There are some businesses that don’t move in straight lines. Their charts don’t slope diagonally from bottom‑left to top‑right. Instead, they bend, hesitate, dip, and then — suddenly — turn up with a force you wish you had seen coming.

That bend… that hesitation… that slow, painful grind before the explosive upward curve?

That’s the J‑Curve. And once you learn to see it, you can’t unsee it.

My first real encounter with this mental model was with HBL Power Systems. The company spent years building capabilities, sweating balance sheets, dealing with working capital cycles that would test a monk’s patience. But behind the scenes, something magical was happening — engineering depth, customer trust, and global credibility were compounding quietly.

Then suddenly… the curve turned.

Today, when I study Dynamatic Technologies, I feel the same energy. The same quiet momentum. The same deep manufacturing discipline. The same “we are building for 10 years, not 10 quarters” vibe.

This blog is about that journey. About the industries they operate in. About how large the opportunity really is. But more importantly, about why these companies feel like J‑Curve stories.

Let me take you through it — as if we’re both sitting with chai, pulling annual reports apart, connecting dots the market hasn’t reacted to yet.

Years ago, when I was new to the field and learning as an intern, I heard an old fund manager say:

“Real businesses don’t scale on Excel. They scale in factories.”

Back then, it didn’t fully register. Today, after tracking multiple industrial names that went from slow‑boring to multi‑baggers, I know exactly what he meant.

Manufacturing businesses grow like banyan trees — root systems underground for years before the tree bursts above the surface.

Before we go deeper into Dynamatic’s inflection, let me give you the most relatable J-Curve example from Indian markets — HBL’s Kavach.

HBL, for example, spent almost a decade cleaning up product lines, building engineering credibility in railway electronics, defence batteries, and missile power systems. Nothing happened on the stock chart. Nothing.

Then orders started converting. Margins started expanding. Cash flows improved. Debt reduced. Investor perception flipped.

Let me take you to a flashback of The HBL–Kavach Parallel: The Cleanest Way to Understand Dynamatic’s J-Curve

HBL built Kavach in 2004. Yes, twenty years ago. They engineered India’s train-protection system long before the country was ready for it. And for almost 18 years, nothing happened.

But the capability kept compounding silently — engineering, testing, refinement — even though the numbers didn’t move.

Then, 2021–23

Railway modernisation accelerated.

Safety became a national priority.

Tender frameworks have changed.

Suddenly, the same Kavach that sat ignored for years became mission-critical.

Demand exploded. HBL re-rated.

The payoff arrived decades after the work was done.

That is the J-Curve: Years of invisible preparation → Sudden, violent payoff.

This is exactly where Dynamatic stands today.

