From Heatwaves to Market Waves: Decoding India’s AC Industry

BY

Shuchi Nahar

Consumer Goods

Consumer Trends

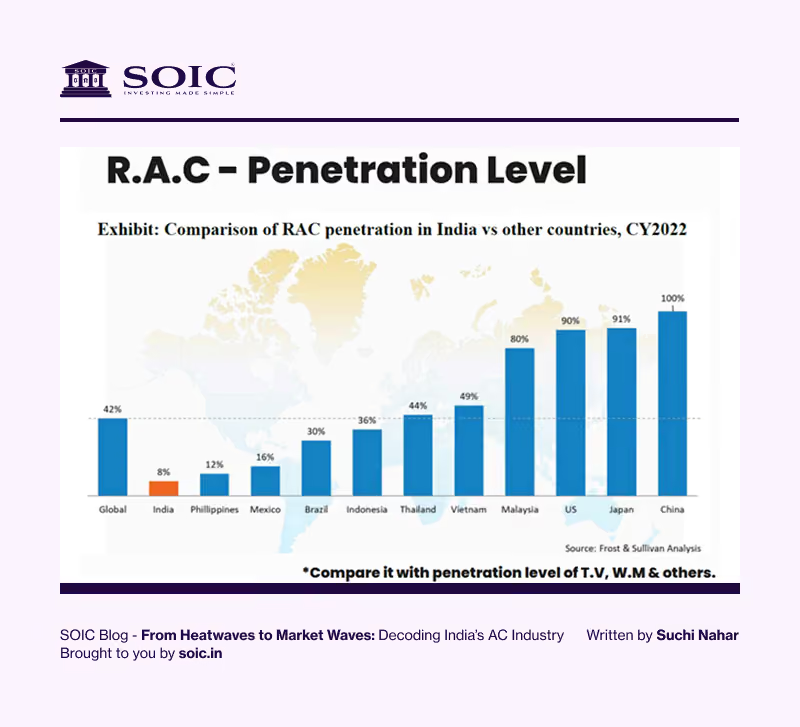

Imagine this: it’s peak summer in Delhi, the kind that melts tar on the roads, and yet only 8% of Indian households own an air conditioner. Compare this with China (~100% penetration), the US (~90%), or even smaller economies like Vietnam (~44%). India’s AC story is not even at the starting line—and that’s what makes this sector one of the most exciting long-term growth stories in consumer durables.

Let’s break down the air conditioner value chain, industry dynamics, and the companies riding this wave.

Industry Dynamics – A Sector Waiting to Explode

Current penetration: Just 8% in India (vs 60–100% in developed markets).

