Why This Is India’s Next Billion-Dollar Consumer Wave

BY

Shuchi Nahar

No items found.

It started with a moment at the airport. A group of college students — not athletes, not bodybuilders — were waiting at the boarding gate. Each had one thing in common: a shaker bottle. One was sipping a ready-to-drink chocolate whey shake, another carried a high-protein yoghurt, and the third had a protein bar peeking out of her tote.

It made me think that ten years ago, the only people carrying protein shakers were gym bros. Today? It’s the new Starbucks cup. A lifestyle accessory. A quiet flex. This shift is already visible in the numbers and in boardroom strategy slides.

The protein powder market in India is estimated at ₹2,800 crores and growing ~18% YoY (the classic powder category), while protein foods — the bars, high-protein milks, lassis, and yoghurts — are the new growth frontiers. The market is being pushed by social media, quick commerce access, and the rise of fitness and ‘clean eating’ as social currency.

As an analyst, the curiosity to know more about this shift led me to write about a structural shift happening around us so silently that we hardly notice:

This isn’t a supplement trend. This is India’s protein awakening. And it is going to be one of the most structurally important consumption shifts of the next 20 years.

Why Now? India’s Protein Problem Meets a Behavioural Breakthrough

When I dug into the data, the problem stared back at me:

73% Indians are protein-deficient

Protein consumption in India is less than 0.6x the recommended per capita in urban areas.

India has one of the lowest protein penetrations globally despite being the youngest major population.

This is the perfect recipe for a megatrend: High deficiency + rising incomes + lifestyle aspiration + digital education

If clean eating is a ₹2.5 lakh crores megatrend over the next decade, protein alone could command 15–20% of this pie.

Total Addressable Market (TAM) — The Real Deal

Okay, but how big is this really? Big picture – how big is India’s protein market overall?

Different agencies define the “protein market” slightly differently (ingredients vs supplements vs foods), but they broadly agree on the $1.3–1.5 billion range today:

Mordor Intelligence estimates India’s overall protein market at $1.52 billion in 2025, projected to be $2.08 billion by 2030 (CAGR ~6.5%).

Another insight piece pegs it at $1.4 billion in 2024, going to $1.88 billion by 2029 (CAGR ~6.1%).

From there, we drill down into product-level sub-markets.

Protein supplements (all formats together)

This is the classic “whey + powders + RTDs + bars sold as supplements” bucket.

$912.9 million in 2025, expected to reach $1,578.1 million by 2034 (CAGR ~6.3%).

₹7,461 crore (US$ 860 mn) in 2024, projected to ₹13,186 crore (US$ 1.52 bn) by 2033 (CAGR 6.6%).

“India’s protein supplements market is already in the $0.8–0.9 billion zone and is on track to cross $1.5 billion over the next decade.”

Whey protein (powders + ingredients)

Indian whey protein market $266.6 mn in 2024, projected $633.4 mn by 2033 (CAGR ~9.9%).

$185.9 mn in 2025 - $248.4 mn by 2034 (CAGR 3.3%).

$200–270 mn market today, growing high-single to low-double digit, which concentrates the largest segment and isolates the fastest-growing.

Plant-based protein and “smart protein” (India)

This is the “next wave” and the growth rates are much higher than dairy protein:

India's plant-based protein market was $552.4 mn in 2024, expected to be $1,916.1 mn by 2033 (CAGR ~14.8%).

India’s “smart protein” (plant-based, fermentation, cultivated) market is ~₹350 crore (~$42 mn) now, projected to $4.2 bn by 2030 – a 100x potential if it plays out.

Plant-based protein supplements alone grew from $99.5 mn in 2023 → $184.9 mn by 2030 (CAGR 9.3%).

Plant-protein is small today but the fastest-growing leg of the protein story, fuelled by veganism, lactose issues, and climate/ethics consciousness.

Dairy protein and high-protein dairy products

There are two angles here, ingredient market and finished high-protein dairy products.

Dairy protein ingredient market

Indian dairy protein market, $627.3 mn in 2024, is potentially headed to $1,131.9 mn by 2033 (CAGR ~6.3%).

Milk protein: $404.9 mn in 2024 → $889.2 mn by 2033 (CAGR ~9.2%).

This is B2B – proteins used in foods, beverages, and pharma.