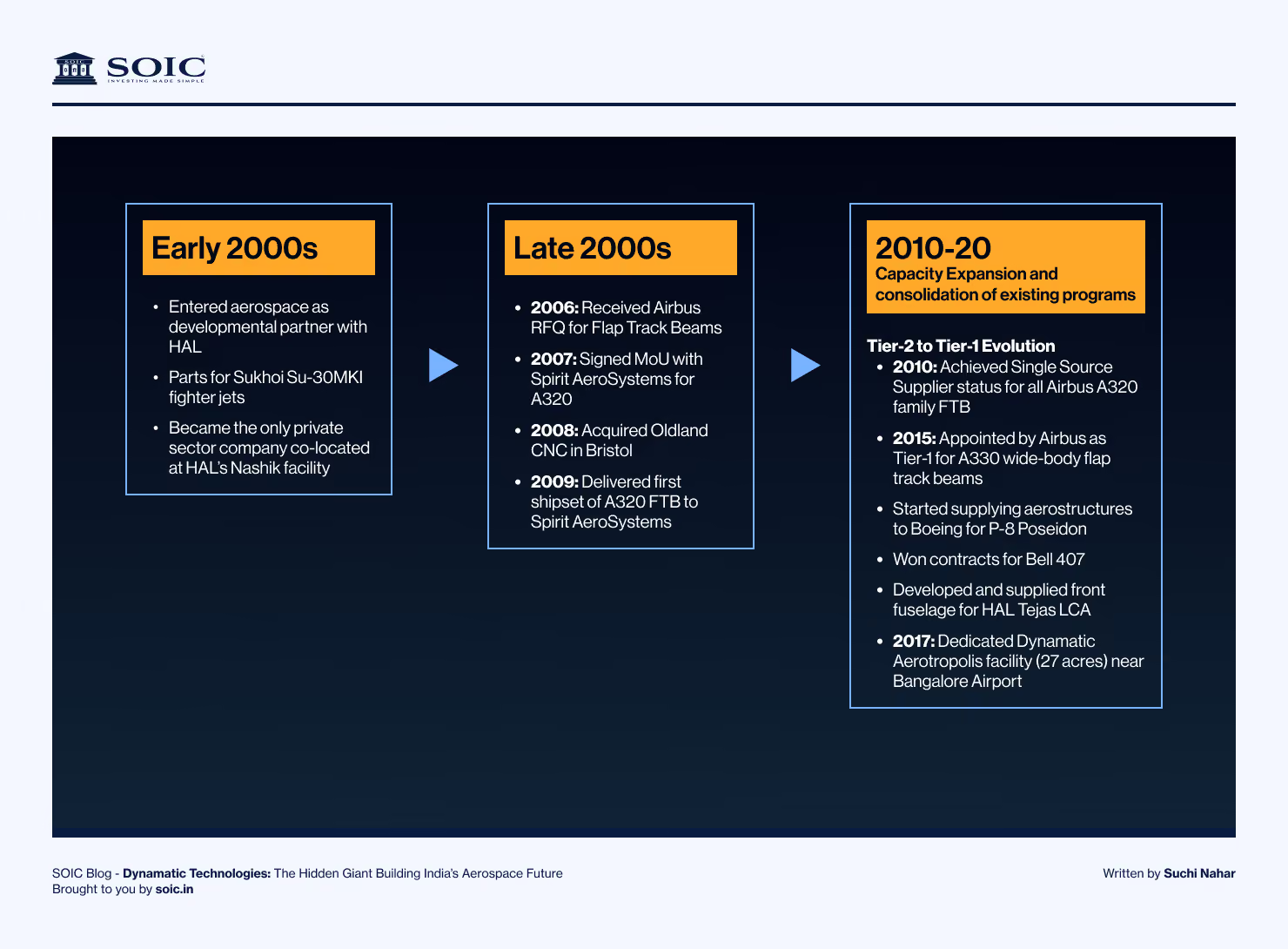

For nearly 15–20 years, Dynamatic was quietly building client relationships and capacities:

But what did the P&L show for 10 years? Flat numbers.

Just like HBL. Here’s the punchline:

Flat financials ≠ flat capability.

If anything, capability was compounding faster than ever.

Today — with A220, D328eco, Dassault, defence, UAVs, hydraulics restructuring, and global supply-chain localisation — the inflection signs resemble HBL right before Kavach’s breakout.

The J-Curve is a mental model investors love: you invest effort/capital at the start (down leg of the J), results look unimpressive or negative for some time, and then—once capabilities and scale align—returns accelerate (up leg of the J). Think of startups burning cash to build product-market fit, then scaling revenue once repeatability is achieved.

HBL Engineering is another real-world company that shares the J-Curve pattern: long capability build, followed by a structural re-rating when order flow and execution demonstrate repeatability. Like HBL, Dynamatic’s risk is execution-to-expectations; its reward is sustained program revenues and margin accretion once industrialisation is complete.

HBL Engineering comparison — why I mention it: HBL (an example many of you may know) went through capability accumulation followed by order wins that created a sustained re-rating. The common pattern is:

Dynamatic follows the same pattern: decades of engineering, then program wins (A220, D328eco, Dassault, Boeing programs), then industrialisation. If HBL’s re-rating was about converting engineering credibility to repeatable orders, Dynamatic is at the cusp of the same. The difference is aerospace’s higher barriers and longer qualification cycles — meaning both higher risk and higher reward.

Before we dig in the company, let’s zoom out. In the last three years, I’ve seen something unprecedented: global OEMs — from aerospace to heavy equipment — are treating India not as a low‑cost vendor, but as a strategic supply‑chain base.

Here’s why, the India Aerospace Components Market is already USD 13.6bn and is growing at ~6.5–7% every year.

India’s precision manufacturing isn’t a theme — it’s a movement. A shift. A structural re‑rating of the country’s capability.