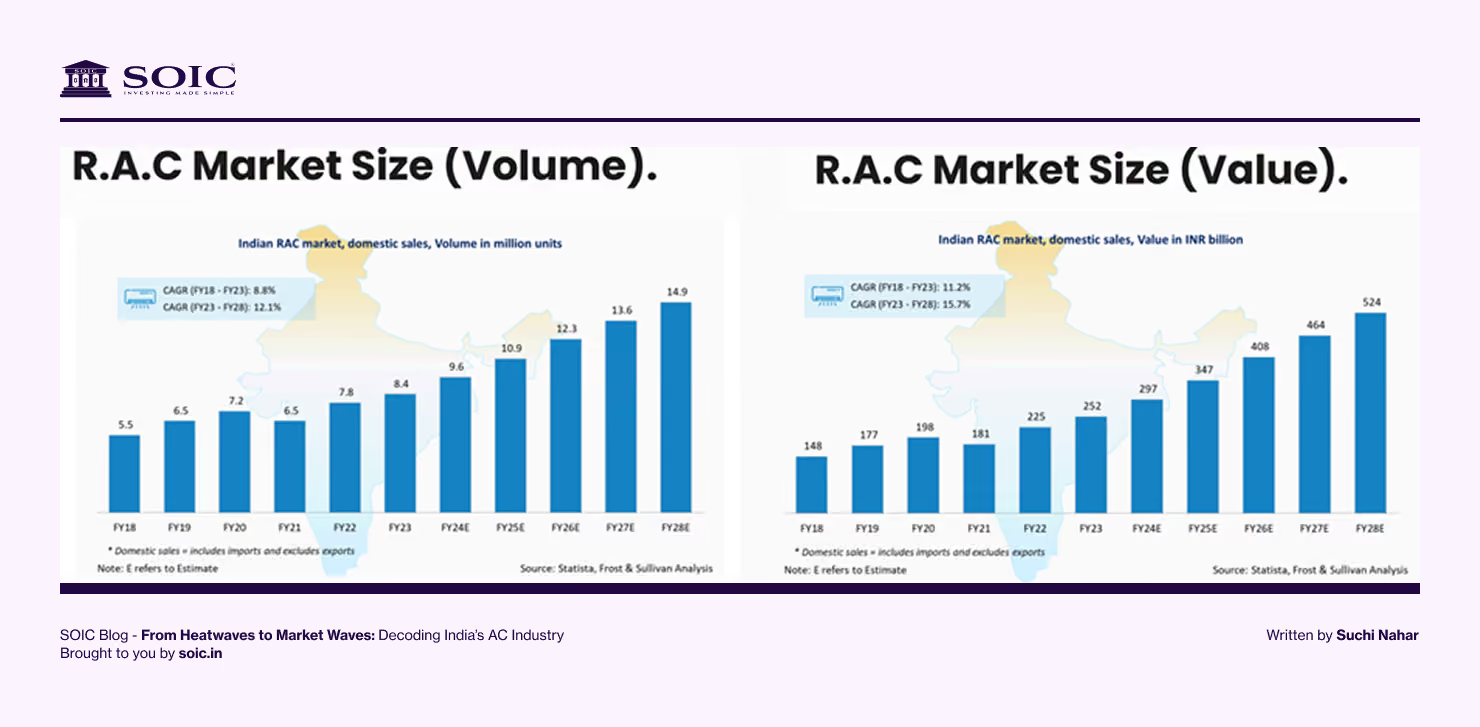

Market growth: Indian RAC (Room Air Conditioner) volumes grew at a 10% CAGR (FY13–19), and post-COVID, the momentum picked up with a projected 17% CAGR from FY23–28 (see Exhibit 7 in your chart).

Global vs India gap: Global AC volumes ~150 mn units, China ~85 mn, India just ~7–8 mn (Exhibit 10). The runway is massive.

With rising middle-class income, urban heat islands, and easy EMIs, AC adoption is poised to be the next refrigerator/TV story of the 2000s.

Penetration vs Other Durables – Why AC is the Last Frontier

The highlights something fascinating:

TVs – 65% penetration

Refrigerators – 29%

Washing Machines – 12%

ACs – only 8%

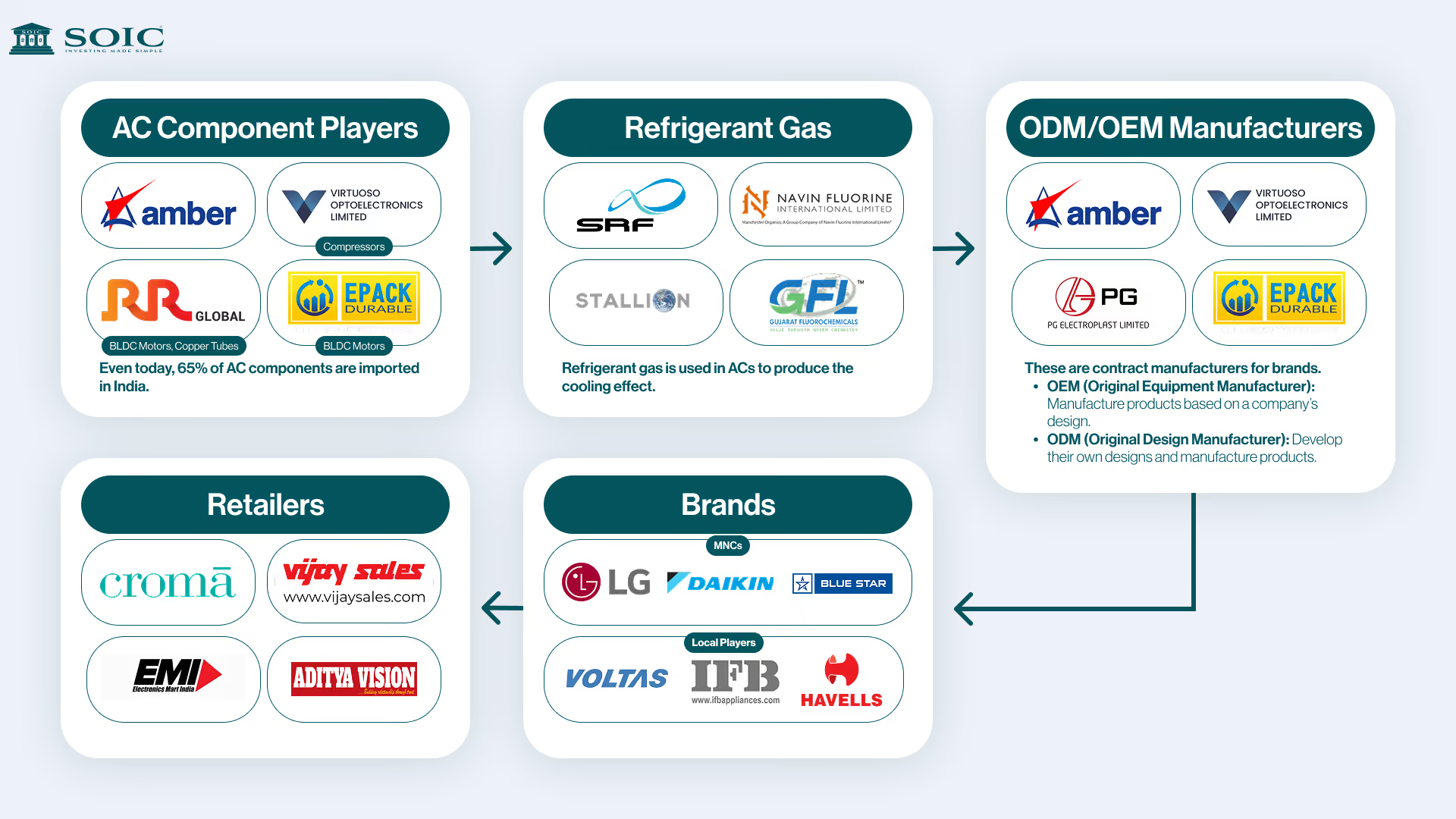

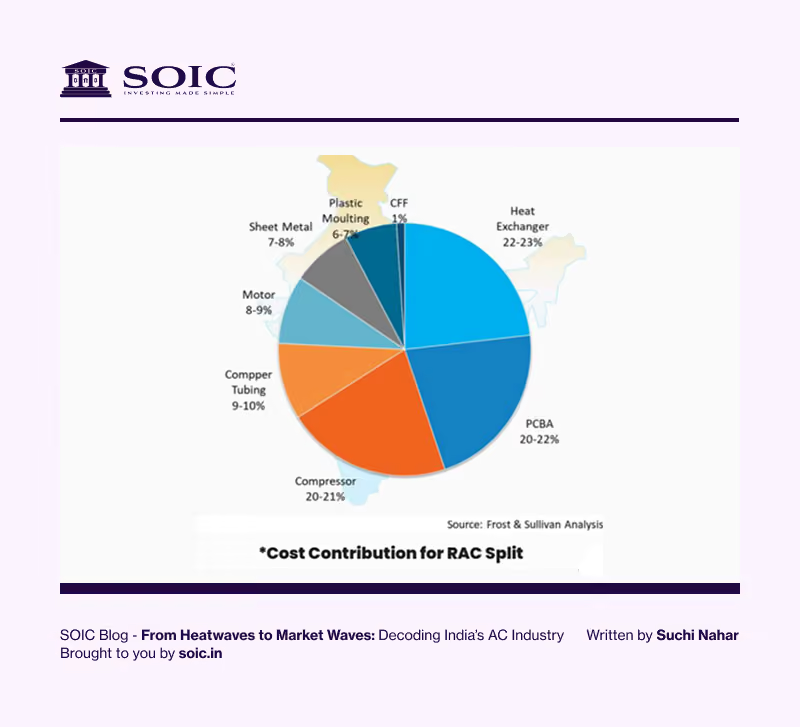

The Value Chain –RAC Manufacturing decoded for you!

An AC isn’t a single product—it’s a collection of multiple precision-engineered parts. Here’s the value chain:

Stamping & Sheet Metal – frames, outdoor unit shells.

Injection Moulding – plastic covers.

Copper Tubes Bending & Forming – core for heat transfer.

Heat Exchangers – efficiency drivers.

Powder coating

Compressors – the heart of the AC, still heavily imported (Japan, Thailand).

Induction Motors & Fans – for circulation.

Cross Flow Fan Manufacturing

PCBs & Controls – the “brains” of modern inverter ACs.

Final Assembly & QC

Packaging and Shipping

Companies like Amber Enterprises, PG Electroplast, Virtuoso Optoelectronics, and Epack Durable act as ODM/OEM partners—building ACs for brands.

The Players – Who’s Who in the AC Universe

Consumer-Facing Brands (Frontline Players)

Voltas (Tata): Market leader (~19% share). Sold 2M+ units in FY24. Strong in Tier-2/3 with affordable EMIs. But highly weather dependent.

Daikin: The Japanese powerhouse. Scaling to 2M units in FY25, 5M by 2030. Localizing compressors & PCBs. Premium brand, strong in both RAC + commercials.

LG & Samsung: Global MNCs with tech edge. LG leads inverter ACs; Samsung is trying a comeback with AI/WindFree models. Strong branding, weaker Tier-3 presence.

Blue Star: Balanced player — RAC + commercial projects. Trusted in institutional cooling (airports, malls, IT parks). RAC growth but not dominant.

Havells (Lloyd): The aggressive challenger. Focused on affordability, distribution via Havells’ vast dealer network, and Tier-2/3 penetration. Rapidly climbing share (~6–7%).

IFB Industries: The quiet riser. Known for washing machines, now betting big on RAC. FY25 RAC revenue grew 59% YoY; volumes crossed 4 lakh units. Strong in North India (8–9% share in states), but still small nationally. Turning EBITDA-positive in ACs, investing ₹350cr capex, expanding retail outlets. A “wait-and-watch” story.

Back-End Specialists (Proxy Players)

