I’ve realised over time that the things I love most in life are surprisingly simple.

A good cup of coffee to start my day with. Generally, I love drinking cold brew and you might find me at some Starbucks in Delhi someday. Silently sitting and enjoying the coffee while I read about different industries on my laptop.

Moments with family and friends, and especially with my nephew who has started aping whatever I do. He has become a Manchester United Fan, and has in his inquisitive way started asking me questions about what stocks are and why do I explain different businesses on Youtube?

Teaching SOIC students on Sundays. I must have taught about different mental models and about nearly 50+ industries over the last 5 years. Now, I am working on distilling all my key teaching in a checklist type class, TVGP framework, which will be announced soon.

Finally, playing football or paddle with friends and working out at the gym. There is something therapeutic in exercise. I have been tracking all my body vitals and signs of fitness using Whoop. It has become an addiction lately to check my sleep consistency, recovery, and VO2 max. As a wise man once said, you can only improve what you measure.

Life at its best, is rhythm and a deep focus that comes by doing what you love. On a side note, I will highly suggest you read books like Flow and Ikigai. :)

Stock picking, too, has a rhythm — when you’re in sync, it feels effortless and joyful. Developing a set up and principles that you will operate with becomes really important. But before I get to the part I love, let’s talk about something we rarely speak about openly: the things I hate in stock picking.

Some businesses are so tied to cycles that your research barely moves the needle. You can spend weeks building a model and still end up being hostage to forces way outside the company’s control.

I’m talking about things like:

These are industries where everyone sells the same thing, competes on price, and is constantly being whiplashed by cycles. There’s no joy there, and very little compounding.

Some industries look fine on paper until irrational competition from China enters the chat. Chinese businesses are incentivised on the basis of production and not profitability. Their only goal is to gain market share and drive away competition.

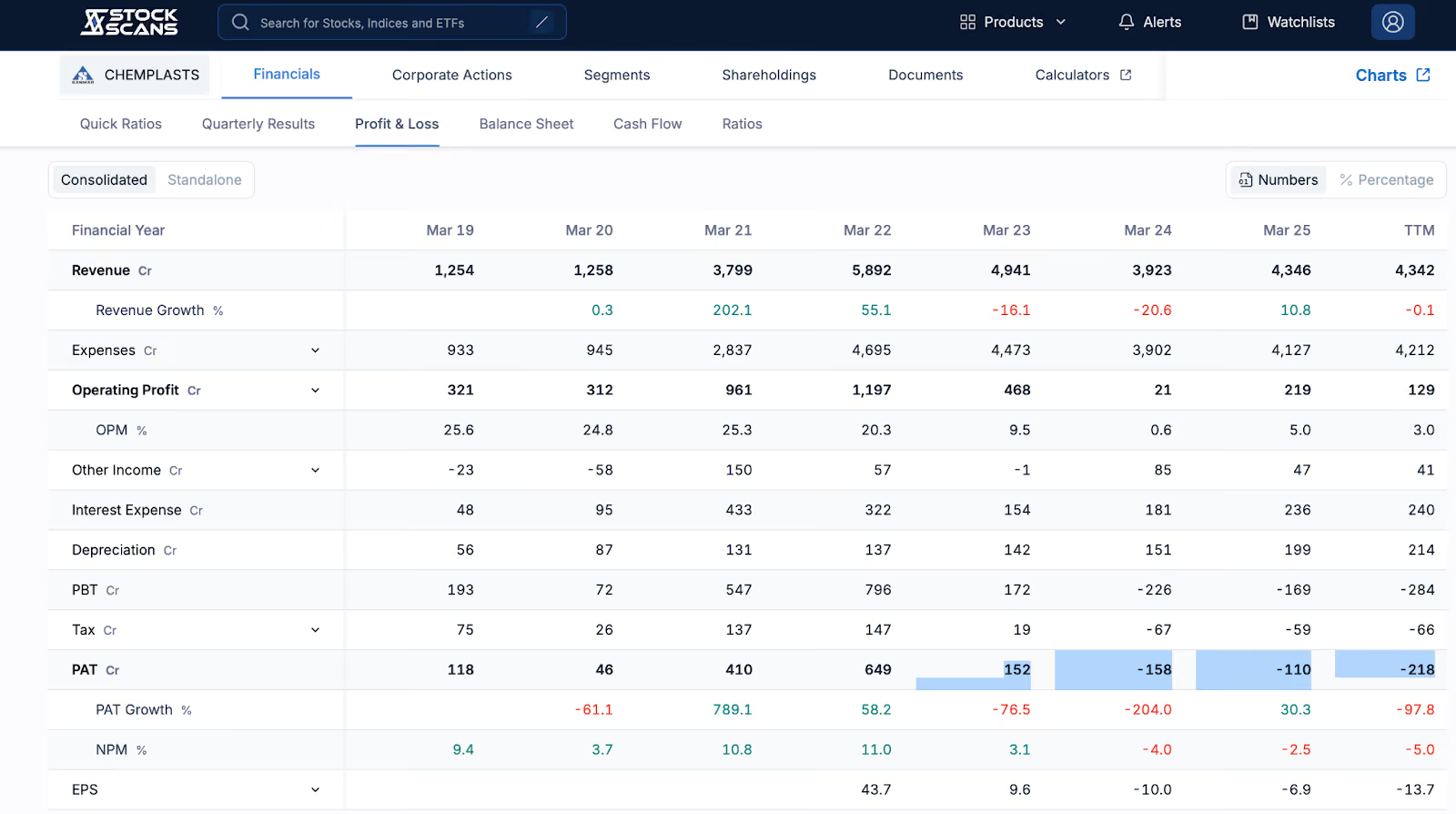

Ask anyone in the PVC space. Chemplast Sanmar experienced exactly this — Chinese players dumping products at prices that don’t even make sense.