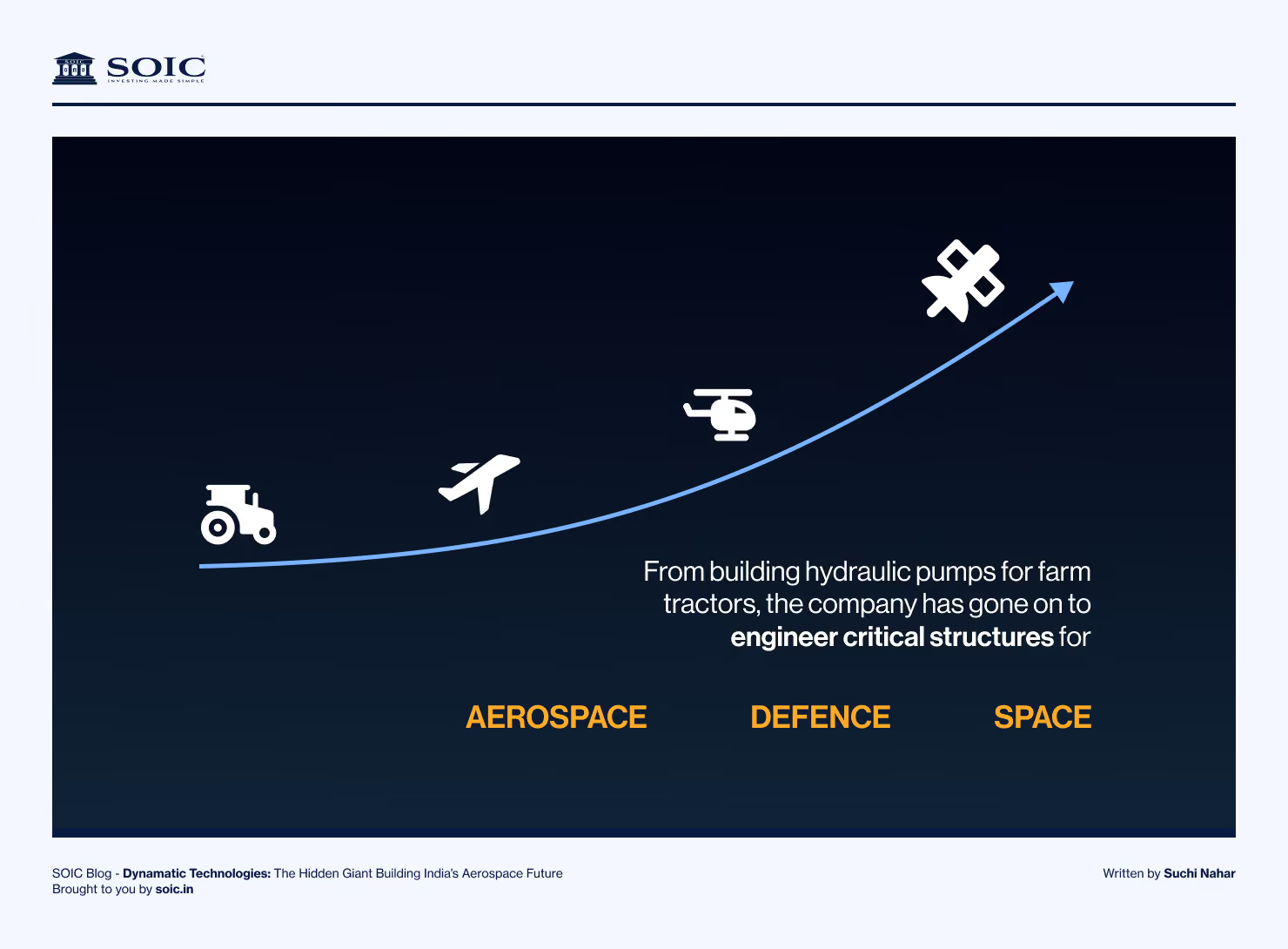

How I like to think of Dynamatic: from tractor pumps to flight-critical structures

There’s a myth in investing that manufacturing firms are “old world” and low-return. That’s lazy thinking. Dynamatic’s journey — from hydraulic pumps for tractors to flight-critical aerostructures and defence systems — is the opposite of low-return thinking: it’s about compounding technical credibility and customer trust in areas where failure is not tolerated.

If that reads as a long, careful climb, that’s because it was. Aerospace suppliers don’t get a seat at the table overnight — they earn it program by program, article by inspection, audit by audit.

Dynamatics has already created an ecosystem and built robust processes to enable the rapid scale up of their programs

Dynamatic takes raw metals (iron, aluminium, alloys), does its own casting, machining and assembly (even robotics and high‐precision operations), to serve three major verticals:

Defence – Dynamatics has gradually built strong capabilities in the entire defence segment and not just aerospace!

Dynamatic Technologies has successfully indigenised the complex Vertical Launch Unit (VLU) structure for the Indian Navy’s Long Range Surface-to-Air Missile (LRSAM) program. Building on this achievement, Dynamatic is currently executing an order for eight additional units, with deliveries scheduled to begin in August 2025.

Dynamatics is developing for BEL, has entered and is executing an order in the missile systems, has partnered Carmor to manufacture Armoured Vehicles and other Military Vehicles and is working on comprehensive Border Management & Physical Security Systems.