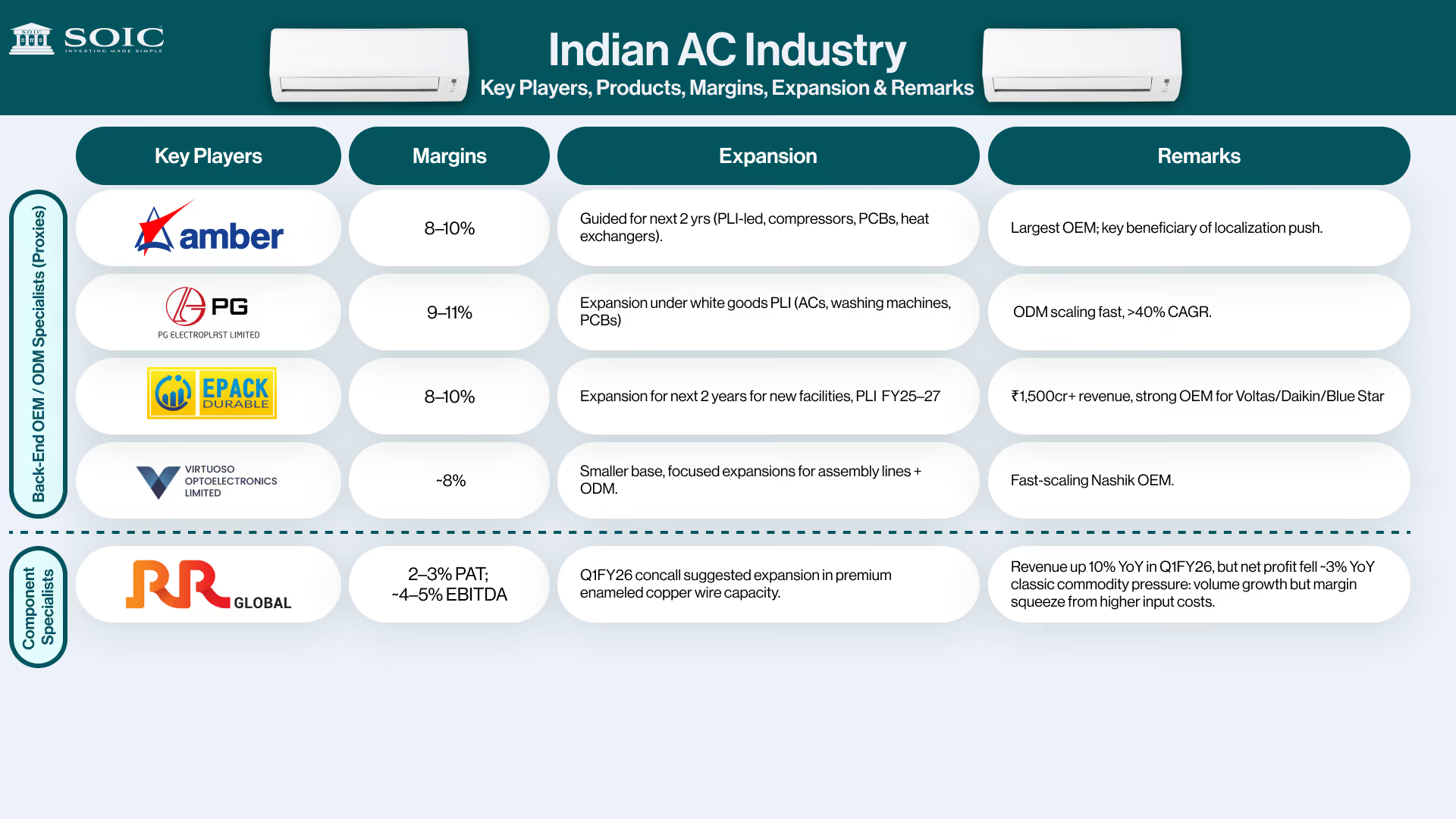

Amber Enterprises: The OEM giant. Supplies most major brands, from copper tubes to full RACs. Heavy capex in backward integration (laminates, heat exchangers). Scale advantage, but valuations are sky-high.

PG Electroplast (PGEL): From plastics to full ODM player. The Supa plant under PLI integrates heat exchangers, copper tubing, and RAC assembly. Fast growth, but working capital heavy.

Epack Durable: Rapid scaler. Revenue ₹1,500 cr. in FY24, growing at 30%+. Supplies to Voltas, Blue Star, Daikin, with a strong backward integration, but customer concentration is a risk.

Virtuoso Optoelectronics: Smaller, nimble OEM, that specialises in indoor/outdoor RAC assembly and expanding into components. Q1FY25 revenue up 27%. Fast but dependent on tie-ups.

Why this matters: Often, OEMs (proxy players) earn steadier margins than brands, as they sit on the “picks & shovels” side of the value chain.

This means companies don’t just ride the RAC boom but also benefit from refrigeration, commercial AC demand (malls, offices), and spare parts—making the story more diversified.

Voltas (Tata Group)

Clear market leader with ~19.5% share of the RAC market.

The year 2024-25 was historic: sold over 2.5 million AC units, the highest ever by a single brand in India.

Strong distribution across metros and Tier-2/3 towns, backed by Tata trust.

The new Tamil Nadu facility will boost domestic production capacity.

Plays well on financing options and promotions, making ACs affordable to middle-class consumers.

Weakness: extremely weather dependent. A bad summer or extended monsoon quickly dents sales.

Reputation for reliability in projects (airports, malls, IT parks).

Growing fast in RAC but battles intense competition in price-sensitive categories.

Strength: balanced play across residential + commercial cooling.

Weakness: lacks mass-market dominance in RAC, compared to Voltas or LG.

How demand shapes in consumer durables – Explained in detail!

Havells (Lloyd brand)

Havells bought Lloyd in 2017 and has been scaling it up aggressively.

Strategy: use Havells’ powerful distribution network and Lloyd’s brand recognition to crack RAC.

Strong in Tier-2/3 towns where affordability matters.

Weakness: still building brand equity compared to Voltas, LG, or Daikin; consumer perception of Lloyd as a “value-for-money” brand limits premium positioning.

IFB Industries (The Quiet Riser)

Known for premium washing machines, IFB is finally making noise in ACs.