High-protein dairy as consumer products

India’s high-protein dairy market (yoghurts, milk, etc.) hit ~$1.5 billion in 2024, after 9.4% growth YoY, and is expected to grow another 12% in 2025.

High-protein dairy is already bigger than powders in value terms and is a key bridge for mass India because it rides on trusted brands like Amul, Mother Dairy, Parag, Zydus, etc.

Protein bars and energy/protein snack bars

Indian protein bars market was $124.2 mn in 2024, projected to be $189.9 mn by 2033 (CAGR ~4.8%).

“Protein bar” figure looks much larger ($863.9 mn in 2024 → $1,266.9 mn by 2030), but likely includes a wider set of bars or uses a different scope.

Business of Food estimates India’s broader energy bar market at ~₹600 crore (~$72 mn) with a significant headroom versus the US.

“Depending on the definition, India’s protein/energy bar market sits somewhere between $120–250 mn today, still tiny compared to total snacking, but growing faster than legacy biscuits & chips.”

You can also mention that snack bars struggle to become daily snacks (D2P consultancy’s point) – price and taste vs Indian savoury cravings.

Ready-to-drink (RTD) protein shakes and beverages

This is one of the hottest sub-segments because it fits the “on-the-go Gen-Z” lifestyle.

India's protein shakes market was ~INR 18 billion in 2023 (≈ ₹1,800 crore), growing at >20% CAGR.

RTD protein beverages at ~$48.8 mn store-based sales in 2024, with online RTD growing fastest as part of the supplement market.

Overall, India RTD beverages market (all categories) is $7.85 bn in 2024 → $13.59 bn by 2033 (CAGR ~6.3%), so protein RTDs are still a small slice but with outsized growth.

RTDs are the “Starbucks-ification of protein” – sippable, flavoured, Instagram-friendly.

Protein powders/shakes as a sub-segment

Sometimes broken out separately from the broader supplement bucket:

Protein shakes alone = Protein shakes alone = INR 18 billion (= ₹1,800 crore ≈ USD ~220 million) in 2023, with >20% CAGR driven by urban professionals and gym-goers.

This overlaps with whey and RTD, so don’t add directly to the supplement market – instead, use it to show how large the “shakes” habit is becoming within supplements.

Smart protein / alt-protein foods

India’s smart protein market (plant-based, fermentation, cultivated) is currently around ₹350 crore (~$42 mn), expected to reach $4.2 bn by 2030.

Let’s construct a conservative TAM framework:

1. Protein Powders TAM: ₹10,000–12,000 crore

Assumptions:

Penetration rises from 3–4% to 10–12% in the light fitness segment

Gym penetration rises from 20% to 50%

Pricing remains stable

2. Protein-Food TAM: ₹40,000–₹50,000 crore

Driven by:

High-protein dairy mainstream adoption

Protein snacks (3.5x faster growth than traditional snacks)

Protein moves from a fitness product → everyday-food ingredient.

That is a ₹1–1.2 lakh crore opportunity over 10–12 years.

The Value Chain: What’s Happening Behind the Scenes?

1. Product R&D + Formulation

Earlier, India mostly imported protein formulations. Today, with brands like MuscleBlaze, HealthKart, Ritebite, Thewholetruth, Avatar, Yogabars, etc. investing in domestic product development.

Flavours localised for the Indian palate

Better digestion enzymes

Blends for women, seniors, and diabetics

This increases adoption by 3–4x.

2. Domestic Manufacturing — The Game Changer

The founder of MuscleBlaze explains this beautifully: Earlier, a 2 kg whey tub cost ₹6,000–₹7,000. With domestic manufacturing + scale + smart procurement:

prices fell 30–40%

quality improved

adoption exploded

India’s protein boom is possible only because manufacturing is finally local.

3. Distribution Reinvented

Three layers of distribution are simultaneously scaling:

E-commerce (2015–2020): Gave India access to protein powders beyond metros.

D2C + Q-com (2020–2024): Turned protein snacks & protein dairy into an impulse buy.

Offline Modern Trade (2024–present): Amul, Mother Dairy, Haldiram’s are entering the game. Fast food giants like McDonald’s launched Protein+ slices, tapping into this mass trend.

When mass FMCG enters, it signals the category is hitting escape velocity.