SPACE INSPIRE Program – Vertical Hoisting Device for Thales Alenia Space Dynamatic-Oldland Aerospace® has been awarded a prestigious contract by Thales Alenia Space France to manufacture a Vertical Hoisting Device for the SPACE INSPIRE next-generation spacecraft platform.

This precision-engineered mechanism, developed using aerospace-grade materials and complex actuation systems, reinforces Dynamatic’s capabilities in delivering mission-critical structures for space applications.

UAVs The company started developing capabilities in the security and UAV division since 2010…one of the first Indian players to enter this space.

DTL is nicely positioned in niche, high-engineering, high-barrier domains that benefit from structural tailwinds. The question is: how well is it capturing them?

In this section, let’s highlight what could drive Dynamatic from “good” to “great” — and what milestones to watch.

These milestones are important because aerospace components have higher margins, longer visibility, higher certification barriers (which provides moat). If DTL can push its aerospace mix higher, margins should improve.

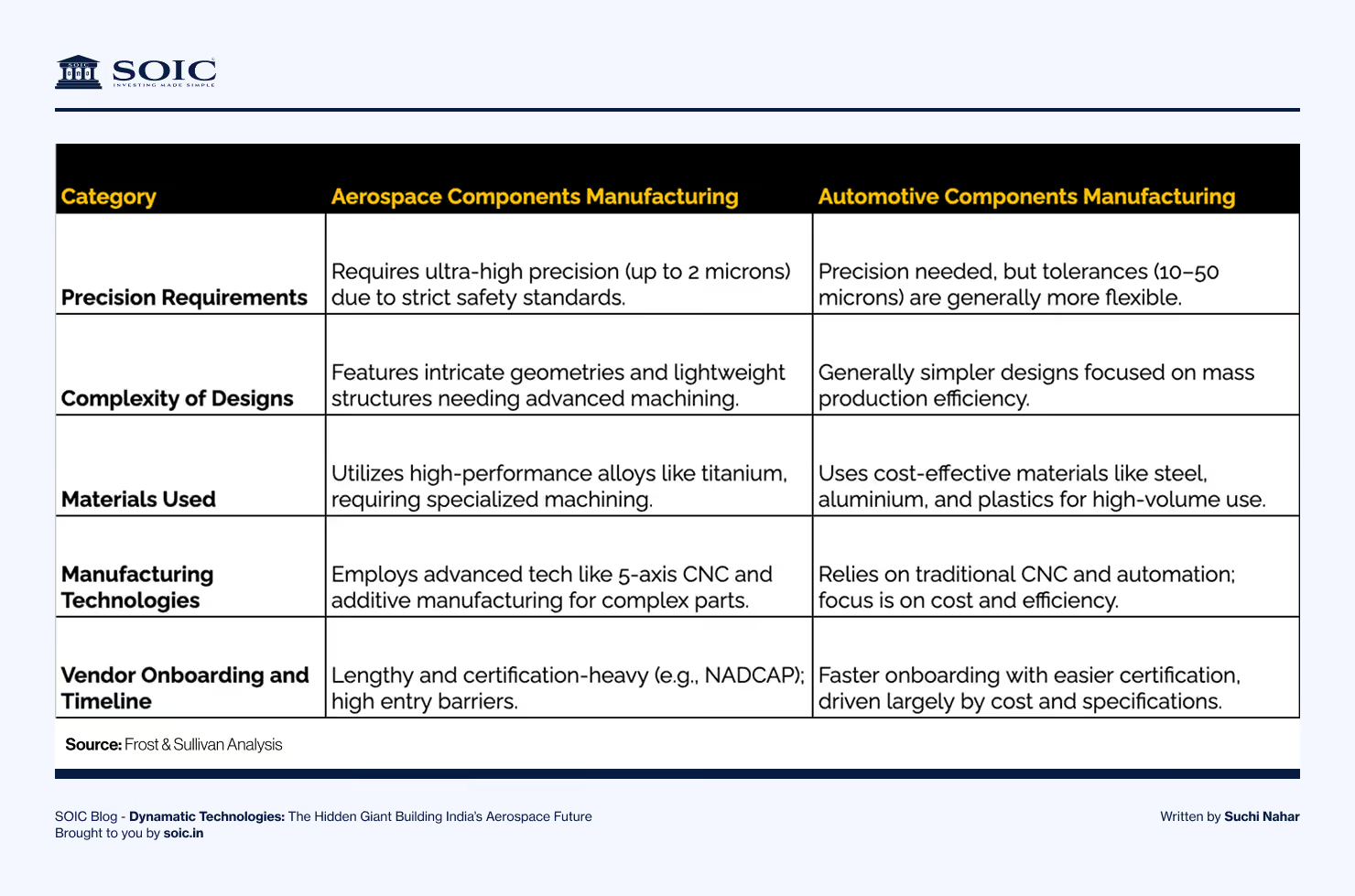

Manufacturing aerospace components is challenging, with a complex supplier network.

