%2016_9.png)

Welcome to Investors’ Edge - your daily dose of business insights, trends, and updates that matter. In this space, we go beyond the headlines to explore the evolving world of companies and industries. Here we bring you thoughtfully curated insights, sharp observations, and key developments shaping the business landscape.

Whether it's a strategic pivot by a market leader or an under-the-radar company making waves, we break it down for you — clearly, concisely, and consistently.

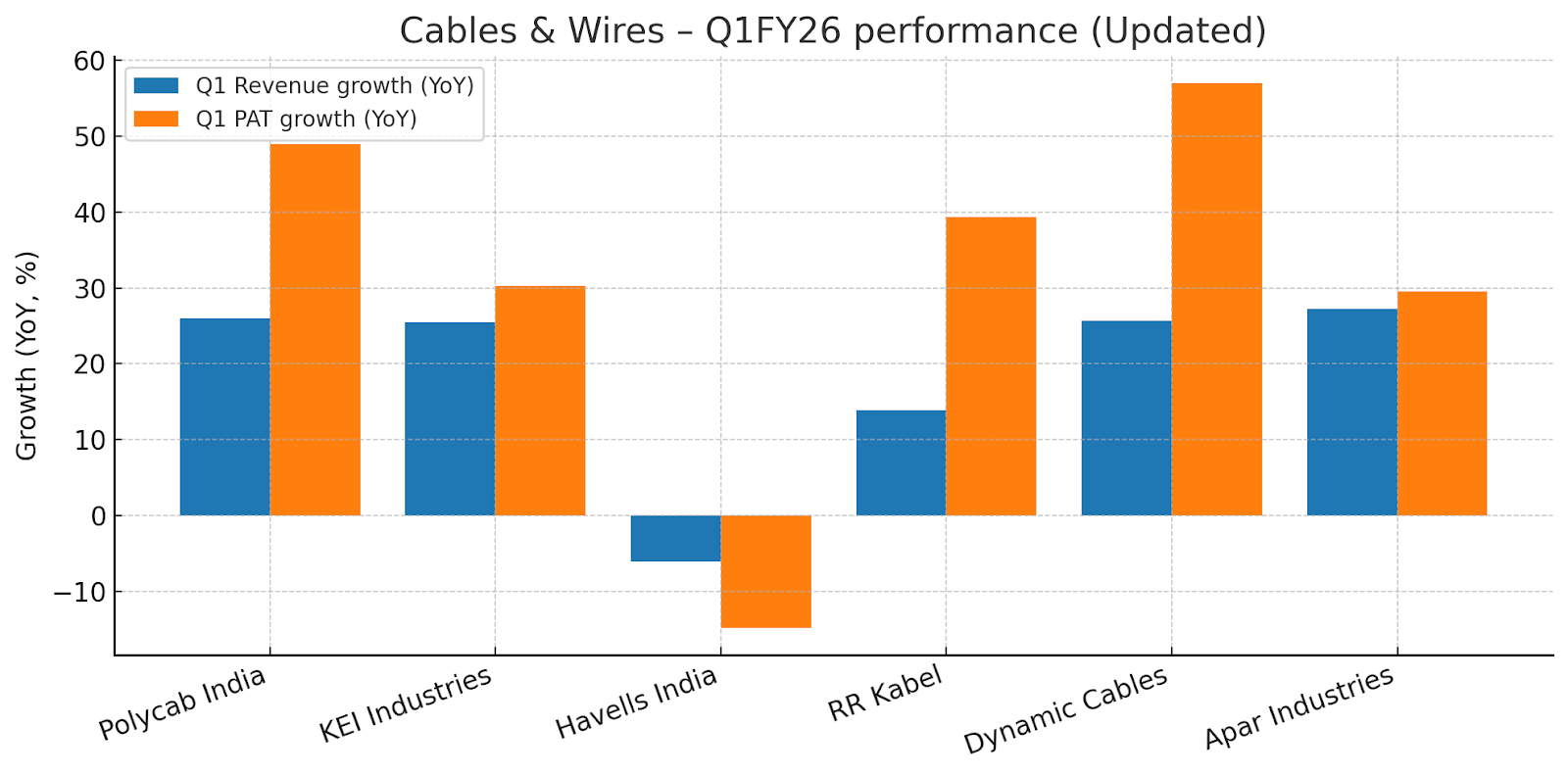

Welcome to the 22nd edition of Investor's Edge! This issue analyzes the Q1FY26 results and concalls of leading Cable and Wire manufacturers. We will uncover key insights from their quarterly performance, explore their significant capital expenditure plans, and identify the growth triggers that will drive their future expansion.