The Three Big Growth Drivers (Already at Play)

1. Large Companies Are Driving Awareness + Form Factor Innovation

Look at the brands entering protein:

Amul: High-protein milk, high-protein lassi, high-protein dahi

The category becomes mainstream only after incumbents adopt it. We are living through that exact moment.

2. New-Age Protein Brands Are Redesigning Food Categories

Lo! Foods

Reinventing rotis, snacks, and Indian staples into high-protein functional variants

24 → 68 crore revenue jump (FY21–FY25E)

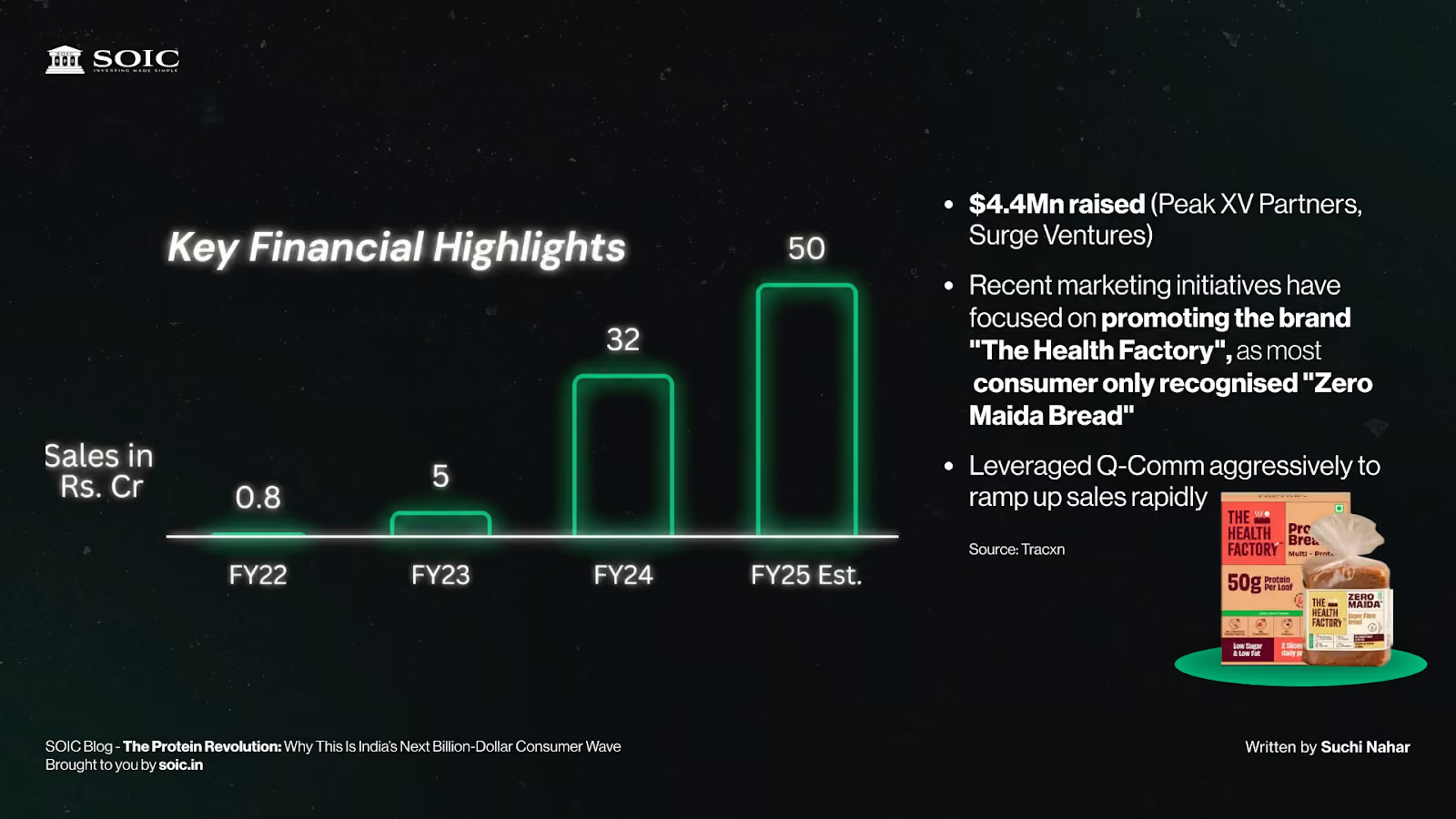

The Health Factory

Clean-label bakery range: zeromaida, no preservatives, high-protein positioned bread (a daily staple) as a functional upgrade cracked the taste and marketing code.

