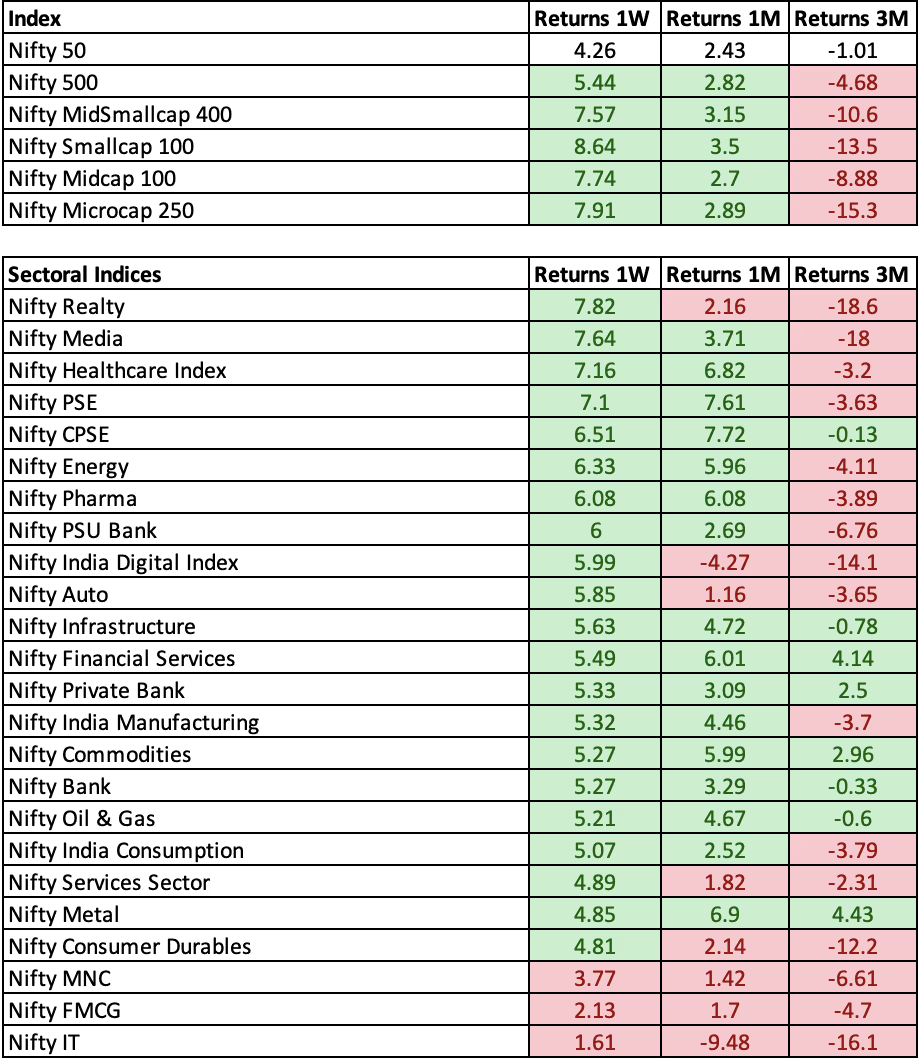

The market rebounded strongly last week after months of bearishness. Here are key insights from indices that outperformed over the past week and the last three months.

MidSmall cap Surge, but Mixed Longer-Term: Nifty Micro-cap 250 led the pack over 1W with a strong +7.91%, yet it remains one of the weaker performers over 3M at -3.88%. This highlights a short-term bounce despite lingering weakness in the broader micro-cap space. Also, mid-cap and small-cap index did well both moving up in the current week close to 7-8%.

PSU Banks & Realty Shine Short-Term: Nifty PSU Bank’s +8.25% and Nifty Realty’s +7.82% in 1W outperformed the benchmark by a notable margin, signalling renewed interest in these segments—possibly driven by improved sentiment or policy cues.

Healthcare & Pharma Buck 3M Downtrend: While many indices stayed in the red over 3M, Healthcare (+2.48%) and Pharma (+2.27%) stood out as defensive plays, maintaining positive returns when most others dipped.

IT & Digital Under Pressure: Nifty IT and Nifty India Digital Index both lagged over 3M, reflecting global tech sector uncertainties and cautious investor appetite in the face of macro headwind. With all the earning disappointments and the boring earning prospects for the future led to the underperformance for the sector.

Private Banks, Financial services, Metals: This sector seems to be the underdog slowly but largely outperforming the market in all the timeframes. Can be an interesting space to keep a watch on.

In the past 3 months Realty, Media, IT, Consumer durables were one of the few names that corrected the most amongst others