In FY25, RAC sales jumped 59% YoY, with volumes crossing 4 lakh units. In northern states, IFB even commands a good hold.

Importantly, its AC division turned EBITDA-positive, and the company is investing ₹350 crore into expanding capacity.

Still, IFB’s national share is tiny (<1%), and its distribution/service network lags peers. But the momentum suggests it’s no longer invisible.

Daikin (Japan’s premium warrior)

One of the fastest-growing MNC players in India; aiming for 2 million unit sales (20 lakh) in FY25 and 5 million by 2030.

It already has multiple plants (Neemrana, Sri City) and is localising aggressively—compressors, PCB circuits, and parts.

Strength lies in its global tech (inverter ACs, eco-friendly refrigerants, smart systems) and strong commercial HVAC segment.

Weakness: premium pricing limits deep penetration into value-conscious buyers, especially in smaller towns.

Strategic push: increasing localisation from 53% to 75% to cut costs and reduce import dependence.

LG (The efficiency king)

Known for dual inverter and energy-efficient tech, with strong branding in urban markets.

Crossed 1 million AC sales within just 100 days in 2024, showcasing consumer pull.

Targets mid-premium and premium segments; strength lies in quality and after-sales.

Weakness: weaker penetration into the mass-value segment compared to Voltas or Lloyd.

Samsung (The comeback story)

Has relaunched its AC lineup aggressively with “WindFree” and AI-enabled models.

Targeting ~10% market share in RAC by differentiating on design and smart features.

Historically, Samsung struggled to scale ACs like LG or Voltas but is trying to position itself as an aspirational, tech-driven choice.

From Humble Parts to Integral Player

Amber Enterprises: The Backbone OEM / ODM Giant

Amber did not start by selling shiny ACs with flashing lights. It began with parts. Over the years, it built up backward integration—sheet metal components, plastic injection molding, heat exchangers, motors, copper tubing, etc.

Today, it’s among the few Indian companies that:

Make components + full AC units (both room ACs (RAC) and commercial ACs)

Operate multiple plants across states, providing better proximity to brand customers and reducing lead times.

The largest contract manufacturer in RAC with deep backward integration (plastic parts, copper tubing, motors, fans, heat exchangers).

Supplies almost every major AC brand in India—truly the “arms dealer” of the industry.

Capex heavy: recently investing in copper laminate plants to secure electronic components.

Weakness: small size compared to giants like Amber; dependent on tie-ups with big brands; margin pressure in highly competitive OEM business.

3. Ancillaries & Component Makers: The Unsung Heroes

While Amber & PGEL are big names, much of the AC boom depends on smaller component or ancillary players: makers of compressors, PCB laminates, copper tubing, fans, motors, heat exchangers etc.

New Players in the Value Chain - Specialised Cooling Players

KRN Heat Exchangers

KRN is a component / heat exchanger supplier stage. Its margins are healthy (~15–17%) for component players, which is a strong sign of pricing power or efficiency. Its facility and PLI backing suggest it wants to deepen backward integration and supply more to OEMs/brands.

Strategic moves: • They have commissioned a new manufacturing facility at Neemrana (via a wholly owned subsidiary, KRN HVAC Products Pvt Ltd) starting May 31, 2025. This should expand capacity for heat exchangers / HVAC products. • Their subsidiary was sanctioned ₹141.72 crores under the PLI scheme (white goods) to support localization, integration, and capex. • Exports are doing well: The export segment grew ~39.04% YoY, and they see a push to raise export share (~50% over 3 years).