Why Does It Work?

Staple-first approach: attacks a daily-consumed item → higher repeat frequency nutritional differentiation: breads with 3–4x more protein than regular variety.

TBOF: Turning Grandfather’s Farming and Grandmother's Recipes into a Global Brand

Transitioned to organic farming after witnessing soil fertility decline Moved from raw produce - value-added products: moringa powder, Khapli wheat Built a farmer network of 3,000+, covering 4,000–5,000 acres.

Why Does It Work? Authentic brand stories rooted in “grandfather’s farming, grandmother’s recipes" gains consumers’ trust through clean packaging, community-led marketing. Patient capital, bootstrapped for the first 8–9 years.

These companies are not riding a trend — they are creating it.

Then came the cultural accelerants:

Fitness became social currency

For 35+ consumers, fitness is now the new wealth signalling

GenZ drives 40–43% of spend

A generation that snacks 3–4 times a day demands functionality and pays a premium for clean food.

3. Quick commerce changed everything

Q-commerce has made high-protein foods as accessible as chips. This is where the flywheel begins.

Market Size: How Big Is India’s Protein Opportunity?

1. Protein Powder Market

₹2,800 crore today (growing at 18% YoY)

Penetration among gym-goers:

20% for heavy gym population

Just 3–4% for light fitness users

Benchmark: In the US, 85% of gym-goers use supplements.

If India simply follows the US gym-penetration curve, this market can grow 4–5x over the next decade.

2. Protein Foods Market

The real non-linear growth is here.

Protein food categories (bars, oats, shakes, high-protein dairy, nut butters, yoghurts) are scaling faster than powders.

The report shows the spread clearly — from bars and peanut butter to high-protein milk, lassi and dahi

Quick commerce adoption + new D2C formats = the perfect distribution shift.

3. Clean Eating & Functional Foods Market

The larger structural umbrella under which protein is exploding:

India’s wellness and clean eating food market is growing at 20% CAGR, and is expected to reach $30B by 2026. Functional foods are premium, high-gross-margin, and repeat-driven.

Within that, protein is the single most important functional macronutrient, driving:

RTD shakes

High-protein dairy

Protein bars

High-protein snacks

Fortified breads, rotis, and traditional foods

Three things are colliding:

A real nutritional gap. Reports highlight severe protein deficiency in India — a structural unmet need that functional foods can address. The scale of deficiency frames protein as a functional necessity in the nutrition story.

A new consumer: Gen-Z and Millennials. Gen-Z contributes ~40–43% of the clean-eating spend and is willing to pay premiums for functional, tasty, on-the-go products. In other words: the people who snack more, post more, and try new products more often are the very people who make protein mainstream.

Discovery & access via e-commerce and q-commerce. E-commerce first exposed non-metro consumers to powders. Now Q-commerce and D2C brands make protein an impulse category — an order that shows up in 10–20 minutes next to your chips. That distribution swing is what converts awareness into repeat buying.

Market Size and Growth: The Two Big Pies

Protein powder: ₹2,800 crore today, ~18% YoY growth. Powder remains important but is starting to plateau in growth share as foods scale.

Protein foods and clean eating umbrella: The broader wellness food / clean-eating market is growing at ~20% CAGR and was projected to reach ~$30bn by 2026 in the BRC deck — with protein and functional snacking being major drivers. This means protein-adjacent categories (high-protein milk, bars, fortified staples) have massive headroom.

Investment activity: Funding for health-food brands exploded (e.g. $65M raised by health food brands in H1’25 vs much smaller amounts in prior years), and ~90% of protein startup funding happened in the last 2 years, signalling investor belief that this is an early large market.

Put simply, powder is big and healthy, but the non-powder protein food market is where the non-linear growth and scale will come from.

Why the Demand Surge Is Happening — Not Just in Gyms

Here’s what I see fuelling this wave:

Rising health awareness and nutritional deficiency push: As more Indians become conscious of health, protein deficiency (particularly in vegetarian diets) becomes a concern. Functional foods and supplements are emerging as easy solutions — especially for urban, busy lifestyles.

