%20(1).avif)

The Day “Waste” Looked Different

A few weeks ago, I was cleaning a drawer at home.

The kind where everything eventually ends up — old chargers, tangled wires, broken earphones, maybe even a dead phone that you keep thinking you’ll repair someday. Don't smile; I know everyone has that one drawer, even you :) I picked up one of those wires and instinctively moved toward the dustbin. Then paused.

Because suddenly, it didn’t look like a waste.

It looked like copper.

Not in its clean, shiny form — but still copper.

That drawer, if you really think about it, had:

All in small quantities. All ignored.

And that’s when a simple thought hit:

We don’t have a shortage of resources.

We have a shortage of systems to recover them.

Now scale that drawer across millions of homes, factories, batteries, electronics… And you start seeing the outline of something much bigger.

An Industry That Exists… But Was Never Seen Properly

Recycling in India has always been there. But it never really looked like an “industry”.

It looked like an activity.

It worked — but it didn’t scale.

It didn’t attract capital.

It didn’t attract attention.

And more importantly, it didn’t attract structure.

But that is slowly changing.

And like most structural shifts — it is happening quietly.

It’s easy to assume that recycling will grow because demand is increasing.

But the reality is:

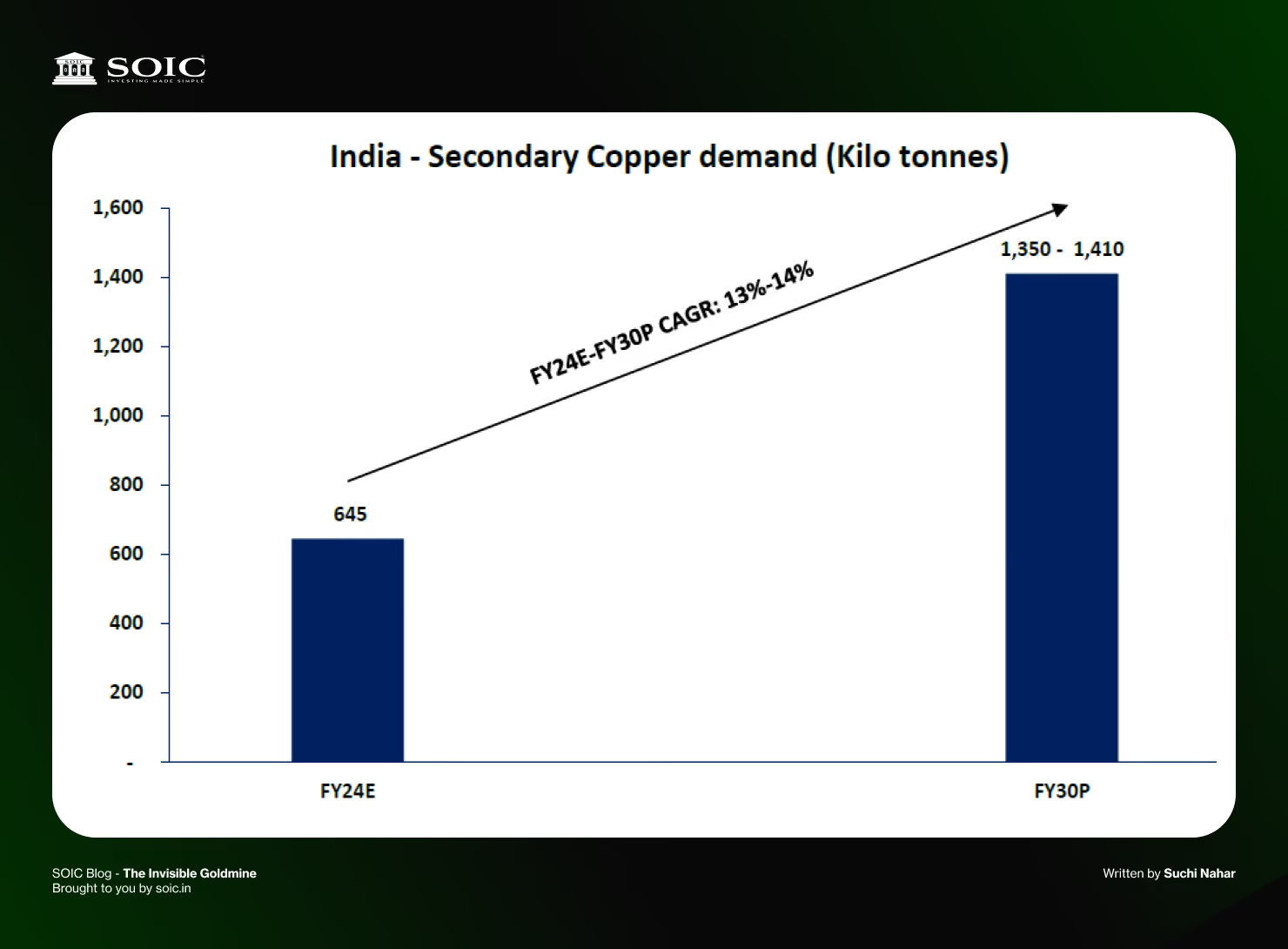

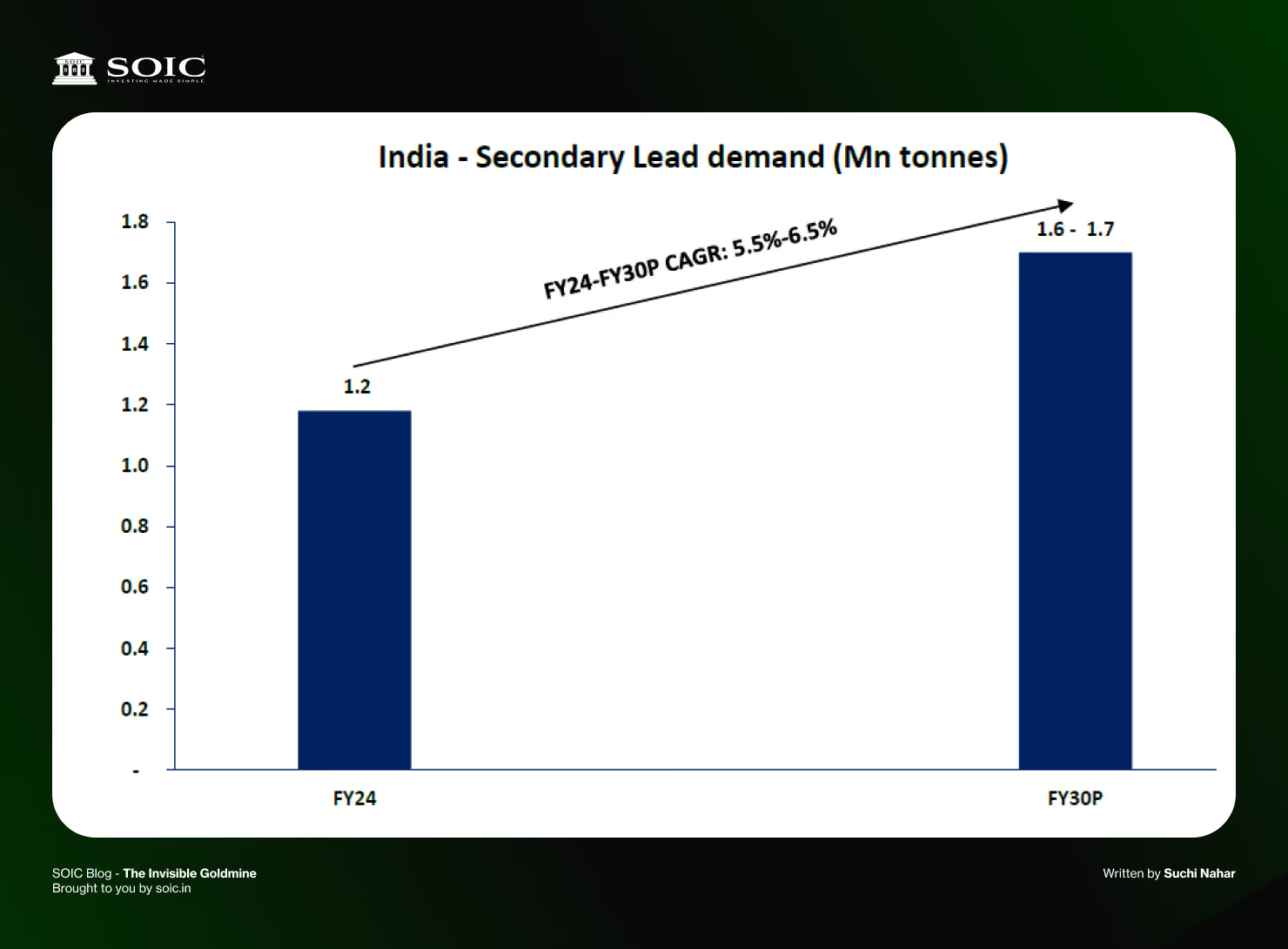

Demand for metals has always been strong.

The constraint was never demand — it was organisation.

From the data:

This is being driven by:

So the real question is not: Will demand grow?

The real question is: Who will be able to service that demand efficiently?

Earlier, the system was simple:

Scrap → Local dealer → Small recycler

Now, slowly, it is becoming:

Scrap → Organised collection → Compliant recycler

This shift is being driven by regulation.