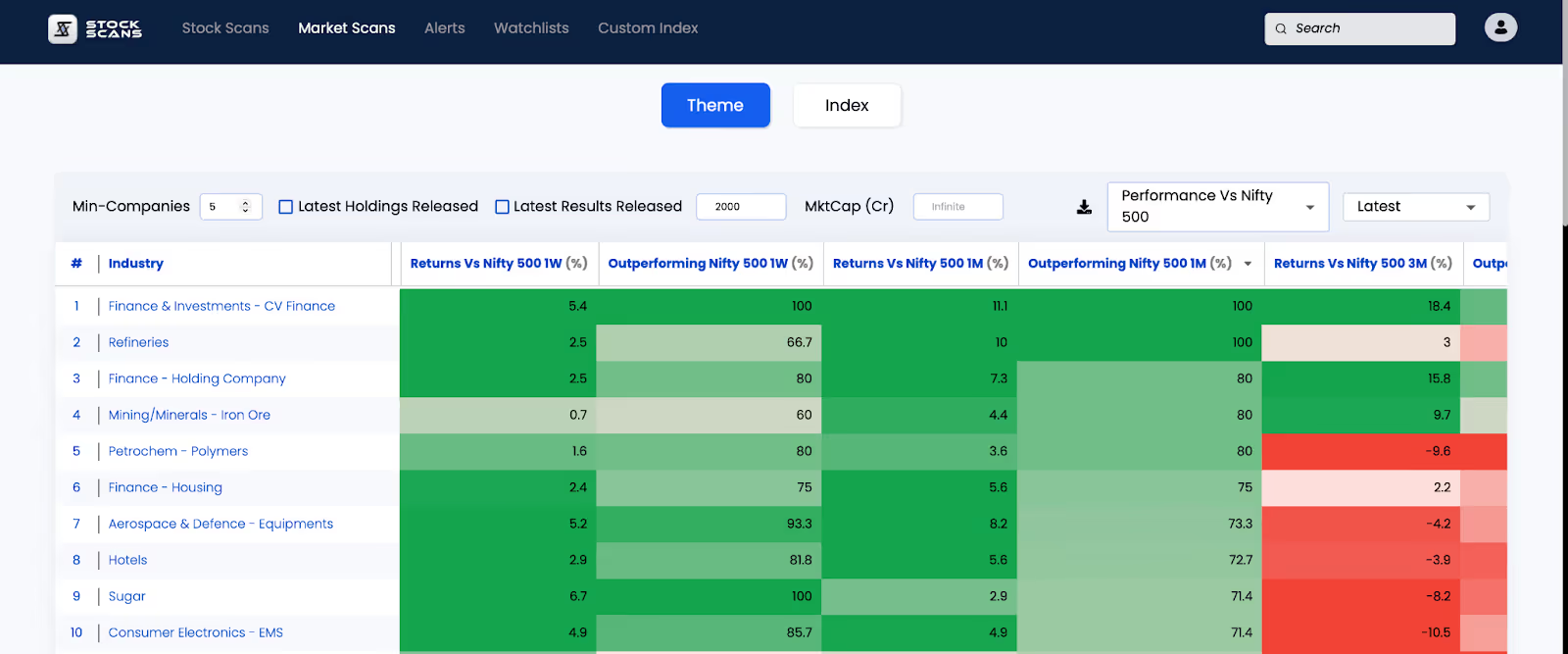

Current Strongest Themes

These are the Top 10 themes that are outperforming the Nifty 500. Prices have a lot of hidden stories and the ones that are outperforming have some special ones hidden within.

Interesting to see few new names pop-up here as EMS, Hotels, Mining and Minerals, and Sugar.