The Q1 FY26 period presented a mixed bag for the covered companies. While the Wires & Cables segment generally demonstrated robust growth driven by strong domestic demand, government infrastructure spending, and favourable commodity prices, the FMEG segment faced headwinds due to seasonal factors (early monsoon affecting cooling products) and subdued consumer demand.

Exports, particularly to the US, are a point of uncertainty due to evolving tariff situations, but companies are actively diversifying their international presence. Capacity expansion and operational efficiency remain key strategic pillars to capitalise on anticipated long-term demand.

All companies highlight strong tailwinds from government infrastructure spending, real estate, and electrification efforts

Polycab also notes

"strong tailwinds from infrastructure spending, improving private sector investment, and momentum in the real estate sector."

RR Kabel states their business

"continued to benefit from sustained demand across key sectors especially driven by infrastructure expansion, housing construction and increased electrification efforts nationwide.

KEI Industries also points to

"solar and renewable power development and data centers, transmission and distribution projects by power companies, whether in the government sector or in the private sector, electric vehicle recharging stations, infrastructures like railways, metros and tunnel ventilation projects."

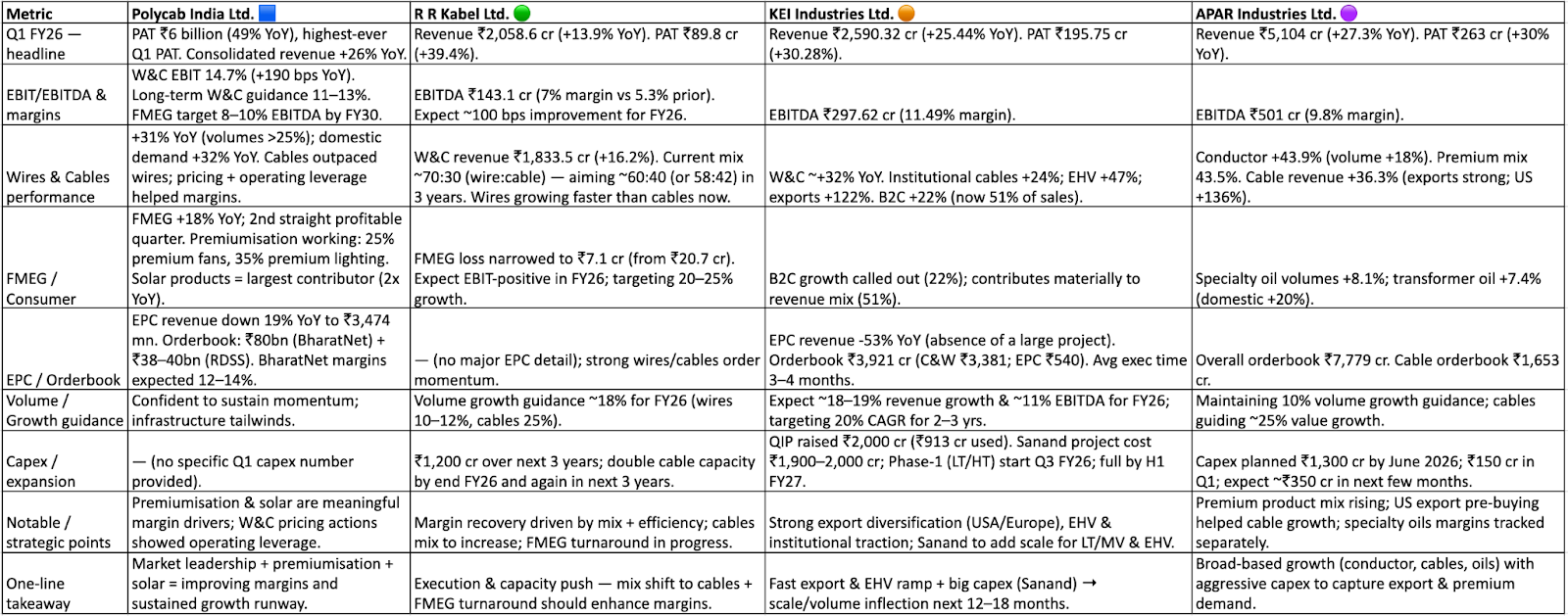

Domestic Market Strength - Domestic W&C business is a primary growth engine. Polycab reported "impressive 32% YoY revenue growth, driven by higher government spending, improved project execution and the favourable impact of rising commodity prices." RR Kabel’s domestic revenue grew "mainly due to wire business."