Consumer lifestyle shift — from “bulking” to “wellness + everyday nutrition”: The new consumer isn’t just a gym-goer. It’s the corporate professional grabbing RTD (ready-to-drink) protein shakes for breakfast, the young adult adding protein powders to traditional meals, or the health-conscious parent buying protein-enriched dairy for kids. As one recent article describes — “protein booze” is even being tried as a novelty after-work drink.

Yes, you read that right: some brands are experimenting with protein-infused alcoholic beverages —I was so surprised when I read that protein has crossed over from health to lifestyle and/or social domain.

Distribution and product innovation: powders are old news: The real growth now is in protein-enriched foods and drinks — bars, RTD shakes, high-protein dairy, snacks, even everyday staples. Consumers want convenience, taste, and nutrition — not necessarily gym-level protein. Reports highlight growing demand for plant-based proteins, flavored ready-to-drink options, and clean-label products.

Growing reach beyond metros — tier-2 / tier-3 India joining the wave.

Earlier, protein powders were largely an urban, metro-phenomenon. But data shows demand expanding into smaller cities, thanks to improving awareness and wider distribution.

How Indian Players (Old & New) Are Jumping In — And Reshaping the Space

This isn’t just about global brands throwing products at India. A lot of action is happening right here, domestically.

New-age health-food and functional brands: Indian firms producing protein bars, shakes, clean-label snacks and ready-to-eat protein products are growing rapidly. There’s rising demand for plant-based + vegetarian solutions — a sweet spot for India’s mostly non-meat-eating population.

Dairy and legacy protein producers expanding their portfolio: As awareness grows, established proteins (like whey) are no longer sufficient. Brands are doubling down on enriched dairy, RTD beverages, and fortified foods — converting traditional nutrition channels (milk, dairy) into protein-rich mainstream pipelines.

Plant-based and sustainable protein options gaining ground: As consumers (especially younger ones) care more about sustainability, plant proteins (soy, pea, rice, blends) are gaining share — supported by global trends and environmental awareness.

Experimentation and “fun” products — signalling mass-market adoption: The “protein booze” story is perhaps the most extreme example. But it illustrates a broader dynamic: protein is no longer just functional. It’s becoming fashionable, even indulgent. That’s how categories go mainstream.

How the value chain is reshaping to make protein mainstream?

I think of the protein value chain like three linked gears — product innovation, manufacturing, and distribution — and all three are spinning faster now.

1. Product and format innovation — it’s no longer “just whey”

Powder used to mean tubs and gym use. Now product innovation is attacking every eating occasion:

Protein bars and peanut butters for snacking: You won’t believe how handy it is to carry 3-4 protein bars when I’m traveling for events, seminars, or vacations! They really save me a lot of time and keep me fueled on the go. Give it a try – you’ll thank me later!

Ready-to-drink (RTD) shakes and high-protein yoghurts for on-the-go

Fortified staples: high-protein milk, lassis and even protein-fortified sweets and kulfi.

The “protein dilemma” — a market full of high-price tags with varying nutritional value — and outlines the winning formula: radical honesty, taste (Indian palate), and innovation beyond whey (plant proteins, blends). That’s a roadmap for winners.

2. Domestic manufacturing — the cost & quality inflection

Domestic manufacturing is the unsung hero. Several Indian players (and new contract manufacturers) are localising whey processing and formulation capability, which:

reduces import dependency and cost

improves traceability and trust (“made in India” whey vs unknown imports)

enables faster product iteration and scale for lower price points.

To connect with Indian players, Parag Milk makes a bold statement that truly captures attention - they produce their own whey (via cheese production) and have launched Avvatar whey and protein wafer bars — a direct example of upstream (cheese → whey → B2C protein products) integration. That vertical play lets traditional dairy scale into functional nutrition efficiently.

3. Distribution — from e-commerce to quick commerce to modern retail

E-commerce seeded powder adoption in Tier-1 and Tier-2.

Q-commerce made RTD & snack formats impulse buys (huge for repeat).

Now, mainstream FMCG channels and large dairy brands are adding protein SKUs, bringing the product to the household. The BRC deck shows how quick commerce and D2C models accelerated trial and tasting, while incumbents (Amul, Marico, etc.) are moving in by product extension and tuck-ins.