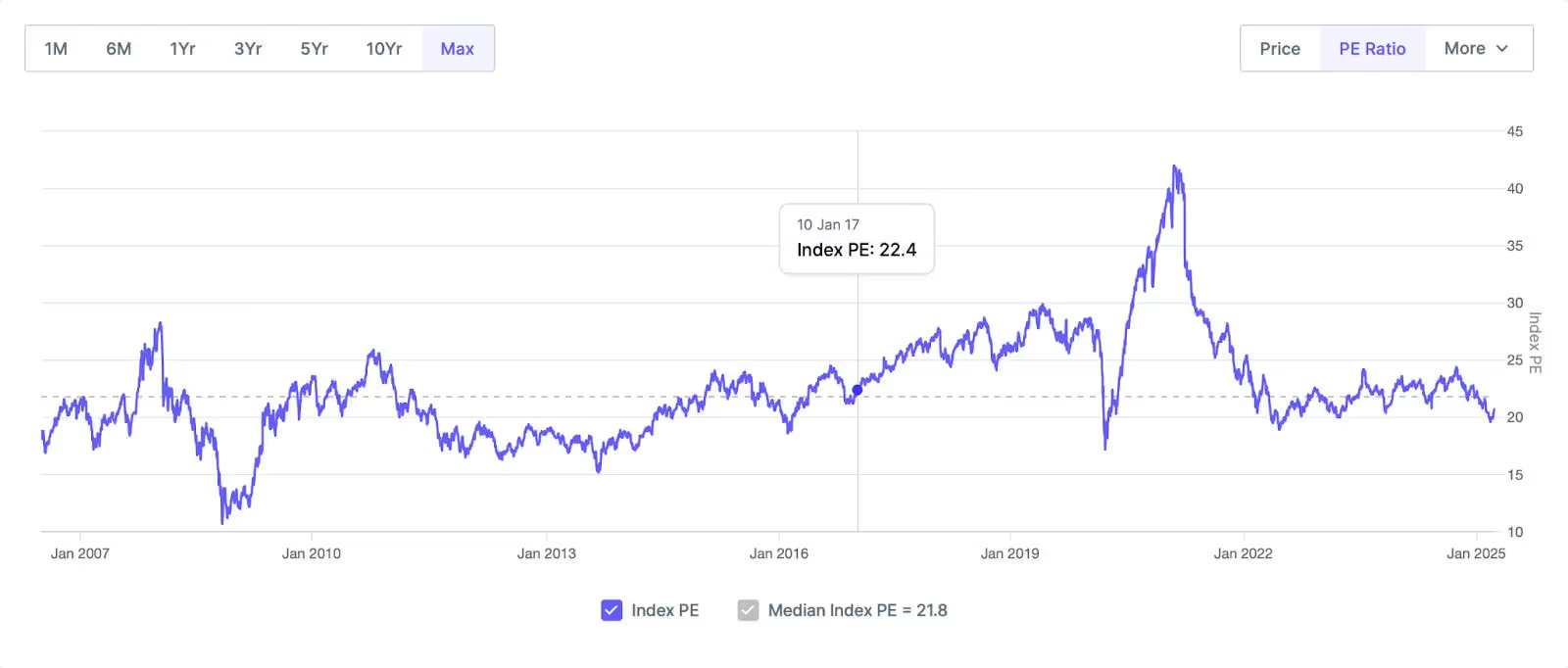

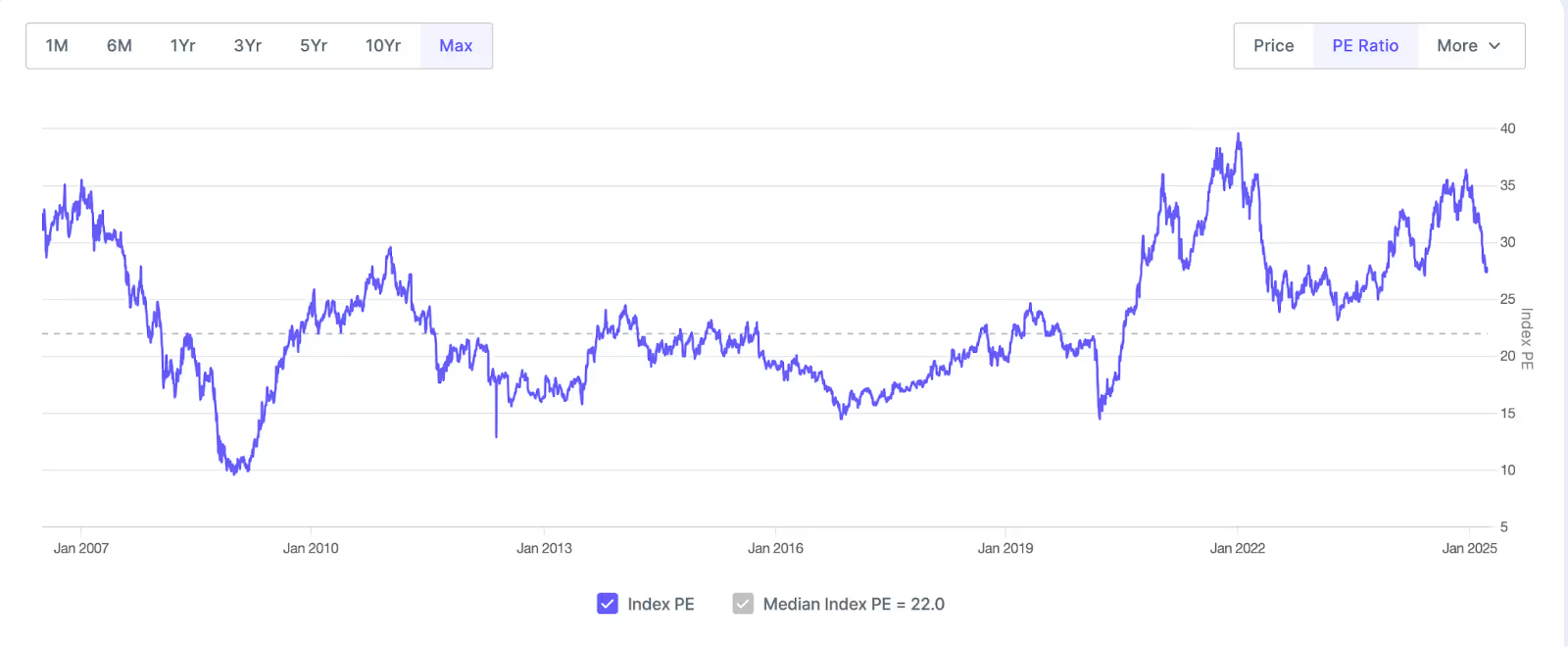

Valuation Check

Nifty Bank is another index that is trading below its historical valuations. Nifty bank has been more or less sideways from the past 1-1.5 years. Might be interesting to keep this one in the watch.

Nifty Bank is another index that is trading below its historical valuations. Nifty bank has been more or less sideways from the past 1-1.5 years. Might be interesting to keep this one in the watch.

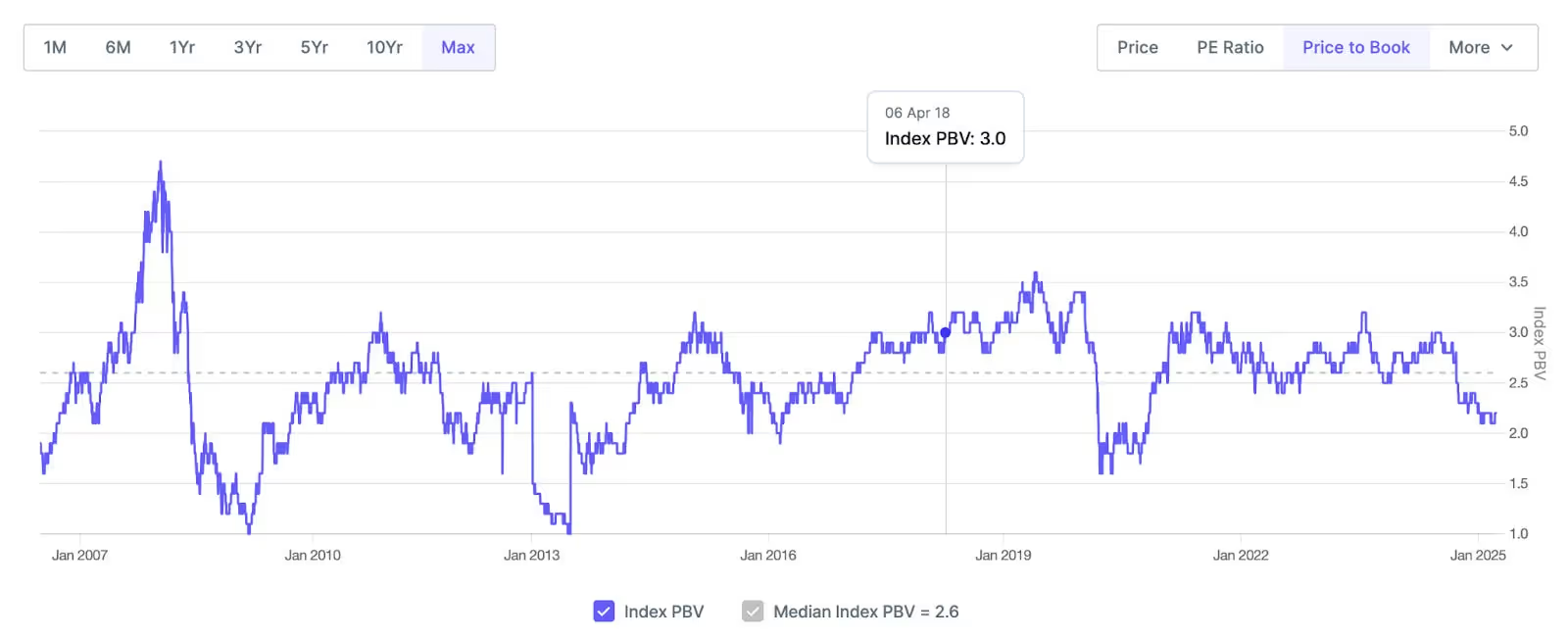

Nifty FMCG even after all the beating that has been done is still above the historical averages. Seems to be in the similar phase like it was between 2000-2008 when we were in an investment led GDP growth.

Nifty IT shows the similar aspects here of very slow growth expectations and higher than average multiples for the IT services companies.

Accenture Drawdown — A Reality Check for the IT Services Industry

Accenture reported 2QFY25 revenue of $16.7 billion, marking an 8.5% YoY growth in constant currency. However, its FY25 revenue guidance was tightened to 5-7%, signalling caution due to continued weakness in discretionary IT spending.

