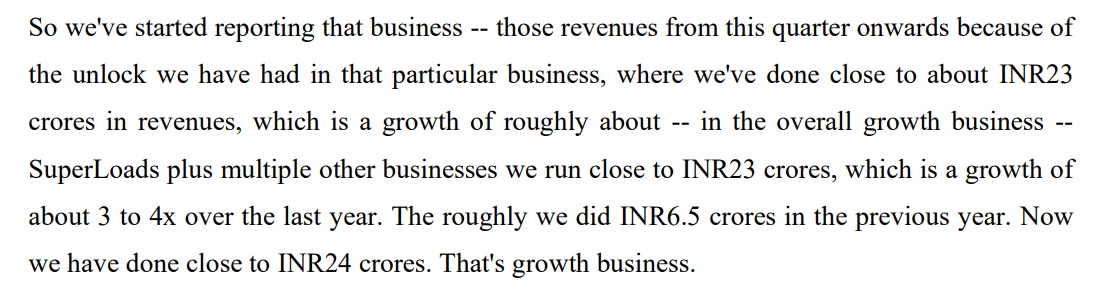

The newly introduced Superload’s business which acts as a market place for the truck load is growing on steroids with growth of 4x from 6.5 crores last year to 24 crores this year . And that's a very high value proposition for the customers . Its still in the nascent stage and has a huge TAM which is unexplored

Management says - “ I mean, basically, like if you have to draw a parallel, like probably it would be like a 2019 or 2020 of quick commerce where there's literally nobody doing anything in this space, right? That's point one. Point number two, is that the biggest competition in this market today is the market itself because it's a hard market to crack. We've been in this space for the last like 10 years. And the ability to build supply is very hard because of the demography of the customers. And like the places and the regions they need to really go into the build supply, and it's very costly, right? Most of the money we've invested is basically into building supply, prior to doing public, all our loss-making years but largely about building supply on the platform.”

Management says- “Basically, the whole -- first of all, the largest part of the revenue collection for the tolling networks, right, the government road networks come from the commercial vehicles, right? So the -- like it's obviously a risk, but then like the whole total collection going down, India can't build more roads, so I would only say that -- I see the risk as very minimal, but then, yes, I mean, nothing on the commercial that typically has been really altered by the government on this but then it's left to speculation.

Paytm turned the corner in Q1 FY26 with its first ever profitable quarter at Pat level as operating leverage, cost control, and merchant-lending growth lifted margins and PAT.

Management says - “ So it is strictly about current lenders that have existed previous quarter or previous to previous quarter, number one, which inherently inherits that the book has performed incredibly good for lenders to have their risk and comfort to be deciding because you know there were various clearances and clarifications that got issued. “

Management says - “With respect to EBITDA, so we're not doing adjusted EBITDA anymore. We're not doing EBITDA before ESOP costs. So of course, this is straight up EBITDA reported GAAP EBITDA. We do think that what we had said earlier about 15% to 20% EBITDA Margin over the next two, three years is still the number to drive towards. And that seems more achievable today than even a few quarters ago, because the contribution margin is very good, and we are seeing that keeping a tight leash on indirect expenses overall does still allow us to grow very well. “

Management says - “I do believe payment is a profitable business. Like you're seeing, without UPI, MDR, we are talking profits. And I do believe the payment channel is profitable and has operating leverage. We continue to push operating leverage by creating more solutions and value-adds on top of as basic as processing, if you will. And that's where the differentiation in the payment business comes. I continue to believe that payment standalone will be a bottom-line driver and a large bottom-line driver once these MDRs also show up. In effect, today we are calling breakeven and tomorrow we are going to call large profit from payment. That's why I keep saying, "focus on the core, we have a great business.”

Strong payments momentum (lifetime-high GMV; better gross margin) but consolidated losses widened as financial services remained soft and finance costs weighed.

Management says - “Our lending business, which was doing very well, Last financial year, after Q2, we had a downturn in line with the sentiment in the market and as you know, we've been reporting for the last two quarters that we are trying to recover that business. This quarter, we have shown 30% growth in the disbursal there, which is on top of a 30% growth in disbursal that we also reported last quarter. So, we are trying hard, and we expect the recovery to be even stronger in the coming quarters.”

Management says - “Overall, we are trying to grow our payments business, wallet and UPI. We are trying to recover our lending business. We have optimized all costs; you can see the contribution margin has improved. EBITDA has also improved in contrast to the last quarter, and we are well-positioned to deliver a strong year in terms of growth and achieving break-even EBITDA in the last two quarters of this financial year.”

Zomato delivered blistering topline growth in Q1 FY26 driven by Blinkit’s surge while consolidated profitability softened on continued quick-commerce investments.

Management says- “That's what we expect. In that timeframe, we should be able to move most of our business to inventory ownership and the margin accretion should also happen in that timeframe.”