These policies are doing something very important: They are forcing accountability into the system.

Producers now need:

And informal networks cannot provide that at scale. So naturally, volumes begin to migrate. This Is Not Growth. This Is Reallocation. And that distinction is critical.

This is not about the industry suddenly becoming bigger.

It is about: The same volume moving from unorganised → organised players

From the reports: Only ~35–40% of scrap is currently formalised

Which means:

The opportunity is not just in growth.

It is in market share shifting structurally

At its core, recycling looks like a commodity business.

But it isn’t entirely.

Because there are two very different ways to operate:

1. Price-led model

2. Conversion-led model

One is volatile.

The other is predictable.

And over time, that difference becomes everything.

At first glance, Gravita, Jain Resource, and Pondy Oxides look similar.

Same sector.

Same inputs.

Same outputs.

But once you look closer, you realise:

They are not competing the same way.

They are solving different problems within the same space.

It begins with scale — but not all scale is equal.

It starts with something as basic as capacity.

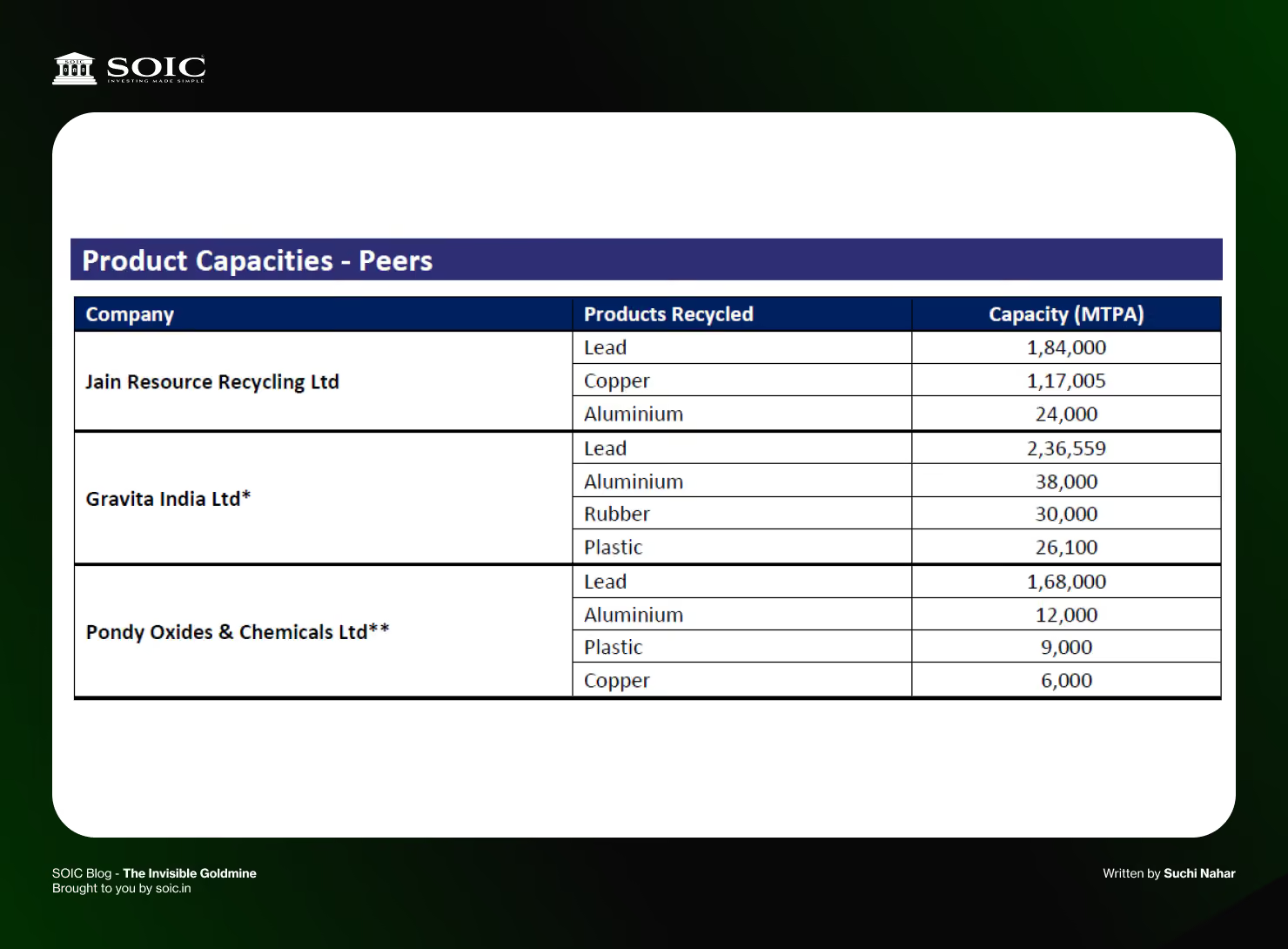

If you look at the numbers, all three have a meaningful scale.