How Are Indian Players Participating — A Layered Picture

Three types of market participants are racing:

A. New-age D2C challengers (taste, branding, Q-commerce mastery)

Brands like the functional-food D2C cohort are converting Gen-Z trial into habit with strong branding, clean labels and Q-commerce reach. D2C players show much higher YoY growth and premium gross margins. This group is winning taste + authenticity + direct consumer data.

B. Large legacy players and dairy majors (scale, distribution, trust)

Amul and large dairy houses are experimenting with high-protein milk & dairy variants.

Parag Milk is explicitly repositioning from dairy FMCG to a health & nutrition company — Avvatar whey, Avvatar Protein Wafer Bar, Pride of Cows expansion — and plan to keep building protein SKUs as a strategic thrust. They talk about producing whey in-house (via cheese) to ensure quality and economics. Their new-age business grew rapidly and now contributes meaningfully to turnover.

Large companies bring trust, distribution muscle and buyer reach; they also normalise protein for households by embedding it into everyday formats (milk, sweets, breads).

C. FMCG & QSR “protein halo” entrants

McDonald’s launched a “Protein Plus” slice as a low-friction add-on fast-food and mainstream dessert players have started high-protein variants. This is crucial, when QSRs make protein a menu option for ₹25, the average consumer starts accepting protein as normal.

Examples that prove the thesis:

Protein powder market ₹2,800 crore, ~18% YoY; emerging protein foods include high-protein milk, lassi and dahi (clear product map). Clean eating market ~20% CAGR; Gen-Z drives ~40–43% of spend; $65M+ funding momentum with 90% of protein startup funding in last 2 years; D2C growth multipliers and premium multiples for functional food brands.

Parag crossed ₹1,000 crore quarterly revenue; new-age portfolio (Avvatar, Pride of Cows) grew ~79% YoY and Avvatar expanded six-fold; Parag launched Avvatar Protein Wafer Bar and is producing whey in-house to improve product economics and quality — explicit strategic shift from dairy into nutrition.

Once affordability kicks in, the category switches from “aspirational” to “habitual.” D2C players capturing premium multiples and scaling revenue quickly — proof that once taste & price meet, customers pay.

Why Protein is Not a Fad: What CEOs are Telling Us

Parag Milk Foods — Protein Strategy in Short

Actively pivoting from Dairy → Nutrition company → management positioning whey as a core growth engine.

Avvatar = flagship protein brand (100% vegetarian whey, made in India) — not a side SKU, but strategic.

Targeting30–35% CAGR in whey business; aim for 20–25% whey market share by FY27–28.

New Age brands (Avvatar + Pride of Cows) growing 79% YoY; now ~9% of revenue (up from 6%).

Expandingon-the-go protein formats → Avvatar Fuel Whey + Protein Wafer Bar for snacking occasions.

Long-term:20%+ portfolio to be health and nutrition SKUs — youth-focused, premium.

Parag doesn’t want to sell only milk anymore — they want to own the Indian shaker bottle and the protein snack in your gym bag.

Zydus Wellness — Protein Snacking Strategy in Short

Uses Max Protein brand as the spearhead for health-focused snacking. Max Protein is performing above expectations post-acquisition.

New SKUs: RiteBite Millet Wafer Protein Bar → 10g protein, no maida/palm oil/added sugar. Nutralite Activ Peanut Butter as protein-rich everyday food.

Focus on multi-occasion usage — not just fitness; snack anytime positioning.

Scaling through Q-commerce + E-commerce + deeper General Trade reach across India. → New consumers entering the portfolio.

Management guiding for sustained double-digit growth + 17–18% EBITDA ahead, driven by protein-led categories.

Strategic stance: build a multi-category, multi-channel health ecosystem, not a single protein SKU.

Zydus is turning protein into a lifestyle snack — the kind you order with cold coffee on Blinkit, guilt-free. I've recently found my ultimate snack solution: Max Protein Bars! They’ve quickly become my go-to option every time I need a quick, delicious boost.

Risks:

Protein labelling confusion and poor formulations (the “protein dilemma.”

Commodity volatility (milk/whey prices), which Parag mentions as a headwind, but they offset via product mix and pricing power

Taste acceptance, if it tastes like chalk, repeat rates rule the product out.

Blueprint for winners

Radical honesty and transparent labelling — build trust (BRC admonition).