Aerospace components are subject to the most stringent defect standards in the industry, with a requirement for zero Parts Per Million (PPM) defects. Achieving this level of quality is non-negotiable and forms the foundation for Tier-1 supplier status in the aerospace sector.

During a Decade of Minimal Progress…

Years of capability development and R&D was quietly laying the groundwork…

Attaining Tier-1 supplier status is not an overnight process; it involves a rigorous, multi-year qualification journey. Original Equipment Manufacturers (OEMs) conduct exhaustive due diligence that spans several critical stages: initial supplier identification, Request for Quotation (RFQ) evaluation, product development, First Article Inspection (FAI), and the Production Part Approval Process (PPAP).

Within an ecosystem that comprises thousands of suppliers, only a select few progress to become true partners, deeply involved throughout the entire cycle of design, development, manufacturing, and maintenance.

The aerospace manufacturing sector rewards firms that demonstrate technological depth, mature processes, and uncompromising precision. Companies must make sustained investments in advanced capabilities, materials engineering, specialised processes, and robust quality systems.

Importantly, these investments are undertaken well in advance of any reflection in revenue or profitability, highlighting the long-term commitment required for success.

It is precisely this long-cycle, capability-driven evolution that defines the DNA of Dynamatic Technologies. The company’s approach is anchored in building advanced competencies and robust processes, positioning it to meet the demanding standards and expectations of global aerospace OEMs.

A small number of key OEM orders can validate their capabilities, paving the way for rapid revenue growth across various programs.

2020: Chosen by Boeing for T-7A Red Hawk fatigue testing.

2021: Won F-15EX Eagle II fuselage contract and orders from Dassault Aviation; partnered with Deutsche Aircraft to make D328eco rear fuselage assemblies in India.

2022: Signed long-term MoU with HAL for LCA Tejas front fuselage production (20+ aircraft/year, scaling up).

2024: Expanded Airbus partnership to include aircraft doors—one of India's largest aerospace export contracts, with deliveries starting 2026.