How do you build a long-term thesis when the guy on the other side is playing a different game entirely?

China was mentioned more than 20 times in their last few concalls. Just check the profitability over the last couple of quarters for the business.

This is the instant red flag for me. A company that lacks a clear strategy, or worse, tries to be everything to everyone — is usually headed for pain.

Remember Shemaroo randomly entering the restaurant business around 2017–2018 or Quess corp buying Mohan Bagan football club or Amtec Auto going on a crazy debt binge by acquiring companies outside India?

Confusion at the top always shows up in the stock price. A lot of FMCG companies today are at a similar juncture. They aren’t willing to sacrifice the fat margins they make to launch new products and innovate. Business strategy is flawed in my opinion, and makes the sector an "avoid" for me at least till they get their act together.

After all the things I hate to see in a set up, here’s the part I actually enjoy — the reason I get excited about teaching about stocks and stock market in general. Because when you strip away the noise, stock picking is ultimately about understanding businesses — that’s where the real magic lies.

For me, this is the biggest love of all.

A stock is not a ticker. It’s not a chart. It’s not a P/E multiple.

A stock is a piece of a business as Ben Graham said, and the real joy comes from studying what that business is trying to do and whether the strategy makes sense.

I have noticed over the years that the difference between people who compound faster in life vs the ones who do it slower purely lies in certainty and clarity of thoughts. Better clarity and certainty lead to better actions, which helps one in getting to their destination earlier.

Some examples where I saw this clarity over the last few years. Many more such examples exist, but the idea is to teach you through case studies.

When a company has clarity, research becomes joyful. You’re not guessing the future — you’re simply watching the strategy play out.

Two books I often recommend for this:

1. Understanding Michael Porter by Joan Magretta

2. Growth IQ by Tiffani Bova

These books teach you one central truth:

Great companies do fewer things — but with more intensity and patience.

There’s a line in the Indian Army’s AGNIPATH training philosophy:

“Transformation hurts before it inspires.”

Business transitions are exactly like that. They’re painful, messy, slow, and uncomfortable. But when they work, they completely re-rate the company.

This is one part of stock picking I absolutely love — spotting the transition before the P&L shows it.

Some examples:

When you find a company in the middle of a transition and the management knows what it’s doing — it's one of the most rewarding things in stock picking if you stick throughout this journey.

Some businesses aren’t just “good companies,” they’re impossible-to-recreate companies.

I love them because markets often underestimate how powerful time, capital intensity, regulation, and geography can be as moats.

Think about:

These are assets you simply cannot rebuild today. Not at the current cost structures. Not with today’s regulatory hurdles. Not with the inflation we’re dealing with. Definitely not with the patience required to see a long-cycle project through.

These businesses are so asset-heavy and capital-intensive that the entry barrier itself becomes the moat. Over time, this leads to:

People often underestimate what happens when a company owns an asset the world needs but nobody else can afford to replicate at current cost structures. That’s when time becomes your biggest ally as an investor.

Another thing I love deeply about stock picking is finding companies where the supplier, not the customer, has the power.

These are the businesses that:

One of my favourite examples is TDPS and the way they broke into the elite group of global gas turbine genset suppliers.

To put this into context:

There are only four major gas turbine manufacturers in the world:

Getting approvals from them is a multi-year, reputation-driven process. You don’t enter this industry by building a factory. You enter it by getting approvals from the customers.

Another brilliant example is CCL Products, which is another business that possesses supply side dominance when it comes to coffee processing. They have:

You cannot replicate this with capex. You can only replicate it with decades of learning and customer stickiness. This is what gives them supply side dominance.

When I’m analysing a company in this category, I look for four simple markers:

When these four things come together, you get businesses that compound quietly in the background — without needing hype or headlines.

Who makes money when there is a war?

The guys who sell bullets and guns. That is the definition of proxy. In modern day world it could be the guys who sell missiles and drones. :)

One of the most underrated joys of stock picking is finding the proxy — the company that benefits from a big trend without being the one standing in the spotlight.

Peter Lynch often spoke about the California Gold Rush, where the real money wasn’t made by the miners It was made by the guys selling shovels, axes, and tents. Everyone chased the gold but the toolmakers built empires.

Proxy investing is exactly that mindset — look for the companies that quietly enable mega trends rather than the ones trying to claim all the glory.

Some modern examples:

These are businesses where you don’t have to take upstream risk, regulatory risk, or hyper-competitive risk — but you still ride the same secular tailwind. Another big trend of proxy investing is financialisation of savings. :) Many proxies from Exchanges to AMCs to investment bankers to custodians, etc. exist here.

If you want to get good at identifying proxies, there are three habits worth developing:

1. Study the value chain end-to-end

Every industry has adjacencies. Some of the safest compounders live in the middle of the chain. DRHP’s or our YT channel can help you study different industries and value chains.

2. Look for businesses that benefit from the megatrend without being the hero

Instead of betting on who wins the data centre capex game, ask: “Who wins no matter who builds the data centre?”

That’s where the proxy ideas hide.

3. Find companies that benefit when bigger, upstream players grow

Proxies often grow because someone else is spending heavily. They ride the wave without needing to create it.

That’s the elegance of it.

I will conclude this article by sharing the above set ups I absolutely love. I will ask you, the reader, which one is your favourite set up of the 5 above and why in the comments below. 🙂

I will see you soon in the TVGP Stock Picking Checklist class that will be held on 30th November!

0 Comments