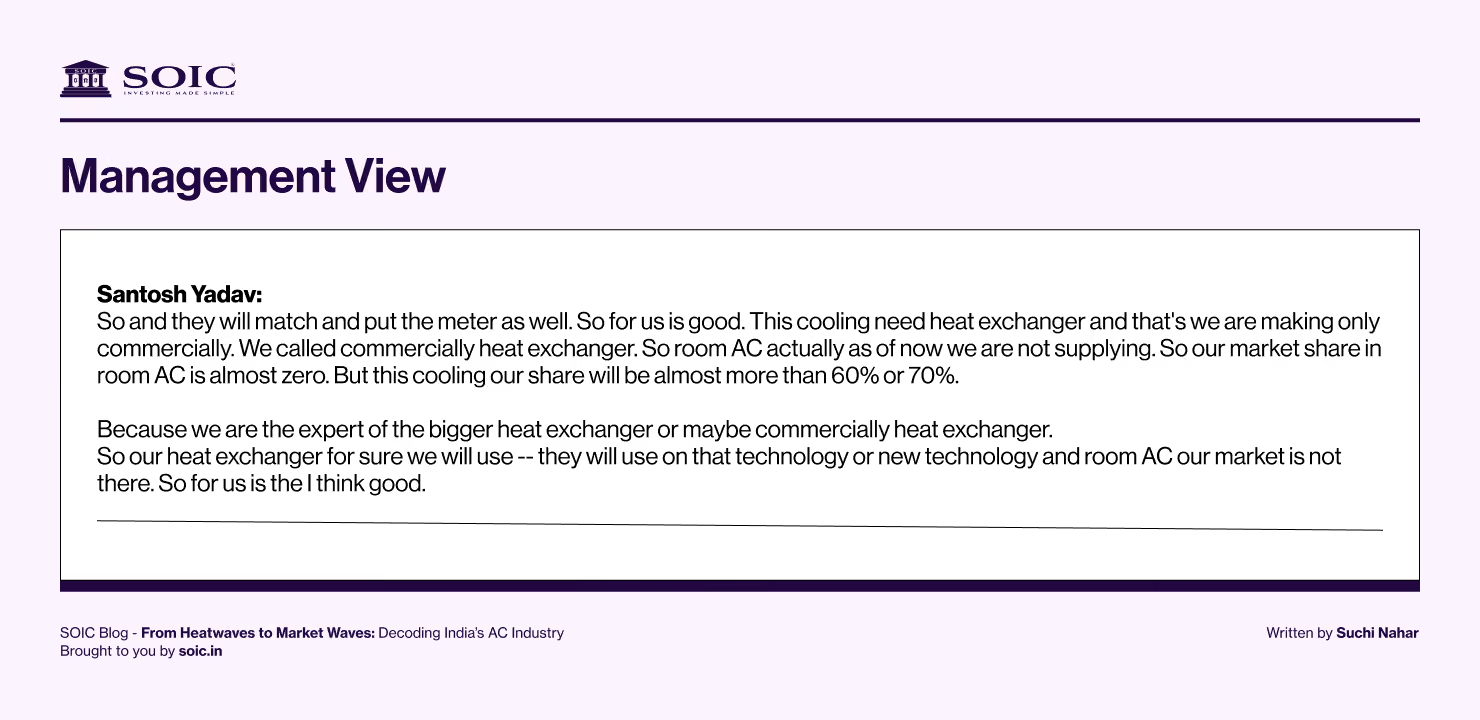

Management View:

Ram Ratna Wires

Financial snapshot: • Revenue: ₹986.14 crores (↑22.3% QoQ, ↑10.2% YoY) • Total expenses also rose ~23.1% QoQ / ~10.5% YoY. • Net profit: fell ~17.8% QoQ & ~2.9% YoY to ₹15.93 crores. EPS ₹3.30.

Interpretation / value-chain relevance: Ram Ratna is primarily a wires and cables/component manufacturer. In the AC chain, they supply copper wiring, electrical cables, possibly connecting to motors/PCB components. Their falling profit despite revenue growth suggests margins are under pressure—higher operating / input costs may be eroding returns. Growth in revenue but shrinking margins is typical under seasonal/commodity stress, and it warns that even component players are not immune to macro swings.

Shree Refrigerations Ltd

Business scope: Shree Refrigerations builds chillers, industrial / HVAC cooling systems, marine & defence cooling. They are becoming relevant in special cooling / industrial / high-end segments, not just mass ACs.

Recent strategic move: They have tied up with Canadian firm Smardt Chillers to bring oil-free chiller cooling solutions for data centers in India. This is significant — data centres are high-growth, high-demand, high-margin cooling use cases.

Implication in value chain: Shree sits between component / system / cooling solutions levels. They may be a pick for more niche, premium cooling systems rather than mass RACs. Their push into data centre cooling is a move to expand beyond seasonal residential demand.

Risks/points to watch: Ramp-up risk: the new facility will take time to stabilise. In Q1, they expect initial utilisation to be low. Maintaining margins as input costs fluctuate.

Market Share of Different Players as of FY25

How to Play the AC Cycles: An Investor’s Playbook

1. The Nature of AC Cycles

AC demand in India is extremely seasonal — with 40–50% of yearly sales packed into April–June.

This creates boom-or-bust quarters: a scorching summer sends volumes soaring, while unseasonal rains or cooler weather can crush sales.

Because of this, short-term earnings are volatile, and stock prices of AC brands (Voltas, Blue Star, Lloyd, IFB) and proxy players (Amber, PGEL, Epack) swing sharply with the season.

2. Poor Summers = Great Entry Points

When summers turn weak and monsoons arrive early, AC companies report sluggish Q1 numbers.

Stocks often “bomb out” 20–30% as analysts cut earnings estimates.

But remember: the long-term thesis is intact — penetration is still <10%, climate change is worsening heatwaves, and the middle-class appetite for ACs is only rising.

These weak summers are often the best entry points because:

Inventory overhang and discounts are temporary.

Consumer demand revives with the next heatwave.

Structural drivers (penetration, PLI, local manufacturing) don’t change.

3. Strong Summers = Exit or Trim Points

When summers are extremely hot, companies report bumper Q1s.

Stock prices usually run ahead of fundamentals, pricing in a multi-year boom.

For investors, this is often a time to book partial profits or trim positions — because seasonality euphoria rarely sustains.

4. Where to Position in the Cycle

Consumer-facing brands (Voltas, Daikin, Blue Star, Lloyd, IFB)

Highly sensitive to seasonality → they sell the final product.

Weak summers hurt them most; hot summers reward them most.

Best bought during weak quarters when the market panics.

OEM/Proxy players (Amber, PGEL, Epack, Virtuoso)

Slightly less exposed to seasonality in sales, but order cuts and under-utilisation hit margins.

They recover faster as their order books are linked to multiple brands.

Still, the best entries are often after weak Q1s when order flow looks uncertain.

5. Investor Thesis (Simple Rules)

When it rains, you buy → Poor summers + good monsoon = bad quarterly results = better entry prices.