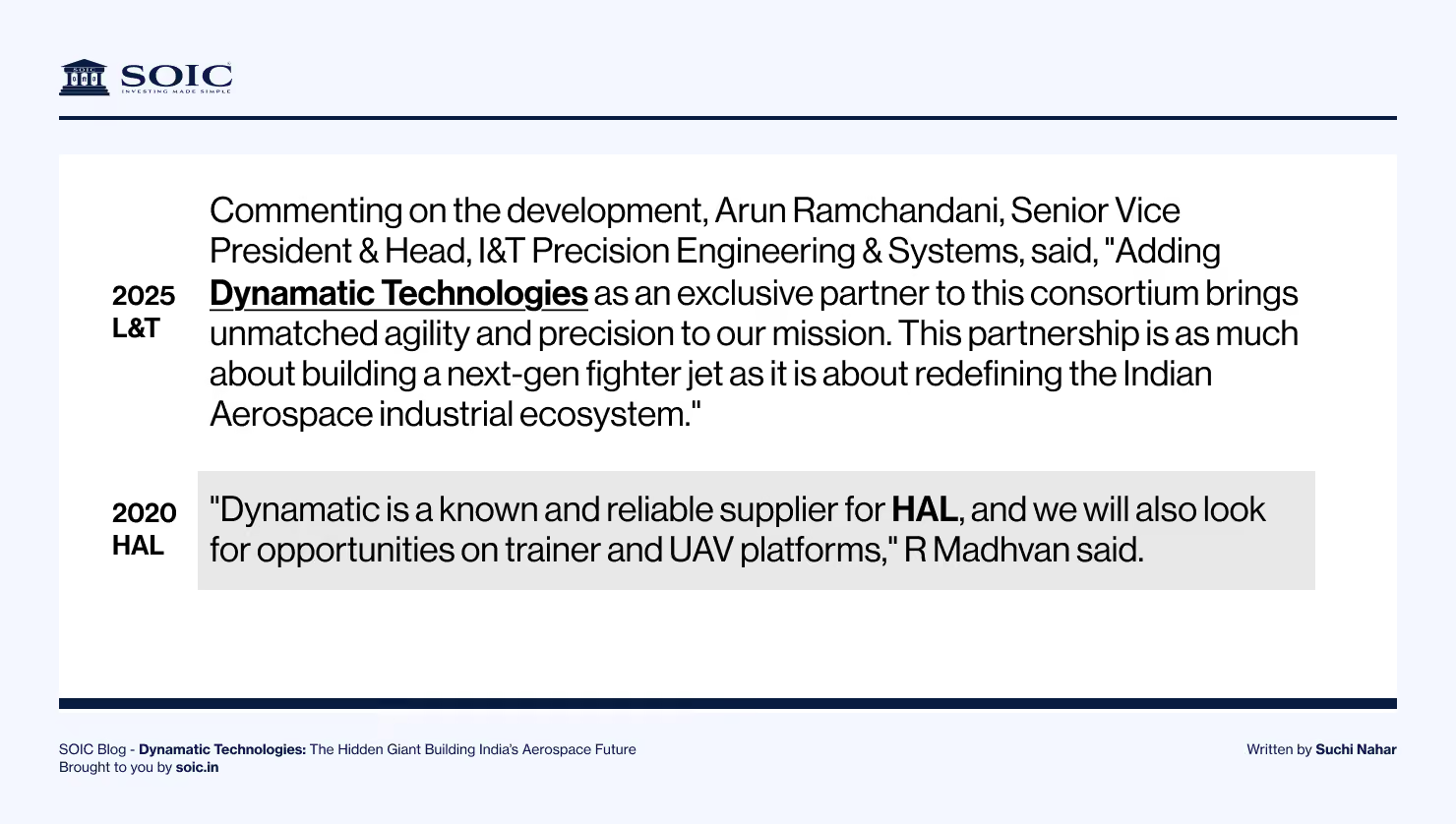

2025: Named exclusive partner by L&T-BEL consortium for AMCA fighter program.

Ongoing discussions of additional OEM parts to drive rapid revenue growth.

Management matters here more than in consumer businesses. The CEO, Dr. Udayant Malhoutra, and the senior team have been associated with the firm’s long capability build and cross-border strategy. The company’s disclosures and AGM materials show hands-on leadership in aerospace industrialisation, ecosystem-building, and strategic German/UK investments.

Two governance points I look for:

Overall, the management appears as builders with a long view — which is precisely what you want in a long-gestation engineering story.

Dynamatics has proven its capability to scale relationships with customers…

Not Just Aerospace — Banking on Multi-Billion-Dollar Horizons for growth

Here, let’s shift into numbers and valuation, and what that implies for investors.

Source: ALPHA IDEAS Presentation 20/20 NOV-2025

% of revenue from Airbus, Boeing & other aerospace OEMs

A precise customer-by-customer revenue split is not disclosed by the company but they provide a clear directional indicator:

Dynamatic currently accounts for “less than 5% of Airbus + Boeing’s India sourcing”

— which together is over USD 2 billion annually.

This implies that a very large share of Dynamatic’s aerospace revenue comes from Airbus & Boeing, because:

So while exact % isn’t disclosed, the data implies: Airbus + Boeing together likely contribute 60–70% of total aerospace revenue - (majority of the ₹607.85 crore A&D FY25 revenue).

This is consistent with their status as Tier-1 suppliers and their multi-decade programs.

Order book pipeline of Airbus & Boeing (tailwind for Dynamatic) -

Boeing India sourcing = USD 1.25 billion per year - and continues to grow due to ramp-up in commercial & defence programs.

Airbus currently sources “over ₹1,000 crore worth of parts from India” — and plans to double this before 2030.

Airbus + Boeing’s India sourcing (~USD 2 billion combined) will double this decade — creating massive visibility for Dynamatic.

Since Dynamatic currently captures “<5% of this,” even moving to 10% share would:

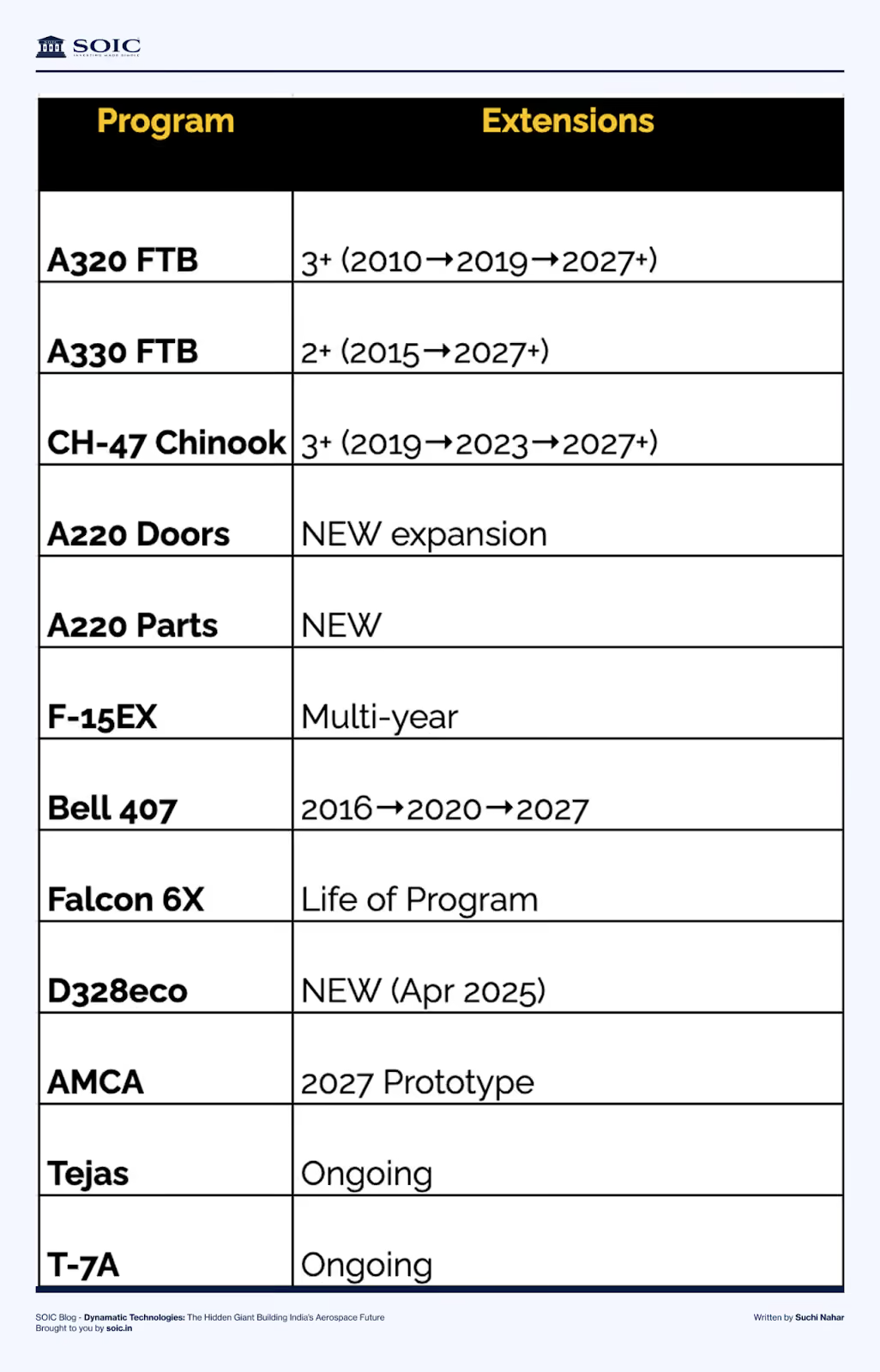

A220 Program Pipeline

Other OEM pipeline tailwinds

Dynamatic’s aerospace revenues are dominated by Airbus and Boeing, which likely contribute 60–70% of the segment though exact splits are not disclosed. The company currently captures less than 5% of the USD 2+ billion India sourcing by Airbus and Boeing — a figure expected to double this decade. Airbus alone plans to double India sourcing by 2030, and Boeing already exports USD 1.25 billion worth of components from India annually. This expanding procurement pipeline, combined with Dynamatic’s A220 doors industrialisation, Dassault programs, and D328eco fuselage assemblies, gives the company multi-year visibility for strong growth.

Compared to the last decade, it is expected Dynamatic to do significantly well over the next decade

Aerospace

With enough land in Bangalore and Coimbatore, new facilities can be established with minimal investment. The company has sufficient staff to double current revenue and is positioning itself as a design-led subsystems supplier focused on assembly.

Hydraulics

Historically a cash cow, this segment should see margin expansion and stable growth after ongoing restructuring.

Metallurgy

Margins are set to improve post-restructuring, with revenue rising as manufacturing increases. Entering explosives could offer major upside, though it's uncertain.