Also there was a very interesting insight from the RR kabel on how the margins vary across business segments i.e. Domestic wires vs Domestic cables and Export wires vs Export cables

“So it is in line with our earlier quarters only. As we have told in domestic wires, we have higher margins while in domestic cable, we have less margin because I have a very low base and my delivery cycle and still waiting time is a little bit higher. But once I improve the scale and then it will help me to improve the margins.

On export, it is another way around. Wire is considered a little bit simpler product so we have lesser margin while in cables we have higher margins and here we are improving our cable exports. So again, this will help me to improve my overall margins.”

Industry wide product mix shift towards cables from wires

Companies are seeing or anticipating a higher contribution from cables, especially in the domestic market, driven by infrastructure projects. RR Kabel expects "higher contribution from the cable segment in coming quarters," with a projected "25% growth in our cable business." Havells is "doubling our capacities in underground cables." Even Kei expects that “the growth in cable segment should be higher this year, but even wires will

also grow reasonably”

Also the case here is that larger players are continuing to gain market share with their wide distribution

Market Share Gains: Companies like Polycab (26-27% in organised C&W for FY25) and RR Kabel (expanding distribution in Tier 2/3 cities) are continuing to gain market share, attributing it to capacity, product bouquet, distribution reach, and a shift from unorganised to organised players.

KEI mentions "the industry itself is growing close to 12% to 13%. So it gets automatically adjusted."

Early monsoon brought some drought to the FMEG sales specially cooling segment

Early onset of monsoon significantly impacted cooling product sales (fans, ACs, coolers). Polycab’s "fans segment, while overall sales were muted due to shortened summer," and RR Kabel’s "Fan segment has underplayed due to early monsoon." Havells reported a "decline in cooling products revenue was more profound due to a strong base of last year."

The trend towards premiumisation is also present here where companies are pushing premium products to improve margins and resilience. Polycab's premium fans contributed "roughly 25% of the fan sales," and lighting premium products made up "over 35% of the sales." RR Kabel's premium fan products contribute "20% revenues from premium products."

Also to steadily increase the profitability of this segment companies are pushing towards better product mix, scale and operational efficiencies. Polycab’s FMEG business achieved its "second consecutive profitable quarter." RR Kabel "narrowed its segmental loss to INR7.1 crores" and expects to be "EBIT positive in FMEG" by year-end.

Chinese dumping not major risk in european geographies and Middle east has good infrastructure led demand

Polycab with a detailed dive on export markets

“Starting with Europe, very akin to the U.S., it is not very pro-China and they are looking at alternatives to Chinese products. So over there, even though Chinese suppliers offer a lower price compared to other suppliers, the end customers are still willing to pay a premium for non-Chinese alternatives. So, we are not seeing any dumping behavior at least in Europe.

Moving to the Middle East, again, it has huge demand for cables due to the significant investments happening on the infrastructure side. This makes the market open to various suppliers. Depending on what tariff situation is there in different countries, you are able to secure a lot of orders. For instance, we are doing a lot of supply to Saudi Arabia, where India enjoys a better tariff. Hence, we are not seeing as much of a competition coming in from the Chinese players.

Coming to Australia, Australia is where China likely has a competitive edge. They have worked a zero tariff treaty with Australia, which has resulted in most of Australia’s imports coming from China and that trend continues to be the case. Probably that is a geography where we will have to compete effectively on pricing terms or on other service terms and so on and gain a bit of market share through that. But in other geographies, I don't anticipate any dumping effect coming from China that would hamper our exports.”

Uncertainty in US

The evolving tariff situation in the US (e.g., 50% import duties on copper products) is creating uncertainty and causing some clients to "sit on the fence." Polycab notes that "Mexico, another large exporter, will have 30% of import duties effective from 1st August 2025" and "India stands at 10% right now." APAR highlights that "copper, which was previously zero, has also come into this 50% band" under Section 232 tariffs.