The results highlight key trends shaping the IT services sector:

✅ Cost optimisation over new spending

✅ Managed Services outperforming Consulting

✅ Sector-specific demand – Financial Services (+11% YoY) and Healthcare (+10% YoY) led growth, while discretionary-heavy industries like hi-tech and retail remained soft. ✅ GenAI as a future growth driver – Accenture secured $1.4 billion in GenAI bookings this quarter, reflecting strong demand for AI-driven efficiencies.

And all the while large cap IT names were getting beaten down very badly with the names like INFY, Accenture, HCL Tech are down close to 15-20%. In a month this is a really bad performance for the large cap IT companies. Below is a chart of Indian IT businesses and Accenture over last 30 days.

Management Meet Corner — SOIC Research

Arvind Fashion — A branded fashion play with inventory hygiene in place

The company currently operates 5 brands: USPOLO, FM, ARROW, CK, and TOMMY.

Inventory management is crucial for staying competitive; inventory days should ideally range between 80-90 days, with anything over 90 days being unacceptable.

Return on Capital Employed (ROCE) and Free Cash Flow (FCF) generation are key business priorities.

Despite reducing the number of brands from 15 to 5, the company achieved its highest-ever revenue in FY25, compared to ₹1900 cr. in FY21.

The brand FM is expected to start contributing to the bottom line soon, with H2FY25 considered its lowest point.

The company aims for a long-term growth rate of 12-15%, driven by store additions, premiumisation, digital expansion, and growth in adjacent categories.

Women's wear presents growth opportunities in top/bottom wear, footwear, and bags & accessories.

The casualisation trend is here to stay, requiring a differentiated strategy to create demand; Arrow New York was launched specifically for this trend.

The company is a top quartile performer in terms of LTL growth.

While there's currently no evidence of improving consumer spending, macro triggers are expected to drive improvement in FY26.

The store expansion plan includes increasing square footage and adding 1.5 lk sqft per year, with average store size being larger than before.

The company operates on a 65% Franchise Owned Franchise Operated (FOFO) and 35% Company Owned Company Operated (COCO) model. FOFO increases short-term return ratios, while COCO is better in the long run. FOFO inventory is held on Arvind's balance sheet.

There are no plans to introduce new brands currently.

The company aims to be debt-free and expects working capital days to remain stable.

FM's performance is expected to improve significantly two quarters after H2 FY25.

Inventory improvement is attributed to growth in the core business and inventory vectoring.

Goldiam — LGD Beneficiary

Business Growth and Expansion

The initial target is to establish 25 company-owned and operated (COCO) stores within the next 2 years, focusing on securing prime locations early on.

Subsequently, the company plans to adopt a franchise model.

The first COCO stores are expected to open in NCR and Bangalore within the next 6 months.

The company aims to achieve a total of 150 stores in 3 years.

The focus is on premium trajectory; fast fashion is not the company's goal.

Store Economics

Average selling price (ASP) per store is ₹56-57k.

Store size is 800 sqft, with a cost of ₹6-6.5k per square foot.

Rental deposit is ₹40 lakhs.

Total store opening cost is ₹90 lakhs.

Inventory requirement is ₹1.1-1.2 cr. for regular stores and ₹2.2 cr. for big stores.

All stores achieve breakeven within the first month, with a breakeven point of 30 lakhs of monthly revenue.

Stores with ₹40-45 lakh monthly revenue can have strong flows to PBT.

Online Sales

The company has seen a real pivot post-Covid with the online jewellery trend in the US.

Customer behaviour has been favourable towards online purchases.

E-commerce realisation of money takes 7-30 days.

Lab Grown Diamonds (LGD) vs. Natural Diamonds

Average realisation for LGD is 1.5 vs. 0.5 for natural diamonds.

A few test orders have been received for 5-10 carat LGD diamonds.

LGD prices have been stable in the B2B segment for the past 6-7 months.

There was a ₹10 cr. inventory write-off last year.

LGD prices may decline further by 5-8% over the next year, but seem to have mostly bottomed out.

Prices for LGD diamonds up to 5 carats are expected to stabilise.

The largest LGD growers in the US, Ukraine, and Russia have shut down, and no incremental industry capacity is coming in.

Buyers are looking to purchase LGD diamonds in bulk.

Other Considerations

The top 3 customers in the US account for 55% of sales.

The company has 25 eco-friendly machines, with no plans to increase this number.

Inventory risk management and design are key focus areas.

The industry is seeing a shift from single-digit to 80% incremental sales in LGD.

Forward Integration and Margins

Forward integration into jewellery manufacturing and retailing will drive margins and ROCE.

The ORIGEM brand focuses on everyday fine jewellery with lower price points for studded pieces.

The company has a cost advantage and a 20-30% price benefit due to internal manufacturing.

A centre stone setting factory is being planned in the US, with a ₹15-20 cr. outlay and a 3-4 month decision lag.

The order book has a 3-5 month lead time.

Consignment sales amount to ₹150 cr.

There is an 18% differential between loose and finished diamonds in India.

All-natural diamond centre stones are set in the US.

Ram Ratna Wires — ₹700 cr. capex plan

Emerald Copper Wires:

The total organised market share in India is approximately 150,000 tons.

The organised market share could be between 150,000 to 175,000 tons.

Ram Ratna Wires' current market share in this segment is around 15 to 17%.

The business has slim profit margins (P&L).

Copper Tubes:

The current market size is around 1 lakh tons, with 90-95% being imported, primarily from China.

Within one year, the import percentage is expected to decrease to 50%, and in two years to 20%, with 80% being domestic production.

The ideal sustainable EBITDA per ton for the copper tube business (specifically the Baroda unit) should be close to around ₹50,000. The earlier mentioned ₹70,000 is not considered sustainable.

For the Bhiwadi unit, a more realistic EBITDA per ton to consider is around ₹35,000.

Ram Ratna Wires' current Baroda unit has a capacity of approximately 600 tons per month.

The new Bhiwadi plant for copper tubes has a capacity of 24,000 MTPA (Metric Tons Per Annum).

The total capex planned is ₹700 crore across various segments, out of which the capex for copper tubes will be around ₹350 crore (including land and building).