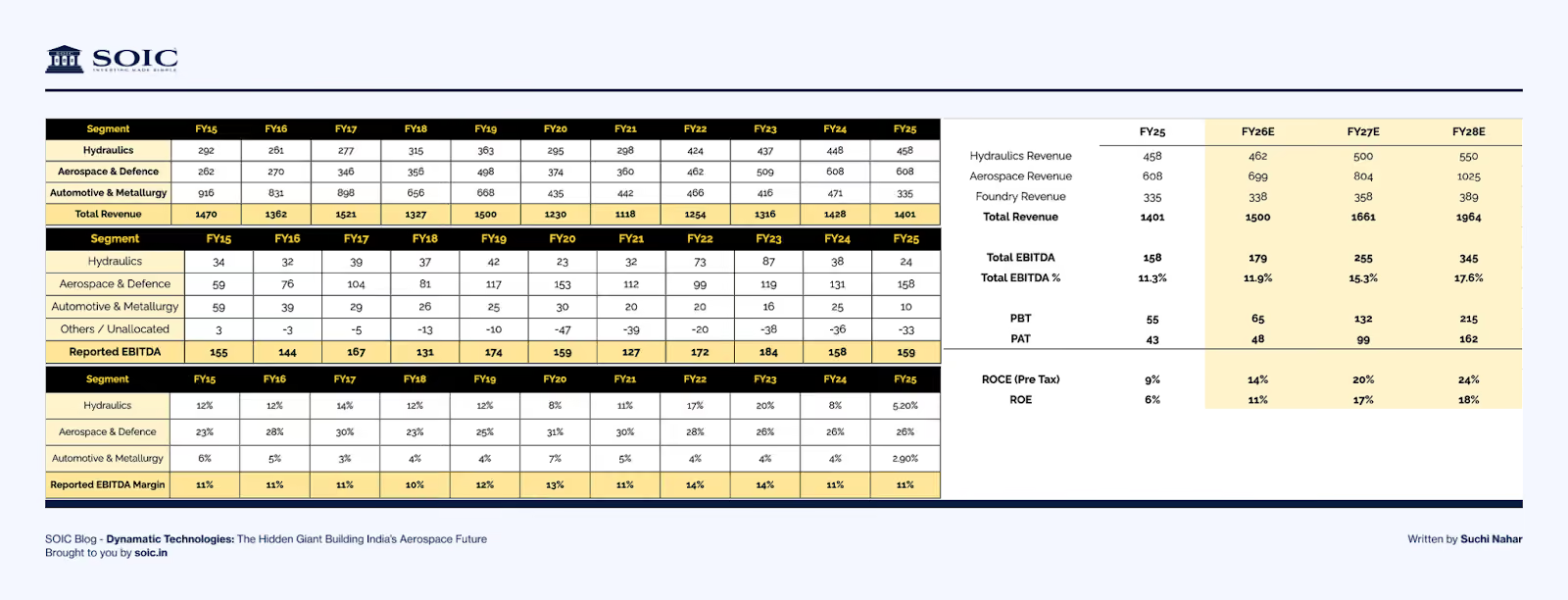

Dynamatic Technologies enters its next decade with one of the strongest multi-engine growth runways in its history. The company is positioned for double-digit revenue growth, supported by a sharp ramp-up in aerospace programs such as Airbus A220 doors, D328eco fuselage assemblies, Boeing F-15 and T-7 structures, as well as deeper penetration into Bell and Dassault platforms. With adequate land bank and manpower already in place, Dynamatic can scale aerospace revenues to 2x of current levels without heavy incremental capex, while operating leverage is expected to lift margins from 11% to 17–18% over FY26–28.

Hydraulics, historically a cash-cow, is undergoing restructuring with annual cost savings of ₹36 crore, unlocking margin expansion and steady growth. The foundry business in Germany, now being repositioned for defence and aerospace, offers long-term optionality—especially as Europe undergoes large-scale militarization. Beyond its core, Dynamatic is positioned to benefit from fast-growing segments like UAVs, anti-drone systems, space hardware, armoured vehicles and missile structures, where multiple products are already prototyped and customers are engaged.

With a strong 24–36 month order pipeline, expanding global sourcing by Airbus/Boeing, and India’s defence indigenization push, the company has visibility for multi-year compounding. If scaled well, Dynamatic has the capability to become a ₹8,000+ crore revenue company, a 7–8x market-cap opportunity over the long term.

In these kinds of companies:

You cannot predict next year’s revenue.

No spreadsheet can model the timing.

Even management doesn’t know the exact quarter the inflection hits.

Because payoff happens when:

You can’t model that on Excel. What you can see is capability and clients accumulation over 15–20 years.

HBL had Kavach waiting for India. Dynamatic has aerospace & defence capability waiting for global scale.

Don’t judge these companies by the last decade’s revenue.

Judge them by the last decade’s customers.

HBL had the Railways. Dynamatic has Airbus, Boeing, Bell, Dassault, HAL, BEL — the best in the world.

That’s the real J-Curve story.

And that’s why Dynamatic today feels like HBL in 2019.

The J bent… and the curve took off. Dynamatic is sitting somewhere on that “bend.” Some closer to the upward leg, some just starting the grind. But they all share one thing: deep precision capability.

The information provided is for educational purposes only and should not be considered investment advice. We are SEBI-registered research analysts. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

.avif)

0 Comments