But when we look at existing polygons versus new polygons that we open, most of the current growth has come from existing polygons. Even in this quarter when we opened a lot more cities, less than 5% of the overall growth came from the expansion areas that we were not serving earlier. Just to add, we have also mentioned in the letter that a city like Delhi, which from a geographical coverage standpoint is fairly well covered, we've seen a growth of 70% year-on-year in this quarter.

Solid start to FY26 broad-based growth with EBITDA up 46% and margin expansion; PAT up 79% on operating leverage.

Management says- “And lastly, on the right-hand side of the page, you'll see that in addition to on-platform and off-platform marketing, we also have the ability to target our consumers across WhatsApp, App Push, Emailer. So the fact that we can use all of these tools and use all these tools for a very large consumer base makes us a very, very strong marketeer, and that is a very important skill set for brands as they look to find a partner for India. Now just spending a minute on premiumization. As I said, both premiumization and penetration are 2 core objectives for Nykaa.”

Management says - “We have made significant progress in terms of the rollout and expansion of Nykaa Now. Today, we are present in across 7 cities, and we have over 50 rapid stores and almost 1.3 million plus orders have been delivered through Nykaa Now over the past several months since we launched Nykaa Now. So Nykaa Now, again, is part of our broader strategy of improving speed and convenience while not compromising on the quality of the product, the quality of the experience that we are providing to our consumers.

And so you can see that today, Nykaa Now is actually the largest assortment of beauty products in India are provided through Nykaa Now. So we have the largest assortment of beauty products available within 30 minutes to 2 hours' worth of delivery. And you can see that this business is scaling sustainably, and it is also getting a lot of consumer traction in the 7 cities in which we are currently present”

CarTrade Tech (CarWale/BikeWale/OLX India) logged its best-ever quarter remarketing auctions and steady OLX India scale drove topline +22% YoY, EBITDA nearly doubled, and PAT +106% YoY with margin expansion.

Management says- “revenue from operations and total income is up 27% at INR199 crores. If you see our cost base is up by only 8%. And normally, as you know, all our increments are done in the first quarter. This cost increase, which we see in employee cost at 7%, we expect to be quite stable now for the rest of the year, considering all the increments are factored in, in the first quarter this year. EBITDA is up 98% as a result of the leverage in the business, as you can see. And EBITDA margin has gone to 25% on a consolidated basis from 15% a year ago. So margins continue to grow”

Management says - “If you look at the businesses itself, the consumer group has grown by 32%, which resulted in a 79% growth in profit and achieved a 29% EBITDA margin, which is getting close to a benchmark for the entire industry. Our remarketing business has gained momentum and delivered a 36% growth, which has led to almost 258% growth in profits, growing the leverage in the business. And OLX has achieved its highest ever revenues with a 71% surge in its profits.”

Swiggy’s Q1 FY26 was marked by accelerating revenue traction (especially from Instamart and supply chain), but profitability pressure persisted as rapid scale investments and cost inflation deepened losses

Management says- “Our GOV growth accelerated to 108% YoY. This was primarily led by our dark-store expansion, both existing and in the new areas that we went into. As we have also spoken in the past, the average order value is a very important determinant of the profitability of the business. I am happy to report that our focused efforts have led to a substantial change in the slope of the driving AOV, with a movement of 16% quarter-on-quarter and 26% Y-on-Y which is ahead of our guidance that we gave

This combined with letting go of some of the low AOV orders led to a moderation in our order growth quarter-on-quarter.”

Management says- “ So, our guidance remains that we expect to get to contribution margin neutrality between December and June quarter of calendar year 2026. And towards that, while we made 100 basis points improvement in the previous quarter, we actually expect to make an even higher contribution margin improvement in the current quarter”

Management says- “See, if you are comparing it to the JFM quarter, yes, it has gone down, but at an absolute level the intensity in the market, we see it being at the heightened level. There are new players also entering the market. Some of them are taking baby steps into these markets as well. So, overall, we do not see this quarter as any indication of whether the competitive intensity will go up or down. We believe that heightened level will remain and it is something that we are also baking on our plans.”

The Q1FY26 snapshot of India’s new-age internet businesses underscores the sector’s transition from hyper-growth to a more balanced focus on scale, profitability, and sustainable economics. Paytm’s return to profitability highlights the power of operating leverage and disciplined cost control. Zomato, while delivering blistering topline growth, reveals the trade-offs of aggressive quick commerce expansion, with profitability coming under pressure. Nykaa demonstrates a steadier path, where execution strength and category leadership continue to drive healthy margin gains.

MobiKwik and CarTrade, on the other hand, represent contrasting phases of digital evolution: MobiKwik navigating consolidation challenges in financial services amid widening losses, while CarTrade showcases operating leverage and integration benefits translating into record profitability.

Ultimately, the sector is no longer defined merely by GMV growth or customer acquisition, but by the quality of revenues, unit economics,path to profitability , strong built in operating leverage in business models and clarity of strategic direction. For investors, the critical lens is shifting from “how fast can they grow?” to “how well can they convert growth into durable profits and defensible business models.”

Disclaimer: The analysis and insights presented in this article are for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy, sell, or hold any security.

%2016_9.png)

0 Comments