India’s Aerospace & Defense: From Import Dependency to Global Command — A Structural Transformation in Motion

BY

Shuchi Nahar

Industry Trends

Market Trends

The Decade That Changed India’s Defense Narrative

A decade ago, India’s defense manufacturing was largely reactive, policy-driven, and import-dependent. Procurement cycles were slow, and technological advancement was limited. The ecosystem was dominated by Defence Public Sector Undertakings (DPSUs) — HAL, BEL, BDL — and the role of private industry was minimal.

Fast forward to 2025, the story has been re-written. India is now designing, assembling, and exporting sophisticated systems — from Tejas fighter jets and Akash missiles to Prachand light combat helicopters and Pinaka artillery systems.

Exports have surged from a modest ₹6.8 billion in FY14 to ₹236 billion in FY25, and India now features among the top 25 arms exporters globally. This shift is not merely industrial; it is strategic and structural, with private sector players and startups now integrated into the nation’s security and technology framework.

At the heart of this transformation lie three structural drivers:

Rising Domestic TAM (Total Addressable Market): Expected to increase 6x over the next two decades, reaching ₹10 trillion (~$122 billion) by FY47.

Indigenisation of Defense Manufacturing: From less than 40% to potentially 70%+ over the coming decade.

Global Integration and Export Ambition: The government’s goal of ₹500 billion ($5.8 billion) in exports by FY29 and the opening up of the global supply chain to Indian firms.