When it burns, you earn → Hot summers = bumper quarters = ride the rally but don’t chase late.

Focus long-term → India’s AC penetration <10% ensures a structural multi-decade growth story. Short-term weather shocks create opportunity.

Diversify within the value chain → Hold both brands (demand capture) and OEMs (supply enablers) to smooth volatility.

Bottomline: The AC sector is like India’s weather — unpredictable in the short term, but steadily warming in the long run. The best strategy is contrarian: buy when weak summers spook the market, trim when heatwaves fuel euphoria, and hold for the long structural cooling revolution.

Key Metrics to Track in the AC Sector:

1. Volume Growth (Units Sold)

Think of this as the heartbeat of the industry. Unlike TVs or fridges (where replacement demand is high), ACs in India are still in the first-purchase stage.

Watch monthly/quarterly volume trends reported by companies (Voltas, Daikin, Blue Star) and OEMs (Amber, PGEL).

Sharp spikes during heatwaves show how weather swings can supercharge demand.

Proxy: Monitor import/export data, monthly AC shipment data from CEAMA (Consumer Electronics and Appliances Manufacturers Association).

Why it matters: Higher volumes dilute fixed costs for both brands and OEMs, lifting margins.

2. Capex Plans (Capacity Expansion)

ACs are capex-heavy to make — you need stamping presses, copper tube bending, heat exchanger lines, and testing labs.

Every proxy player (Amber, PGEL, Epack, Virtuoso) is announcing new plants under the PLI scheme.

Brands like Voltas and Daikin are also setting up greenfield plants in Tamil Nadu, Sri City, and Neemrana.

Why it matters: Big capex today = higher earnings visibility tomorrow, if demand holds up. But it also creates risk if demand falters (under-utilized factories burn cash).

3. EBITDA Margins

For consumer-facing brands (Voltas, LG, Daikin): margins are squeezed by price wars, marketing spend, and after-sales costs (typical range: 7–10%).

For proxy players (Amber, PGEL, Epack): margins depend on utilisation, raw material costs, and integration (typical range: 8–12%).

For ancillaries (component specialists): niche players can earn higher margins if they control critical parts (e.g., compressors, PCBs).

Why it matters: Margins tell you who has pricing power — brands that charge premium (Daikin, LG) or OEMs with scale (Amber).

4. Market Share Percentage

Voltas currently holds a market share of approximately 19.5%, maintaining its position as the leading brand in the Room Air Conditioners (RAC) segment. This represents a decline from its historical share of 25-26%, as the industry now features over 65 competitors, including some multinational corporations that are particularly aggressive in their strategies.

OEMs don’t disclose “share” in the same way, but their client roster shows who they ride with.

Just for example, Daikin from nowhere has come in and grabbed 18% of Market share in the industry.

This is how competition hurts. Just check the contraction in margins which is happening over the years

Why it matters: Rising market share = stronger bargaining power with distributors (for brands) or with clients (for OEMs). Falling share = risk of getting squeezed out.

OEM/ODM players: often priced at premium valuations because they represent a “picks-and-shovels” play with faster growth visibility (Amber trades ~80–100x, PGEL and Epack are also high).

Market rerates quickly if demand slows or capex returns lag.

Why it matters: Even the best story can disappoint if you overpay. This sector is currently priced for perfection in many names.

6. Summers (Heatwaves or Rains)

The AC industry’s biggest “wild card.”

A hot summer = bumper quarter for everyone.

Unseasonal rains or a weak summer = inventory pile-up, discounting, and margin compression.

Climate change ironically works as a tailwind (heatwaves becoming frequent, urban heat islands worsening).

Why it matters: One season can swing a company’s yearly earnings, especially for consumer-facing brands.

7. Penetration Level (Households Owning ACs)

India’s current penetration ~8% vs >100% in China and >90% in developed markets.

Even doubling penetration to 15–20% by 2030 means tens of millions of new units sold.

Rising middle-class, better electricity reliability, and financing options (EMI, BNPL) are the big enablers.

Why it matters: This is the long-term thesis. India’s AC story isn’t about replacement demand (yet) — it’s about first-time buyers. That makes it a structural growth industry, not just a cyclical one.

How to Use These Metrics as an Investor

Short-term tracker → Volumes, summers, and margins (quarterly updates).

Long-term lens → Penetration level and valuation (PE re-rating/de-rating).

Recent & Emerging Trends / Shifts

Here are trends that are shifting the value chain or creating new “twists in the plot”:

Compressor manufacturer push: Companies like Daikin (in JV with Rechi, Taiwan) are planning compressor manufacturing in India, to supply several brands, not just their own units. This is important because compressors have been a choke point: high import cost, tech/quality barriers.

PLI Rounds expanding component coverage: New rounds under the PLI scheme are selecting more companies for AC component manufacturing. For example, the third round of AC & LED component window saw ~₹3,516 crore investment committed; 10 AC component manufacturers added etc.

Rise of manufacturing hubs: The Sri City SEZ is a concrete example where brands + suppliers are located near each other. Such geographic clustering (accompanying favorable state policies, land/infrastructure incentives) reduces logistic cost, improves component supply lead times, and helps labor availability.