Ram Ratna Wires has applied for a PLI (Production Linked Incentive) benefit on a capex of ₹250 crore for copper tubes.

The estimated PLI benefit over five years is around ₹150 crore to ₹160 crore.

The total copper tube market is expected to grow, with some anticipating it to reach 180,000 tons.

The cumulative supply capacity expected in the next two to three years is around 125,000 tons.

Capex and Expansion Plans:

The total planned capex of ₹700 crore includes:

Around ₹350 crore for copper tubes.

Around ₹200 crore for copper foil business, with revenue expected in FY27-28.

The remaining for forward integration products.

The copper foil business is expected to generate revenue approximately 6.5 to 7 times its EBITDA per ton.

The current financial year (FY25) is a heavy capex year, with a gross block expected to be around ₹520 crore. The net capex for the year is estimated to be around ₹200-₹250 crore.

The capex for the next financial year (FY26) is projected to be around ₹80 crore.

Capex could accelerate to around ₹200 crore in the following year (potentially FY28-29) depending on the performance in FY26.

A capacity expansion of 6,000 tons is planned for the Enamuled Copper Wire segment at the Silvassa plant.

Subsidiaries:

Epoova: A capex of around ₹80 crore is planned for this year and next year to add a capacity of 2 lakh motor air condition motor manufacturing units. The plant is expected to commence operations and start showing numbers from October-November onwards. The target asset turnover for E-Power is initially around 2 times, eventually aiming for 3 times.

Tefa: Ram Ratna Wires has bought a 60% share in this steel fabrication company. With a capex of ₹5 crore, it can generate an annual EBITDA of ₹11 crore to ₹15 crore. The target is to scale the EBITDA of Tefa to ₹40 crore to ₹50 crore in the next five years.

Raw Material and Competition:

The majority of copper raw material is sourced domestically, primarily from Hindalco and Vedanta.

Hindalco is also setting up a copper tube plant with a capacity of 24,000 to 25,000 tons per year, expected to go live around the same time as Ram Ratna Wires' Bhiwadi plant.

Other major players in the copper tube space include Kutch Copper, Hindalco, and MetTube, along with a few other smaller companies.

Exports:

The export volume is expected to remain around 8 to 10% of the total volume, with no significant jump anticipated.

Funding:

The capex will be funded through internal cash accruals, improved working capital management (reduction in cash sales days from 65 to 30), and proceeds from the sale of a 1.2% shareholding in RR Kabel in 2022.

A loan of ₹25 crore has been approved as a contingency if required to manage the quick ratio and current ratio during the capex phase.

There are no current plans for equity dilution.

Key market Announcements

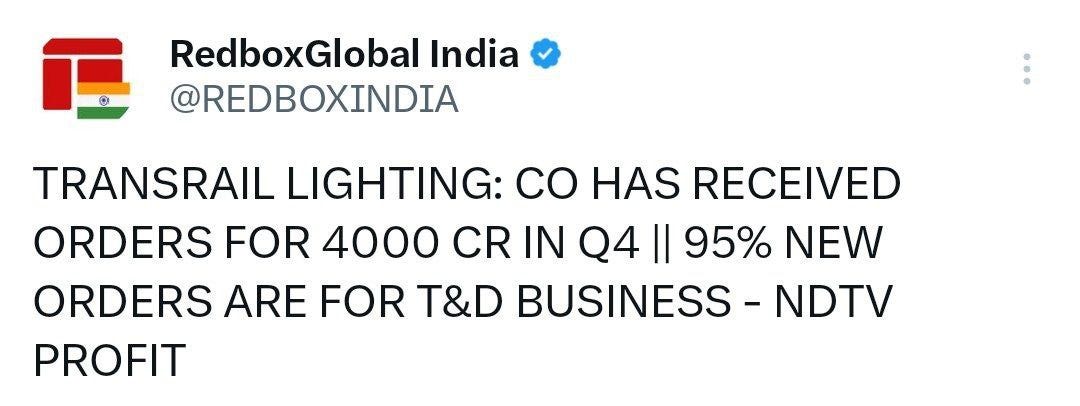

Transrail Lighting Limited wins new orders of ₹1,647 cr. for T&D in Railway business, with year-to-date (YTD) order inflows close to ₹9,200 cr.

Ultratech increased cement capacity by 1.2MTPA - Company’s total domestic grey cement manufacturing capacity stands at 178.86 mtpa. Along with its overseas capacity of 5.4 mtpa, the Company’s global capacity stands at 184.26 mtpa.

The Adani Group, through Renew Exim DMCC, launched an open offer to acquire up to 26% of ITD Cementation India Limited's (ITDCEM) equity shares, representing 4,46,64,772 shares, at ₹571.68 per share, following the acquisition of 46.64% from the existing promoter, Italian Thai Development Public Co. Ltd.

Zydus receives final approval from USFDA for Apalutamide Tablets, 60 mg

G R Infraprojects received LOA for Agra-Gwalior project. - ₹4262.78 cr

Glenmark Pharma expands cardiometabolic portfolio with the launch of Empagliflozin and its fixed-drug combinations in India

Steel exchange capacity increase:

The board acknowledges a healthy order backlog of approximately ₹180 crores and a near-term order pipeline of about ₹450 cr. in Quality Power Electrical Equipments Ltd.

TARIL secures ₹726 cr. order from Gujarat Energy Transmission.

Maharashtra Seamless has received an order with a basic value of ₹298 cr. approx. for supply of seamless pipes.

NCC Received a major order worth ₹2129.60 cr. and an order of ₹1,000 cr. for the redevelopment of Darbhanga Medical College & Hospital at Laheriasarai, Darbhanga.

Bain capital is investing ₹4385 cr. in Manappuram finance (change in management). Manapurram has always traded at a discount to Muthoot; can this be the trigger to narrow the discount?

Management restructuring happening in Bajaj Finance. Elevates Mr. Rajeev Jain to the post of Vice Chairman for 3 years, effective April 1, 2025. Also appoints Mr. Anup Kumar Shah as MD for 3 years. He is currently holding the post of Deputy MD.