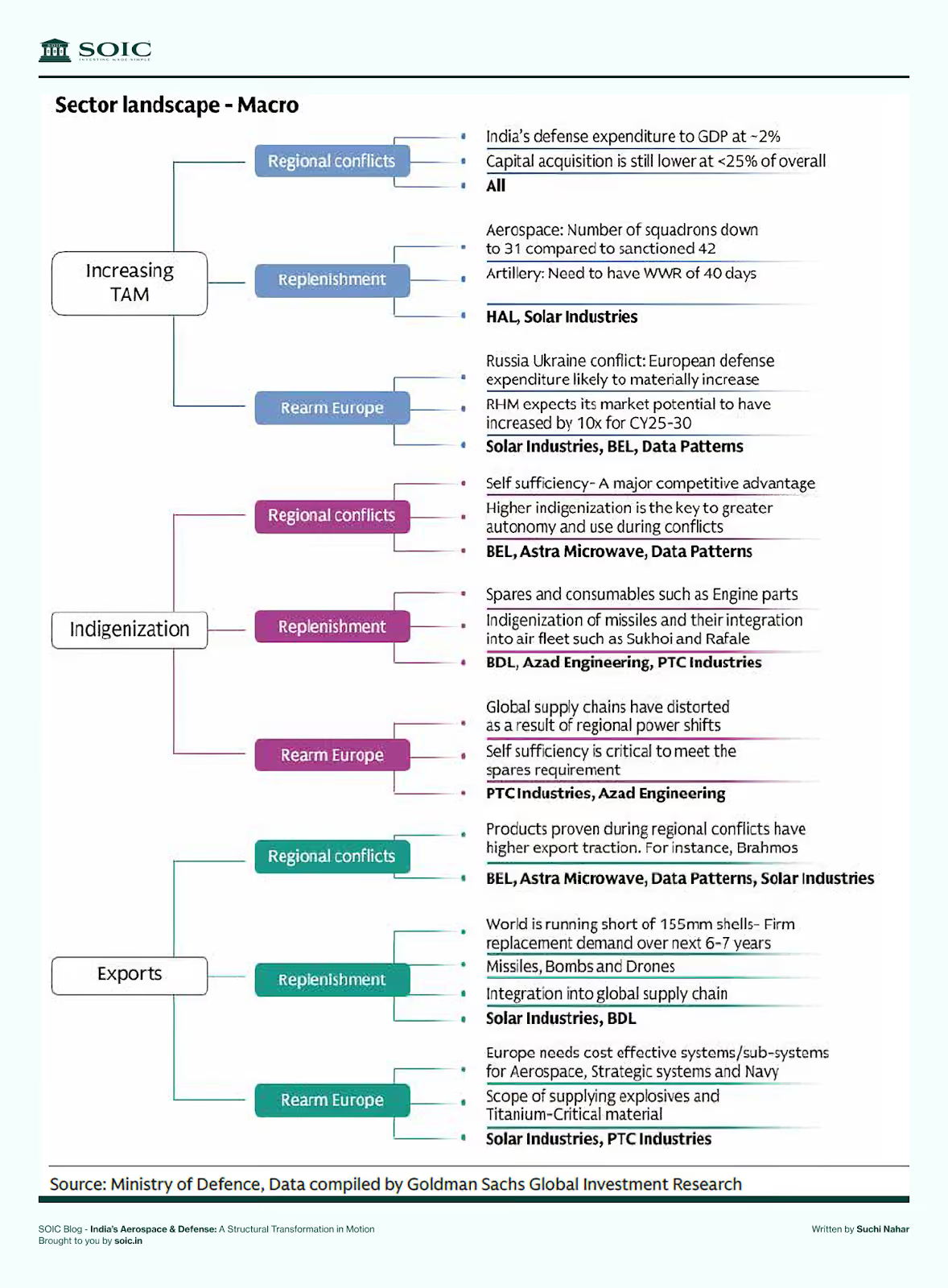

The Macro Landscape: India’s Strategic Repositioning

India’s defense posture is evolving from defensive protectionism to strategic assertiveness.

Historically, defense expenditure has averaged around 2% of GDP, far below that of neighboring countries like Pakistan (3.7%) and Russia (4.2%). Yet, India remains the fifth-largest global defense spender with an annual outlay of over $80 billion (FY25).

The capital allocation mix is shifting:

Capital outlay — the portion of the budget used for equipment procurement — is expected to rise from 25% in FY25 to 36% by FY47.

Revenue expenditure (salaries, pensions, maintenance) will gradually compress as technology-led efficiency improves.

Over time, this creates a multi-decade earnings tailwind for defense manufacturers, particularly those exposed to high-technology platforms.

Defense spending correlates with geopolitical cycles:

1962 China War → Spending surged from 2% to 4.8% of GDP.

Kargil Conflict (1999) → Modernisation focus led to a multi-year capex boom.

Post-Galwan 2020 → Triggered the “Atmanirbhar Bharat” defence manufacturing thrust.

Current context:

With China’s military buildup, border tensions, and regional instability, India’s defence modernisation cycle appears secular, not cyclical. Moreover, global rearmament (EU’s “Readiness 2030 Plan” with €800+ billion spend) presents export openings that were absent in prior decades.

The Future Battlefield: Digital, Autonomous, and Networked

The Technology Perspective and Capability Roadmap (TPCR 2025) outlines India’s next 15-year defence vision across four domains:

The evolution toward AI-enabled warfare, network-centric operations, electronic countermeasures, and cyber-resilient communication will shape the next phase of value creation.

Structural Growth Drivers in Detail

Rising Total Addressable Market (TAM)

Capital outlay projected to grow 6.8% CAGR through FY47.

Total Defence Capital Spend: ₹1.6 trillion in FY25 → ₹10.4 trillion by FY47.

Bull case: 2.5% of GDP allocation with 50% capital share = ₹19.5 trillion market.

Investor Insight:

Unlike past cycles, where budget growth was linear, this time structural reforms — including FDI liberalisation (up to 74%), technology transfer, and joint ventures — enable a multi-layered supply chain opportunity: primes, subsystems, components, materials, and MRO.

Indigenisation — The Core of Strategic Autonomy

India remains the second-largest importer of defence equipment, accounting for 8.3% of global imports (2020–24). Yet, import dependency has sharply declined — from 62% in FY02 → 12% in FY25.

Navy: 100% indigenisation in float components, 80–90% in propulsion (“move”), but <40% in weapons (“fight”) systems — a white space for radar, sonar, and electronic systems.

Airforce: Heavy dependence on foreign suppliers for engines, radar electronics, and avionics — significant room for import substitution.

HAL: Raw material imports still >75%; BDL: import content <5% — showing the contrasting progress within DPSUs.