Electronics / PCB / Inverter / Smart AC push: Many AC units globally & in India are moving towards inverter technology (variable speed compressors/motors), IoT controls, smart scheduling. This increases the importance of semiconductors, PCBs, and firmware. India is still importing many of these, so companies & policy are pushing local PCB, driver circuits etc. Panasonic India head recently emphasized the need for a separate PLI for the AC segment to boost PCB manufacturing.

Efficiency & Environmental Regulations: As energy becomes costlier, consumers increasingly care about efficiency. Also refrigerant regulations (global move towards lower global warming potential (GWP) gases), noise norms, safety norms. This forces R&D and can shift component design (compressors / condensers / coils etc.).

Cost pressures & seasonal volatility: Raw material inflation, logistics cost, and seasonality (peak sales in summer vs off-season) can lead to underutilisation of capacity. So companies with flexible output, diversified products (e.g. commercial AC, refrigeration, cooling products) can hedge.

Risks, Uncertainties & Competitive Threats

While things look promising, there are risk zones to watch. A story is only as good as its obstacles.

Technology & Patent risk: Some tech (especially in compressors, high-efficiency motors, inverter systems) is patented/controlled globally. Indian firms need to license or develop equivalent tech. Without that, they may lag in performance.

Cost of raw material and foreign components: Even with PLI, many key inputs come from abroad; exchange rate swings, trade policy / import duties, shipping disruptions matter.

Scale & Utilization: Factories need to run at high capacity for attractive margins. If demand slows / seasonality is harsh, factories idle → fixed cost drag.

Highly seasonal: 40–50% of AC sales happen in just Apr–Jun.

Cool/rainy summers = bust → unsold inventory, heavy discounts, weak profits. One weak summer can derail a year’s earnings, but the long-term trend stays strong thanks to rising heatwaves and low penetration.

Regulatory / Standards Changes: If energy or environmental regulations become stricter, companies must adapt or face non-compliance. That requires investment in R&D, testing labs, and sometimes the risk of older inventory becoming obsolete.

Competition from low-cost import players: Countries like China / some Southeast Asia have mature AC supply chains, lower cost of capital / labor. If India delays efficiency / cost reduction, brands may find cheaper sources elsewhere or import more.

Consumer behavior & electricity cost constraints: Even with ownership, usage cost (electricity bills), maintenance, reliability, power outages affect satisfaction. In many non-metro / rural areas, unreliable grid or high tariffs reduce usage.

What the Ideal Chain of the Future Looks Like

Compressor factories in multiple states, possibly in JV with foreign tech firms, producing 2-3 million units/year locally, not just for captive consumption but supplying other brands.

Heat exchangers, fan motors, blowers, coils, PCB & inverter driver circuits manufactured locally, with design and R&D departments improving efficiency; some local firms filing patents.

Advanced components like smart sensors, IoT modules, and controls being integrated, perhaps some made domestically; software / firmware design becomes important.

Very high domestic value addition (~75-80%), meaning less dependency on imports, and lower landed cost for brands.

Distribution and after-sales networks strengthened, particularly in Tier-2/3, with better installers, warranty & spare parts infrastructure, and focus on total cost of ownership and energy usage.

Environmental standards are enforced, refrigerants shift toward low GWP, and better recycling/disposal. ACs are marketed not just for “cooling” but for efficiency, noise, and climate friendliness.

Manufacturing clusters (like Sri City) functioning as ecosystems: component makers, logistics, power, and infrastructure in place; R&D / testing labs nearby; skilled labor available.

Financing/incentives/government policies continuing to support localisation, perhaps more aggressive import duties or quality standards that favor domestically produced high-efficiency units.

That is the heart of India’s AC story. A country where 90% of homes are still waiting for their first AC is about to see one of the biggest consumer revolutions of our time. And behind every unit that cools a small shop in Lucknow or a new apartment in Kochi lies a fascinating ecosystem — copper tube suppliers, PCB makers, OEM assemblers, frontline brands, and service networks all working in sync.

Voltas and Daikin will keep leading the charge with scale and technology.

LG, Samsung, and Blue Star will defend their turf with global tech and trust.

Lloyd (Havells) is sprinting ahead as the mass-market challenger.

IFB, the quiet riser, may yet surprise us if it turns regional strength into national presence.

Amber, PGEL, Epack, and Virtuoso will keep quietly minting fortunes as the “picks and shovels” providers to all these brands.

Just as Delhi’s unbearable summers made ACs a necessity, rising incomes, better financing, and frequent heatwaves will make them unavoidable across India. The sector’s value chain is not just about machines — it’s about the story of an aspirational India, moving from ceiling fans to split inverters, from “someday” to “today.”

And for investors, the question is not whether India will cool down, but who in this value chain will capture the biggest slice of this cooling revolution. The sweet spot could be proxy manufacturing players + ancillaries, where competitive intensity is lower, and operating leverage can be huge.

Comment down your thoughts below and till then stay cool! Happy Learning :)

Disclaimer:

The information provided is for educational purposes only and should not be considered investment advice. As an educational organisation, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

Consumer Goods

Consumer Trends

Industry Trends

Investing Insights

Market Trends

Sector Analysis

Author

Shuchi Nahar

Masters in Finance with 5 years of industry experience. My approach is to take one sector at a time and explore plausible Investment ideas.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

png.avif)

.avif)

.avif)

.avif)

.avif)

0 Comments