Diversification is the only strategy that will work in the current environment

Companies are leveraging their global presence and low-cost manufacturing in India to mitigate risks. RR Kabel has a "good order book from our all customers" and presence in "Europe and Middle East." KEI is not "too much worried about US impact at the moment," as its exports to other countries are "substantially high, especially Middle East, Australia, Africa and also Europe."

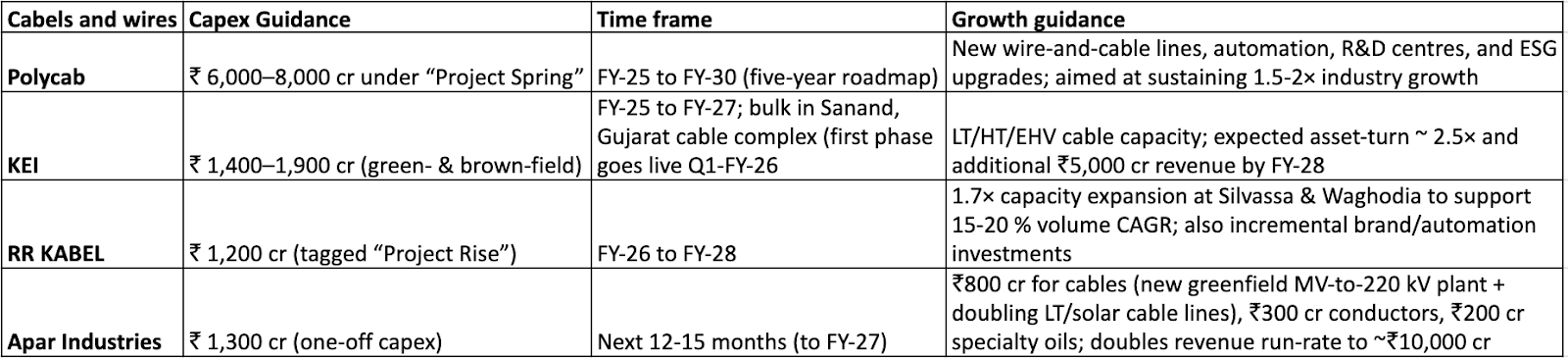

Significant Investments

All companies are committing substantial capital expenditure to expand capacities, primarily in W&C. Polycab targets "₹ 12 billion to ₹ 16 billion annually through FY30." RR Kabel's capex plan of "INR1,200 crores over next 3 years" aims to "doubling our capacity" for cables by the end of FY26 and doubling again in the next 3 years. KEI's Sanand project involves "Rs.1,900 crores to Rs.2,000 crores" capex, with Phase 1 commencing commercial production in Q3 FY26. Havells will be "doubling our capacities in underground cables" from FY24 to FY27, with an additional "CAPEX commitment of over Rs. 340 crores."

KEI also adds that the capex cycle will be continuous growth of 20% “But every year, we need to invest another Rs.600 crores to Rs.700 crores to increase the capacity to maintain the 20% top line”

Focus on Approvals

Especially for cables, approvals and certifications are crucial. RR Kabel states "since already we have got approvals from few of the utilities, now it is just keep that pace going and we'll keep adding approvals quarter-on-quarter basis."

Ramp-up & Utilisation

Companies anticipate gradual ramp-up of new capacities. KEI expects Sanand to take "3, 3.5 years" to reach full utilisation. RR Kabel is at "92%, 95%" capacity utilisation for cables.

The Q1 FY26 results for the Cable and Wire manufacturers paint a compelling picture of an industry poised for significant expansion. Driven by robust government infrastructure spending, sustained domestic demand, and a strategic shift towards higher-margin cable products, the Wires & Cables segment is clearly leading the charge.

While the FMEG sector faced some seasonal headwinds, companies are proactively adapting through premiumization and operational efficiencies, aiming for profitability.

Export markets, particularly in Europe and the Middle East, present promising diversification opportunities, even as the US tariff situation remains a point of caution. With substantial capital expenditure plans and a clear focus on capacity expansion and market share gains, these players are strategically positioning themselves to capitalize on India's growth trajectory.

The emphasis on approvals and efficient ramp-up of new capacities will be crucial in translating these investments into sustained growth.

Disclaimer: This blog post is intended for informational purposes only and should not be construed as investment advice. The views expressed herein are based on publicly available information and personal analysis, and do not constitute a recommendation to buy, sell, or hold any securities. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

0 Comments