Salzer received an order worth 50 cr. for smart meters

Force Motors — saw a splendid 48% of growth led by the strong domestic business for the company

Muthoot Finance crosses Gold Loan AUM crosses landmark milestone of ₹1 Lakh cr. mark

Glenmark launches two new Diabetic drugs

Key Business Updates

Feb 2025 Auto sales update

Domestic business and export sales

IPM FEB 2025 data February was a moderate month:

Volume growth decreased 0.2%, Price growth of 5.2% and new launches increased 2.4% in this month

Out-performers

Zydus lifesciences led the market share with the highest growth at 12.7%, followed by Ajanta pharma (11.8%) and Torrent pharma (11.6%)

FDC and JB chem also performed well with giving 11.3% and 11% growth respectively

In-line performers

Mankind and Glenmark showed in-line growth both showing 7.8% growth

Under Performers

Cipla and Eris Life Science had slower growth at 5.3 and 5.4% respectively

Market Moving News

Impact of the Safeguard Duty on Steel imports

Protection for Domestic Industry: The Director General of Trade Remedies (DGTR) has recommended a provisional safeguard duty of up to 12% on flat steel products for 200 days. This move aims to protect the local steel industry. The duty is recommended on products like HR, CR, flat products, coils, and plates.

Potential for Price Increases: Domestic steel prices had already increased by roughly ₹2,500 per ton (around 5%) prior to this announcement. With the 12% duty, domestic producers now have headroom to potentially increase prices further, possibly by another ₹2,500 or 3-4%. Experts anticipate a near-term price hike of around ₹2,000 to ₹2,500. Historically, safeguard duties have led to price increases of 10-15% over the following months.

Improved Profitability (EBITDA): The price hikes, coupled with potentially lower coking coal prices compared to the previous quarter, are expected to lead to a better EBITDA per ton for steel companies. Anand Rathi estimates a potential 10% EBITDA/t improvement across the flat steel sector. Q4 is generally considered the best quarter for EBITDA, and the safeguard duty is likely to further enhance this.

Level Playing Field: The Indian steel industry has been demanding a level playing field to compete with imports, particularly from countries like China and Korea, which they believe are sometimes due to dumping and subsidies. The safeguard duty is a step towards addressing this demand.

Beneficiaries: Companies with a larger proportion of their portfolio in flat steel products are expected to benefit the most. These include Tata Steel (around 76% flats), JSW Steel (71%), and Steel Authority of India (SAIL) (around 60%). Analysts believe this is a significant positive for SAIL, JS Steel, and Tata Steel. Also Steel convertors will be benefitted by this move

Demand Outlook: Domestic demand in India is currently good and robust, supported by infrastructure pushes from the government. This strong domestic demand provides a favorable backdrop for the price increases enabled by the safeguard duty.

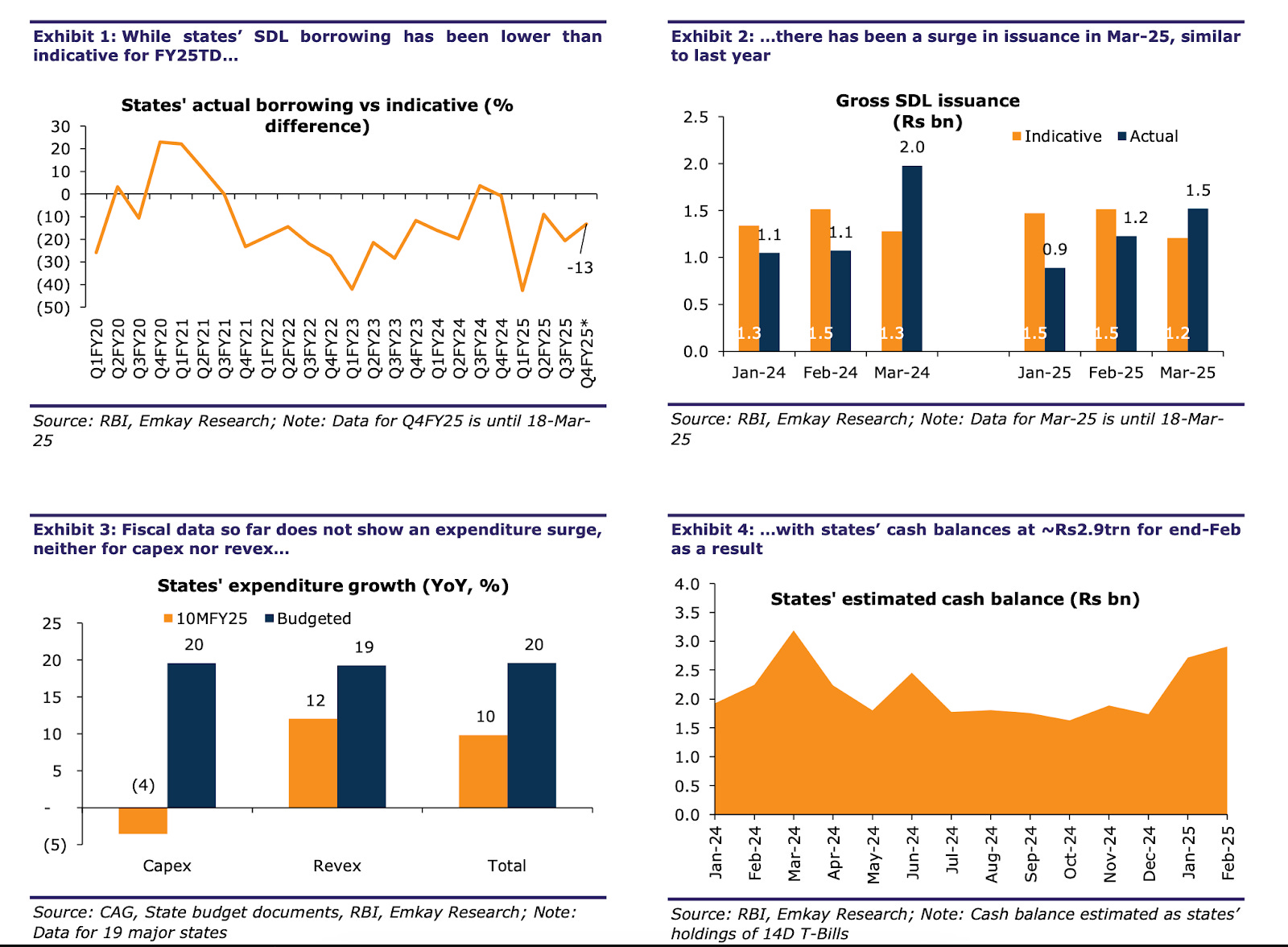

State Capex is not able to match the increase in State borrowings

State budgets are under strain! Despite weak revenue growth, the FY25E fiscal deficit is set at 3%, surpassing last year’s 2.8%. Among 10 major state budgets for FY26, half show worsening or stagnant revenue balances.