Indigenisation lists:

Five positive indigenisation lists: 5,012 items earmarked for local manufacturing; 3,000+ already indigenised.

New opportunities: Aeroengine components, radars, EW systems, UAVs, and processed titanium/superalloys.

Investor KPI: Track the import content (%) of Value of Production (VOP) for each player. A declining ratio signals improving competitiveness and better control over margins.

Export Acceleration — The Global Push

India’s defense exports have compounded >40% CAGR since FY14, with the private sector now contributing 65% of total exports despite only 35% share in domestic output.

Key product lines gaining traction:

Ammunition and energetics (Solar Industries, Munitions India)

Aeroengine castings and Ti alloys (PTC Industries, Azad Engineering)

Radar electronics and EW systems (Data Patterns, Astra Microwave, BEL)

€800 billion earmarked for rearmament by 2030; focus areas align with Indian capabilities (ammunition, drones, radar electronics).

NATO benchmark raised to 5% of GDP for defence by 2035.

Creates an indirect export pipeline for Indian midcaps integrated into the global supply chain.

Investor KPI:

Export revenue share (%)

Geographic diversification (Europe, MENA, ASEAN)

Contract tenure and renewal frequency

White Spaces: The Unaddressed Opportunities

1. Aero Engines & Components

India’s fighter jet squadron strength has fallen to 31 (vs. authorised 42). Orders for Tejas Mk-1A, Mk-2, and AMCA will create multi-decade component demand.

Opportunity size: Co-production of F-414 (GE) and co-development of AMCA engines.

Beneficiaries: Component ecosystem firms — PTC Industries and Azad Engineering.

Recurring revenue: MRO and lifecycle replacements (aerofoils changed every 3–6 years).

2. Radar Electronics & Communication

Nearly 50% of TPCR programs involve radar, EW, and networked systems.