Gravita has built a fairly diversified base with strong presence in lead and aluminium, and has also added plastics and rubber into the mix. Jain, on the other hand, stands out because of its significant copper exposure along with lead, while Pondy remains more concentrated with a relatively traditional mix across lead and smaller contributions from other segments.

At a surface level, all three look “scaled”. But the intent behind that scale is different.

This is where the real separation begins.

Business Model & Positioning

Gravita operates as a conversion-led, globally diversified recycling platform.

Its core philosophy is simple but powerful:

“Do not take commodity risk. Earn from processing.”

This creates:

Capacity & Expansion Roadmap

Current installed capacity:

Target:

Key Capacity Additions (Near Term)

Capex Plan

Geography & Presence

Sourcing & Raw Material Strategy

This gives:

Customers & Demand Nature

Operational Strength

Margins & Economics

Future Strategy

Gravita is not just scaling — it is transforming mix:

Also:

Core Strength: Structured, disciplined, capital-efficient compounding model

Its model is built around conversion, supported by LME hedging that protects it from price volatility. This creates a structure where margins may not look extraordinary, but they remain stable across cycles.

It behaves less like a commodity business, and more like a processing utility.

It is not just recycling — it is integrating forward.

From recycling scrap to producing higher value products like copper cathodes and rods, it is trying to move up the value chain. It also extracts by-products like tin and plastic to improve profitability without additional raw material cost

It is not just participating in the value chain.

It is trying to own more of it.

Business Model & Positioning

Jain is building:

A globally integrated, multi-metal + value-added platform

Unlike Gravita:

Product Mix

Also extracting:

Scale & Growth

Global Footprint

Customers

Capacity & Expansion

Copper — Core Focus

Forward Integration (Game Changer)

Jain Green Technologies project:

Products:

Capacity (phased):

Other Expansions

Sourcing Strategy

Working capital reflects this:

Margins

Lower because:

Hedging

Future Strategy

Two clear tracks:

1. Volume Growth

2. Profitability Growth

Core Strength

Scale + integration + global reach

represents the older structure — stable, functional, but not aggressively evolving its model. Margins tell the story without saying it directly

Business Model

Pondy operates as a:

Disciplined, efficient, value-added recycler

Less aggressive than Jain, less diversified than Gravita.

Capacity & Expansion

Growth Profile

Driven by

Customers & Markets

Sourcing

Margins

Strategy

Core Strength: Efficient execution + improving product mix

To summarise:

Gravita operates at ~10–11% EBITDA margins, which are relatively stable due to its hedged, conversion-led model. Jain operates at ~5% margins. At first glance, this may look like a weakness. But it is actually a reflection of strategy. Jain is choosing growth over margin. Gravita is choosing stability over speed. Neither is right or wrong. But they are very different. The most underrated moat — access to scrap. In mining, you own the resource. In recycling, you have to find it, collect it, and secure it.

Growth — fast vs durable

Jain’s numbers stand out immediately.

This is aggressive expansion.

Gravita, on the other hand, grows at ~20–25%:

Jain is sprinting.

Gravita is pacing.

Pondy is somewhere behind — steady, but not accelerating.

Strategy — where the future is being built

Gravita is evolving into a multi-material recycling platform:

Jain is expanding aggressively across:

One is building depth.

The other is expanding width.

Jain’s IPO valuation was ~35x earnings

Gravita trades at ~25–30x.

The market is already making a distinction:

The deeper insight — what the market may still be missing

Most investors still look at this as: “a metal business”

But increasingly, this is becoming: a supply chain + compliance + processing business

And that shift changes everything:

What are we really comparing here? Not companies.

But philosophies.

The Drawer Looks Different Now - I went back to that drawer again a few days later.

Nothing had changed.

Same wires. Same broken devices.

But it didn’t look the same.

Because once you understand how value is created, you start seeing things differently.

What looks like waste is often just: Value waiting for the right system to unlock it

And that’s exactly where India is today.

Not discovering recycling, but organising it.

And when something moves from:

It doesn’t just grow.

It compounds.

The real question, then, is not: Which company looks the cheapest today!

But:

Which company is best positioned to operate in a system that is only just beginning to take shape?

Because in such transitions, the biggest winners are rarely the loudest.

They are usually the ones quietly building the right foundations.

Disclaimer: The information provided is for educational purposes only and should not be considered investment advice. We are SEBI-registered research analysts.

We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference

0 Comments