Maharashtra (MH) has cut its ‘Ladki Bahin’ scheme allocation to ₹360 billion (from ₹460 billion in FY25BE) by trimming beneficiaries, while its revenue deficit to GDP is rising from 0.6% to 0.9%.

States may try to rationalise welfare spending, but there’s no turning back now—discretionary capex is likely to take the hit.

There are also large unspent policy money and also Most states have reduced their Capex budget estimates.

Where insiders are showing interest

The top sectors and the names where most of the insider buying was seen in the past week

TDPOWERSYS, WESTLIFE, is one of the names where promoter buying continued even in the current week, although in the smaller numbers

Few of the new names where promoter buying became visible — Poonawala, Senco, FSL, Sunteck, Control print.

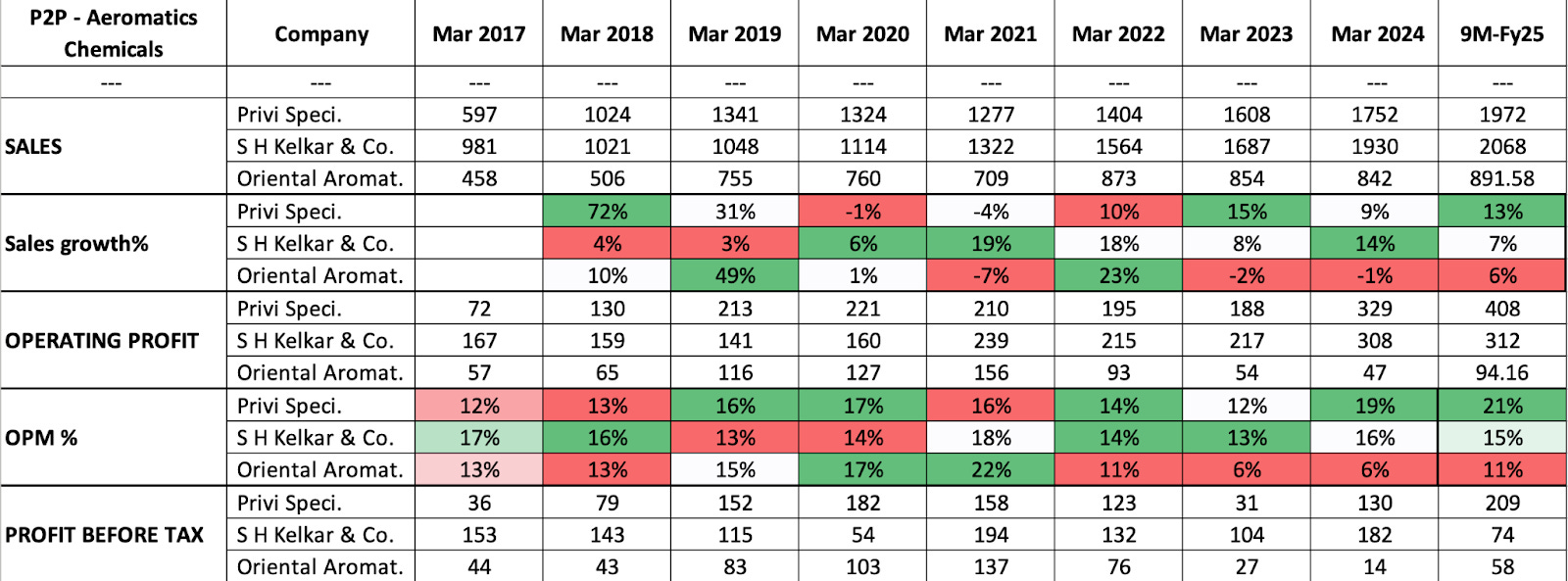

P2P Analysis

Aromatic Chemical Industry — shows why Privi stands above the rest

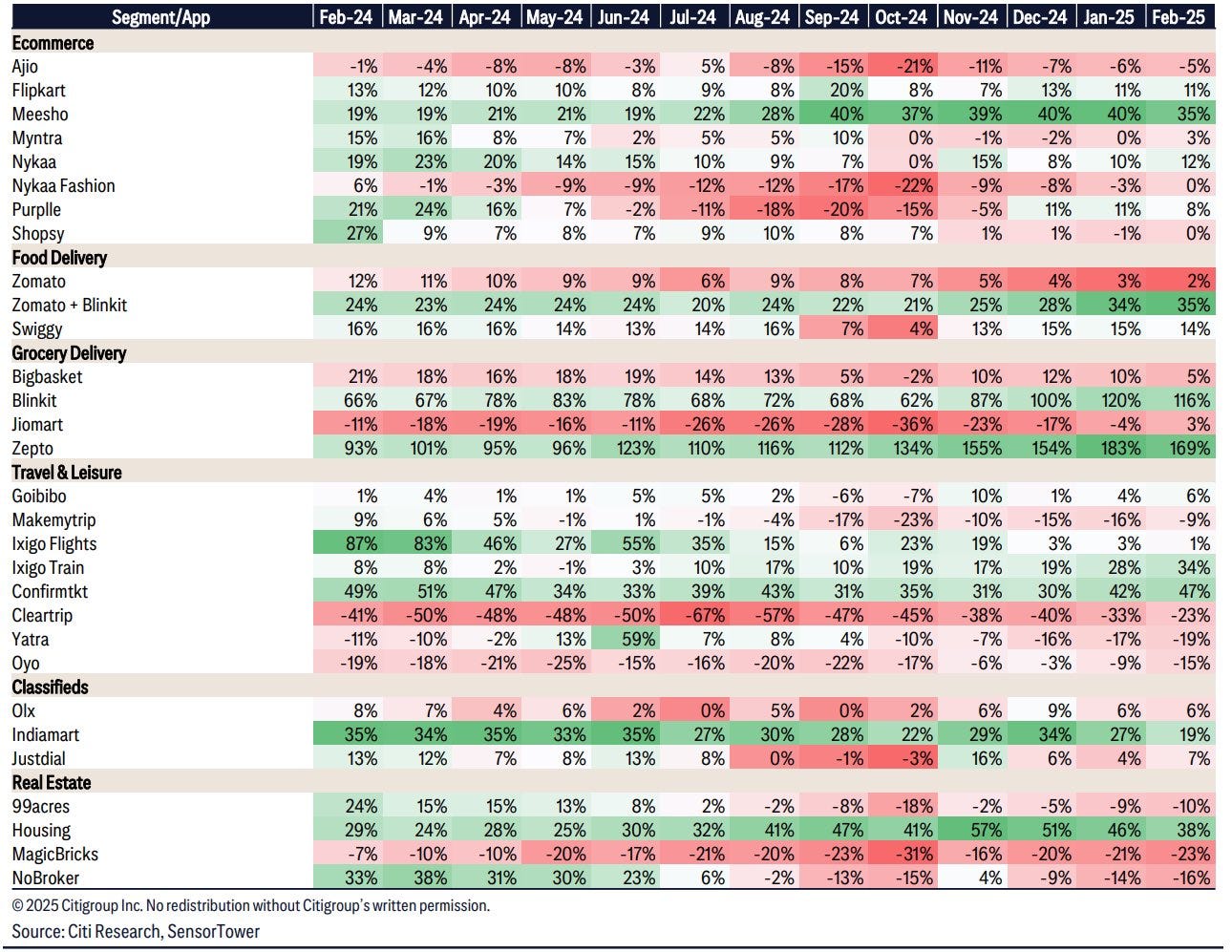

Platform Business app downloads month on month growth

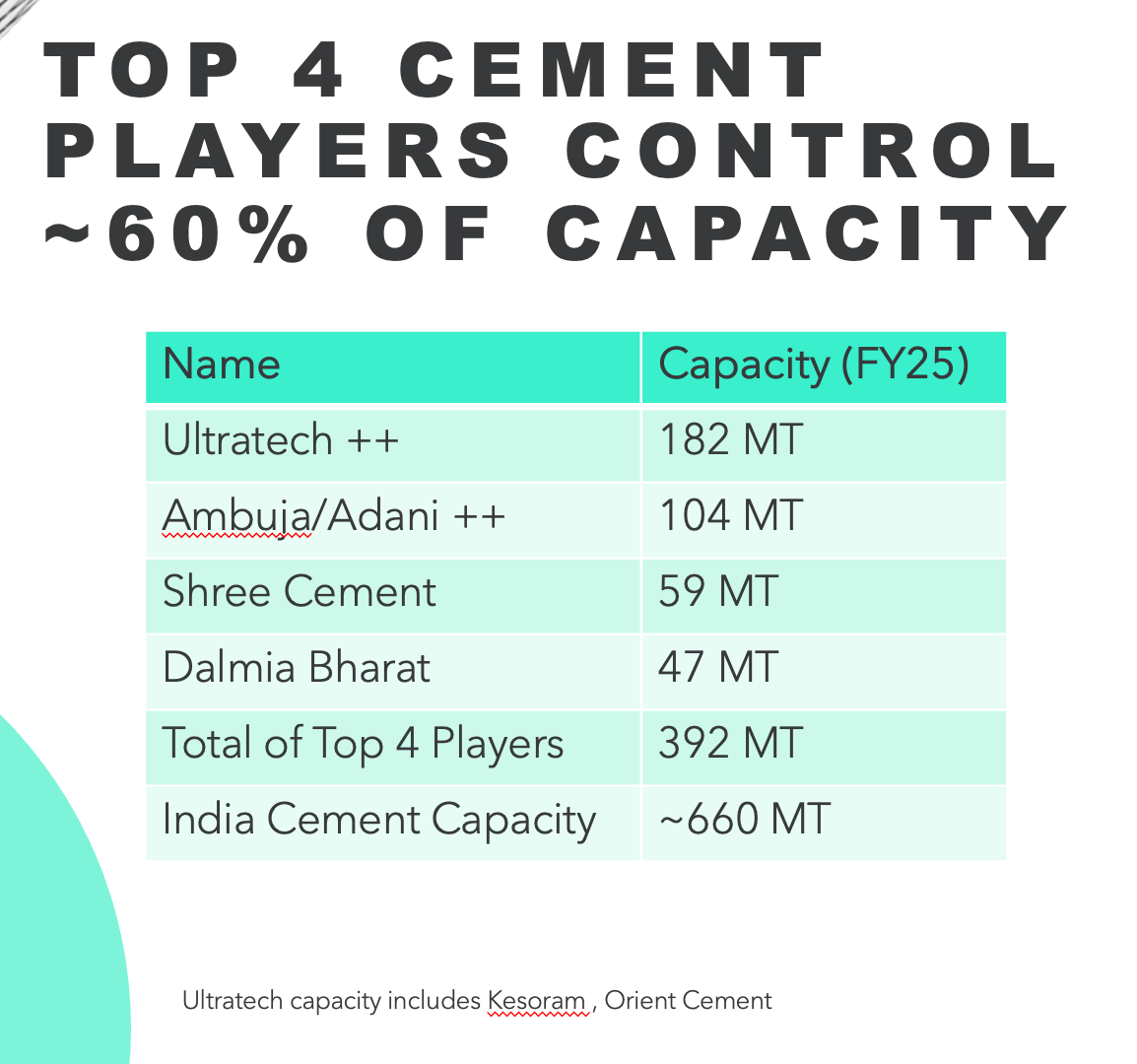

Is Cement in Peak Pessimism?

1. Profitability is at the lowest in the past 15 years

2. Net realisation has also been stagnant

3. Consolidation in the industry is almost done

Source: Ashwini Damani TIA Presentation

A Book Worth Reading

Clear Thinking: Turning Ordinary Moments into Extraordinary Results

This book will help you make better decisions. As a stock picker it is important to have a clear mind and ability to make strong decisions and this book should help with the same.

We host a biweekly video series called Insights with SOIC, where we break down all the key developments in the markets and share interesting updates for our members.

As a bonus, SOIC Membership also gives you full access to our in-depth course on Fundamental Analysis—perfect for building strong investing foundations.

Both the video series and the fundamental analysis course are included as part of your SOIC Membership.

The information provided in this reference is for educational purposes only and should not be considered investment advice or a recommendation. As an educational organisation, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

%20(1).avif)

%2016_9.avif)

0 Comments