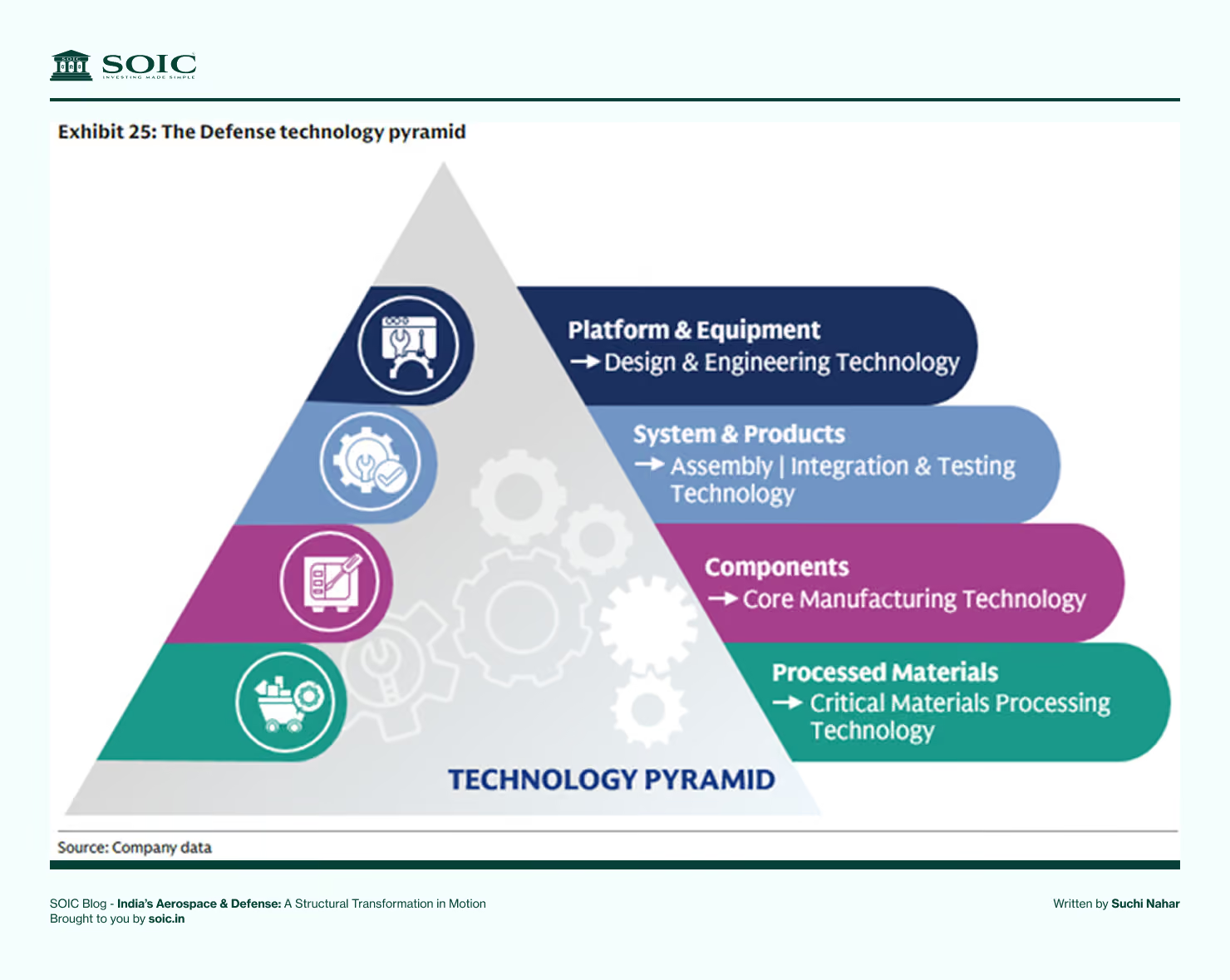

The distribution of domestic players across the technology pyramid and domains suggests that there are not many players at the bottom end of the pyramid across the platforms. Similarly, players with capabilities in the precision machining required for components are also not many.

The Private vs. Public Divide

The private sector’s capex-heavy cycle should not be mistaken for inefficiency. These companies are building new-age defense ecosystems — from materials to electronics — which are capital-intensive but high-return in steady state.

Investor KPI:

Capex efficiency (Incremental ROCE)

R&D capitalisation ratio (expensed vs. capitalised)

Customer concentration (Top 3 clients %)

Risks & Sensitivities

Policy allocation shifts: Any diversion of government capital from defense to social sectors.

Execution delays: Particularly in large aircraft and missile programs.

Global supply realignment: OEMs may shift sourcing away from India if reliability dips.

FX volatility: Impacts import costs for material-heavy firms.

Capex overruns: Can stretch balance sheets for private players in the build-out phase.

The Framework for Evaluating Defence Companies

When assessing defence manufacturers, investors should look beyond simple P/E ratios and focus on strategic performance drivers:

The Long-Term Opportunity — India’s Defence Renaissance

Over the next 20 years, India’s defence ecosystem could transform from a $19 billion market to a $120+ billion powerhouse, serving both domestic and global clients.

This is not just an “earnings story” — it’s an industrial transformation powered by policy continuity, private sector integration, and technology self-sufficiency.

The next decade will see:

Aerospace localisation: From engines to avionics

Electronics dominance: Indian radar systems exported globally.

Global supply linkages: Indian firms becoming Tier-1/Tier-2 suppliers to Western OEMs.

Export-led scale: Defence contributing $10–15 billion to India’s trade surplus.

India’s aerospace and defence industry is evolving from a government-led ecosystem to a technology-led ecosystem — a once-in-a-century structural shift.

For investors and analysts, the real value lies in tracking how capital, capability, and confidence converge across private and public players.

The key is not predicting who wins next quarter — but identifying who is building India’s next defence decade.

Disclaimer:

The information provided is for educational purposes only and should not be considered investment advice. As an educational organisation, our objective is to provide general knowledge and understanding of investment concepts. We are SEBI-registered research analysts.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

Industry Trends

Market Trends

Sector Analysis

Author

Shuchi Nahar

Masters in Finance with 5 years of industry experience. My approach is to take one sector at a time and explore plausible Investment ideas.

.avif)

0 Comments