Solve for the Indian palate — taste matters more than “functional claims” (BRC).

Local manufacturing and backward integration — ensure quality and cost control (Parag’s in-house whey strategy).

Distribution mastery — Q-commerce for trial, modern trade and MT for scale.

A few recent observations have sparked my curiosity and inspired me to explore this topic more deeply.

The Airport Shaker: A non-gym Gen-Z carrying a shaker — not for the gym, but as a daily accessory. Signal: protein as fashion (status + health).

Hotels providing Epigamia Greek Yogurt in breakfast or takeaways, which earlier was not trending

Protein Add-on at QSR: The ₹25 protein slice in a burger — convenient, cheap, normalising protein with zero behaviour change.

My Mom’s Pantry Upgrade: So she started choosing high-protein dahi or bread, saying it’s “healthier.” That’s mass adoption, not niche fitness.

That’s mass adoption, not niche fitness.

Check this out! McDonald's is shaking things up by launching an exciting new protein category. This trend is definitely one to watch!

McDonald's protein bun isn't a single product but refers to two recent innovations in India: the Multi-Millet Bun, a healthier bun made with five millets, and the Protein PLUS slice, a plant-based, cheese-like slice adding 5g of protein to any burger, both developed with India's CSIR-CFTRI.

These offerings boost protein and nutrition for health-conscious consumers, allowing customization for better-for-you burgers like the McAloo Tikki or McChicken.

This latest innovation is the result of our exclusive collaboration with CSIR-Central Food Technological Research Institute (CFTRI), leveraging their decades of expertise in protein research. By combining McDonald’s operational excellence with CFTRI’s cutting-edge food science research, they have created the Protein Plus slice to offer nutritionally enhanced food options. This launch builds on the success of their Multi-Millet Bun, furthering their commitment to delivering innovative and indulgent choices.

The Protein Plus slice integrates seamlessly into your favourite McDonald’s experience. Simply add it to any burger, from the classic McAloo Tikki to the McSpicy Paneer, and enjoy enhanced 5 gm nutrition with each slice, without compromising on the taste.

These micro-moments are the cultural nodes that knit awareness into habit.

Investment lens — where the optionality is.

If you’re mapping investment ideas, think in three buckets:

Ingredient and manufacturing plays — companies building whey or pea protein processing, flavours and contract manufacturing. (High operating leverage when branded demand ramps). Parag’s whey and Zydus Protein bars integration is a direct example.

D2C and functional food challengers — brands that have nailed taste + Q-commerce + clean labels. These trade at premium multiples but can scale quickly.

Listed FMCG or Dairy incumbents — play the distribution + trust angle. When companies like Amul, Parag, Zydus, etc., mainstream FMCG add protein SKUs, they can bring the category to millions — a different risk/return profile from startups.

Sometimes, the biggest revolutions don’t announce themselves loudly. They begin quietly — in a shaker bottle at the office, in a mother’s grocery basket choosing high-protein dahi over the regular, and in a young boy swapping chips for a protein bar because his favourite athlete said so.

When I zoom out at the market sizes, CAGR projections, boardroom commentary — everything screams growth. Parag Milk wants to be known for nutrition, not just dairy. Zydus is turning protein into a cool snack you flex on Instagram. Every global and local player is betting on India’s protein awakening.

We are stepping into India’s Protein Decade — and yes, it will create new categories, new brands, and new market leaders. But more importantly, it will create a healthier nation — one that finally recognises the power of protein not as a gym-thing, but a life-thing.

This isn’t just a market opportunity. It’s a cultural upgrade. And for once, it feels like a megatrend that’s truly good for us — physically, emotionally, and economically.

The protein wave is here — and if you ask me, this is just the first scoop.

Sources and where I pulled what (quick map)

HealthKart and MuscleBlaze deck

BRC “Clean Eating” deck

Parag Milk Foods and Zydus Conference Call Transcript

Parag Milk and Zydus Annual Report

Disclaimer:

The information provided is for educational purposes only and should not be considered investment advice. We are SEBI-registered research analysts. We believe that investment decisions should be based on personal conviction and not borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.

No items found.

Author

Shuchi Nahar

Masters in Finance with 5 years of industry experience. My approach is to take one sector at a time and explore plausible Investment ideas.

0 Comments